The VIX closed at 16.27, indicating an implied one day move of +/-1.03% & an implied one month move of +/-4.7% for the S&P 500.

Highest Technical Rated S&P 500 Components Per 11/6/2024’s Close:

1 – PLTR

2 – UAL

3 – SYF

4 – NCLH

5 – DFS

6 – RCL

7 – CCL

8 – PAYC

9 – TRGP

10 – VST

Lowest Technical Rated S&P 500 Components Per 11/6/2024’s Close:

1 – SMCI

2 – EL

3 – CE

4 – MRNA

5 – QRVO

6 – ENPH

7 – DLTR

8 – APTV

9 – DG

10 – HII

Highest Volume Rated S&P 500 Components Per 11/6/2024’s Close:

1 – DFS

2 – FSLR

3 – TFC

4 – COF

5 – NUE

6 – IFF

7 – CE

8 – GS

9 – ENPH

10 – AMT

Lowest Volume Rated S&P 500 Components Per 11/6/2024’s Close:

1 – LW

2 – RMD

3 – AMD

4 – SWKS

5 – EW

6 – AMAT

7 – CMG

8 – TSN

9 – LUV

10 – WRB

Highest Technical Rated ETFs Per 11/6/2024’s Close:

1 – DPST

2 – TSLR

3 – TSLL

4 – TSLT

5 – NVDU

6 – NVDL

7 – NVDX

8 – TSL

9 – FAS

10 – CRPT

Lowest Technical Rated ETFs Per 11/6/2024’s Close:

1 – MSOX

2 – TSLZ

3 – TSDD

4 – TSLQ

5 – NVDQ

6 – NVD

7 – YANG

8 – SKRE

9 – SMCX

10 – UVIX

Highest Volume Rated ETFs Per 11/6/2024’s Close:

1 – USNZ

2 – IBTO

3 – EV

4 – GUSA

5 – NOVP

6 – UPAR

7 – DECP

8 – XDEC

9 – BGLD

10 – XTN

Lowest Volume Rated ETFs Per 11/6/2024’s Close:

1 – BHYB

2 – GVUS

3 – PSMR

4 – TSEC

5 – MSTI

6 – GENT

7 – KEAT

8 – USSH

9 – MAGG

10 – GSID

Highest Technical Rated General Stocks Per 11/6/2024’s Close:

1 – DRUG

2 – FOXO

3 – CHSN

4 – PRKR

5 – WLGS

6 – MNPR

7 – SGMO

8 – NXL

9 – MPXOF

10 – ELWS

Lowest Technical Rated General Stocks Per 11/6/2024’s Close:

1 – EFSH

2 – SMX

3 – MTNB

4 – SEEL

5 – APDN

6 – WTO

7 – PEGY

8 – BSLK

9 – VCIG

10 – MULN

Highest Volume Rated General Stocks Per 11/6/2024’s Close:

1 – FOXO

2 – SLG

3 – OUT

4 – SONN

5 – TMQ

6 – DATS

7 – SGBX

8 – KKPNY

9 – ROIC

10 – ARBB

Lowest Volume Rated General Stocks Per 11/6/2024’s Close:

1 – ALVOF

2 – MRRDF

3 – YIBO

4 – MTBLY

5 – IFABF

6 – FHSEY

7 – ATRWF

8 – BRVMF

9 – MARIF

10 – GCEH

*** THE LIST ABOVE IS STRICTLY FOR INFORMATIONAL PURPOSES – I MAY OR MAY NOT HAVE OR INITIATE A LONG, SHORT, OR LONG/SHORT POSITION IN ANY NAME ABOVE AT ANY TIME ***

The VIX closed at 20.49, indicating a one day implied move of +/-1.29% & an implied one month move of +/-5.92% for the S&P 500.

Highest Technical Rated S&P 500 Components Per 11/5/2024’s Close:

1 – PLTR

2 -UAL

3 – NCLH

4 – VST

5 – PAYC

6 – TRGP

7 – IP

8 – RCL

9 – DAY

10 – CCL

Lowest Technical Rated S&P 500 Components Per 11/5/2024’s Close:

1 – SMCI

2 – EL

3 – CE

4 – QRVO

5 – MRNA

6 – HII

7 – APTV

8 – DLTR

9 – DG

10 – DXCM

Highest Volume Rated S&P 500 Components Per 11/5/2024’s Close:

1 – CE

2 – WYNN

3 – PLTR

4 – ADM

5 – FOXA

6 – DD

7 – EMR

8 – STE

9 – NXPI

10 – IT

Lowest Volume Rated S&P 500 Components Per 11/5/2024’s Close:

1 – NKE

2 – DOV

3 – MU

4 – CRWD

5 – WRB

6 – GL

7 – SCHW

8 – KEY

9 – COO

10 – FCX

Highest Technical Rated ETFs Per 11/5/2024’s Close:

1 – YINN

2 – NVDU

3 – NVDX

4 – NVDL

5 – XPP

6 – CNXT

7 – KOLD

8 – BABX

9 – DPST

10 – WEBL

Lowest Technical Rated ETFs Per 11/5/2024’s Close:

1 – YANG

2 – TSLZ

3 – TSDD

4 – NVDQ

5 – NVD

6 – TSLQ

7 – SMCX

8 – BOIL

9 – MRNY

10 – FXP

Highest Volume Rated ETFs Per 11/5/2024’s Close:

1 – GUSA

2 – OVLH

3 – SPTB

4 – JFWD

5 – OVT

6 – DVLU

7 – OVL

8 – CPLS

9 – EAOK

10 – MNBD

Lowest Volume Rated ETFs Per 11/5/2024’s Close:

1 – GVUS

2 – UNIY

3 – SPAX

4 – GENT

5 – GGUS

6 – USSH

7 – JHHY

8 – QVMM

9 – MAYT

10 – KEAT

Highest Technical Rated General Stocks Per 11/5/2024’s Close:

1 – DRUG

2 – WLGS

3 – MNPR

4 – CHSN

5 – VSTE

6 – SPPL

7 – PRKR

8 – NXL

9 – SGMO

10 – BSGM

Lowest Technical Rated General Stocks Per 11/5/2024’s Close:

1 – EFSH

2 – ADTX

3 – CETX

4 – RDY

5 – SEEL

6 – MDJH

7 – MULN

8 – WTO

9 – EDBL

10 – PEGY

Highest Volume Rated General Stocks Per 11/5/2024’s Close:

1 – AGFY

2 – OUT

3 – TWO

4 – BNOX

5 – ZVSA

6 – GCTK

7 – BJDX

8 – ZCAR

9 – MAMA

10 – ALBT

Lowest Volume Rated General Stocks Per 11/5/2024’s Close:

1 – MRRDF

2 – NSRCF

3 – TAOIF

4 – SEOVF

5 – DTEGF

6 – GGGOF

7 – RNGE

8 – BDL

9 – PFLC

10 – PWM

*** THE LIST ABOVE IS STRICTLY FOR INFORMATIONAL PURPOSES – I MAY OR MAY NOT HAVE OR INITIATE A LONG, SHORT, OR LONG/SHORT POSITION IN ANY NAME ABOVE AT ANY TIME ***

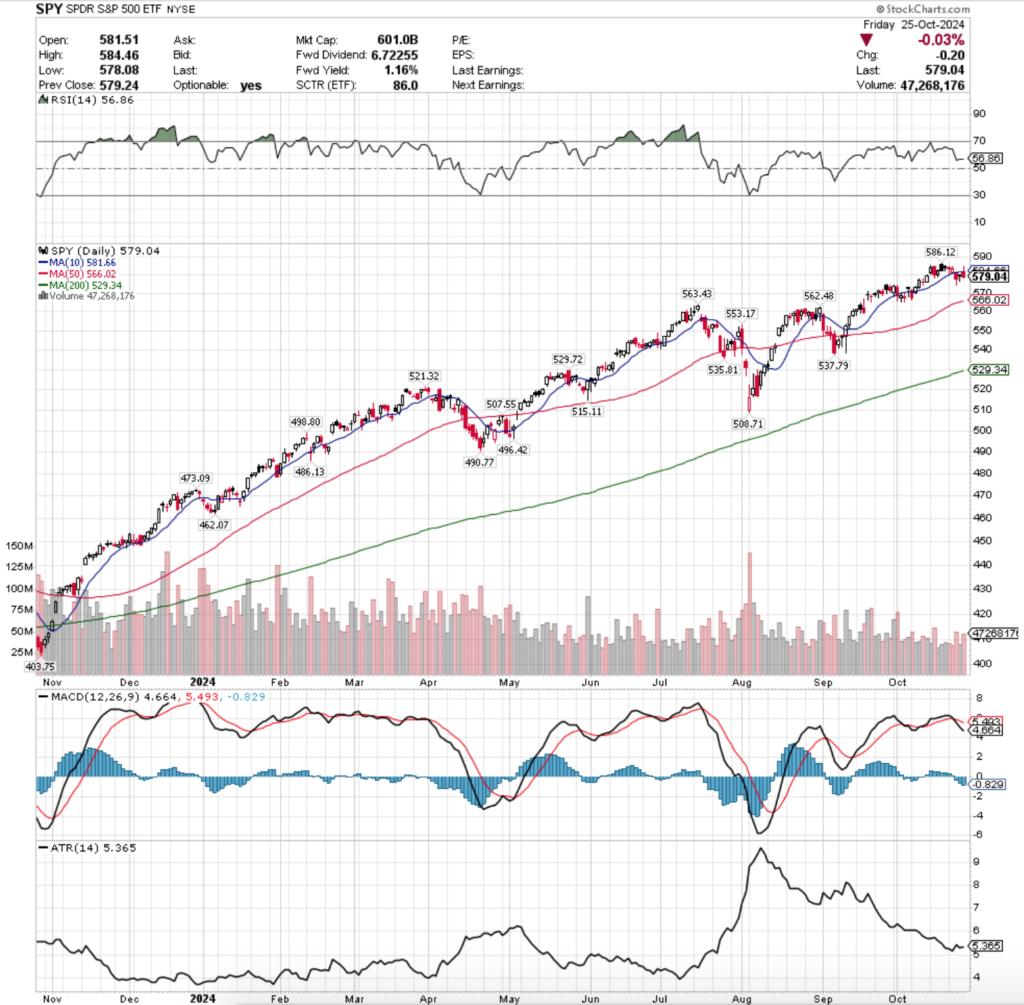

SPY, the SPDR S&P 500 ETF dipped -0.95% this week, while the VIX closed at 20.33, indicating an implied one day move of +/-1.28% & an implied one month move of +/-5.88% for the S&P 500.

SPY ETF – SPDR S&P 500 ETF’s Technical Performance Over The Past Year

Their RSI has flattened out just above the neutral 50 level & sits at 56.86, while their MACD crossed over bearishly on Wednesday.

Volumes were -35.77% below the previous year’s average (40,436,000 vs. 62,957,183), as investors continue to sit on edge waiting to see what mega cap tech earnings & PCE/inflation data tell us this week.

Monday the week began on a sour note, as the session’s candle resulted in a dragonfly doji that tested the support of the 10 day moving average.

While support held up, volumes were even lower than last week’s, indicating that there was still a good deal of fear & uncertainty about SPY’s outlook for the week.

This continued into Tuesday, where on the lowest volume of the week SPY opened in line with the prior day’s close, only to continue lower throughout the day & settle rested atop the support of the 10 DMA.

Wednesday the 10 DMA’s support broke down, as the session opened below it, tested briefly above it only to fall & close lower, with a large lower shadow signaling that there was still more downside appetite among market participants, but that the bulls had temporarily forced a stronger close.

Thursday saw a glimmer of optimism, as another dragonfly doji candle occurred while SPY tried to claw back some of Wednesday’s losses, but note that the volume was extremely weak on Thursday, which does not indicate that there was much bullish sentiment behind they day’s move.

Thursday’s candle could be considered a bullish harami, but based on the low volume sentiment behind the session & the lower close than open it should be viewed bearishly.

One area of hope from Thursday’s session was that the low of the day was not as low as Wednesday’s, but this is nothing to hitch your wagon to just yet.

Friday managed to open higher, but still below the 10 DMA’s resistance, break temporarily above the resistance level, before ultimately closing near the low of they day -0.03% on the second highest volume of the week.

This “risk-off” into the weekend did not set the stage for an enthusiastic new week & indicates that there is still a bit of skepticism among market participants about the current strength of the S&P 500.

As we look to the coming week the 10 day moving average’s relationship to SPY’s share price remains one of the most important areas to keep an eye on this week.

Support gave out & resistance held strong in the latter half of the week, which will remain important in determining the direction SPY goes in heading into the latter portion of the week.

If the price stays below the 10 DMA’s resistance for too long market participants will become exhausted & impatient likely leading to some selling pressure forcing SPY’s price lower.

This is especially true if there is not a meaningful increase in volume, as the current tumbleweed low levels are unsustainable in the long run if SPY’s valuation is to remain justified near all-time highs.

The direction that volume increases in & the magnitude of the increase will also remain important to watch, as it will shed light into which way market participants are likely to continue moving in once a trend has been established.

Watching how investors are participating will help you to anticipate which direction things will move in in the short-to-medium term.

Something else of note for this week is that now that SPY’s price is below the 10 DMA, the first support level (S1) is their 50 DMA, which is continuing to rise.

Looking at their past year’s chart (above) you can see that more often than not in the past year when the price has gone between these two moving averages there has often been declines, many of which have been able to break down & test the 50 DMA’s support (and two in particular that broke down through it entirely).

This leads to something else that has begun emerging from SPY’s chart over the past week, the appearance of a potential bearish head & shoulders set up forming.

Look back to 9/19/2024’s gap up session & note that the left shoulder forming, with the recent all-time high as the head & the right shoulder yet to form.

Should the moving averages observation above hold true that will begin the formation of the right hand shoulder over a 5-6 week period (assuming a more rapid decline doesn’t take place instead).

The low volume of the past couple of weeks has made this become even more of a possibility as there is no fuel in SPYs tank & looking at their MACD & RSIs it begins to look even more strongly a possibility.

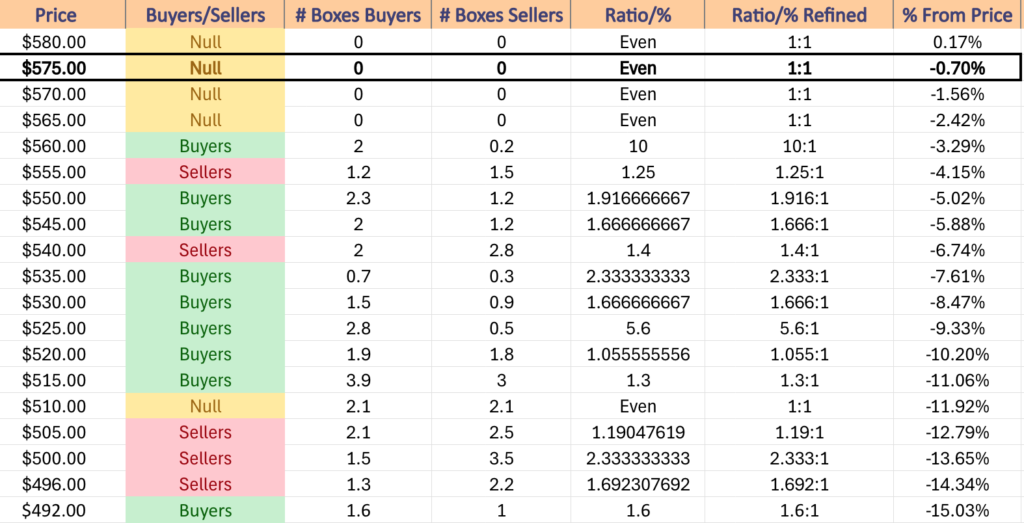

SPY has support at the $566.02 (50 Day Moving Average, Volume Sentiment: NULL, 0:0*), $563.43 (Volume Sentiment: Buyers, 10:1), $562.48 (Volume Sentiment: Buyers, 10:1) & $553.17/share (Volume Sentiment: Buyers, 1.92:1) price levels, with resistance at the $581.66 (10 Day Moving Average, Volume Sentiment: NULL, 0:0*) & $586.12/share (All-Time High, Volume Sentiment: NULL, 0:0*) price levels.

SPY ETF’s Price Level:Volume Sentiment Over The Past ~2 Years

QQQ ETF – Invesco QQQ Trust ETF’s Technical Performance Over The Past Year

Their RSI is trending towards the overbought level of 70 & currently sits at 58.85, while their MACD crossed over bearishly last week.

Volumes were -21.75% below the previous year’s average level (31,432,000 vs. 40,167,659), which as noted in last week’s market review note is severely low in relation to the volumes that QQQ (and the other index ETFs sans-IWM) had previously enjoyed in years past.

QQQ had a different week from SPY, but still did not have a strong performance as investors have begun to sour on the two indexes in favor of IWM & DIA recently.

QQQ opened the week on a quite uncertain note, where mediocre volume resulted in a bullish engulfing candle that resulted in a spinning top.

They briefly broke down through the 10 day moving average’s support during the day, but managed to power higher to close the day higher.

The weak volume & temporary support break down are cause for concern though, which QQQ showed on Tuesday.

While at first glance Tuesday was another bullish engulfing candle & it did not close with the same “indecision” surrounding it that Monday’s spinning top indicated, it should be noted that the volume was weak & that the session opened below the resistance of the 10 DMA.

The fact that the support level was feeble enough to be broken through before the market opened is not indicative of strength & conviction behind QQQ, which was proven with Wednesday’s declining session.

While prices were able to briefly break above the 10 DMA’s resistance, they spent most of the session below it & Wednesday’s volume was the strongest of the week, which is telling about the lack of investor confidence in QQQ as there has not been any major run up to trim profits from & volume hadn’t been that high since 10/1/2024 (also declining volume).

The session’s lower shadow also signals that there was more downside appetite.

Thursday showed the weakest volume of the week for QQQ on a session that closed in a dragonfly doji, indicating indecision, particularly as the 10 DMA was not crossed.

It created a harami cross pattern with Wednesday’s session, which led to Friday’s gap up open that skipped right over the 10 DMA’s resistance.

Friday’s move came on the second highest volume of the week, indicating that there was some support behind it from market participants, however it closed as a gravestone doji, indicating that the bears were still out in full force & likely signaling that there was some intra-day profit taking after the gap up, based on the height of the upper shadow.

QQQ’s week ahead will also be heavily dependent on how the price is in relation to their 10 DMA, which closed Friday as their second level of support (S2).

In the event that prices make a break lower & get pinned between the 10 & 50 DMAs there is additional local support to help prop prices up, but the curve of the 10 DMA should be cause for concern.

Once the 10 DMA curls over as much as it has recently it has led to lower prices in the coming sessions that come in the form of steeper declines vs. consolidation.

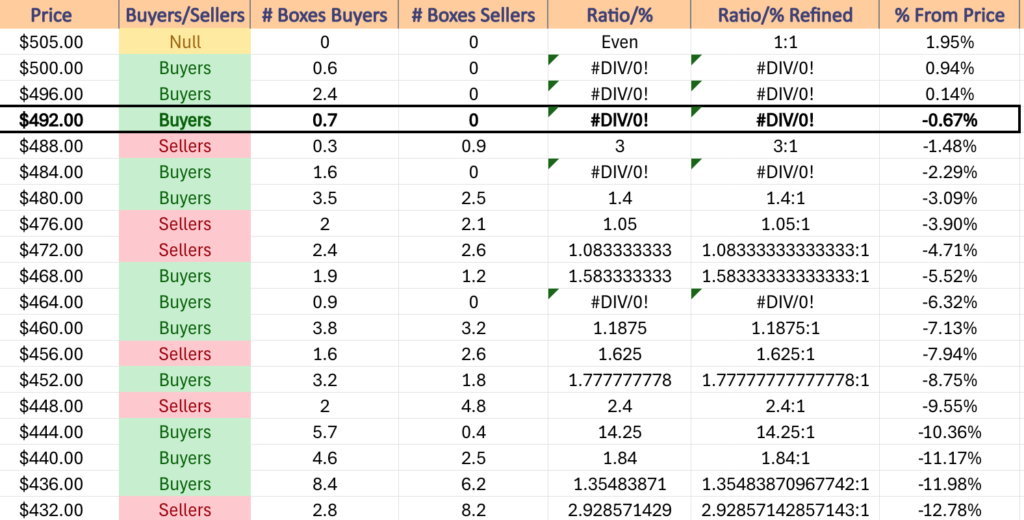

When referencing the volume sentiment by price level table below you’ll notice that this may well lead to a 5%+ decline based on the Buyer:Seller sentiment at these levels over the past ~2 years.

While this week’s earnings calls may be enough of a catalyst to forge higher for QQQ, they too are showing signs of a bearish head & shoulders pattern emerging over a similar time period as SPY’s.

Friday’s high would become the head (assuming nothing in the days to come is higher than it), giving it 4-6 weeks until the right shoulder is formed (in the event that it does not decline more rapidly).

In the event of an earnings catalyst this week, it will be imperative to see how the $502.81 resistance level holds up, as in the event that it is broken through the landscape for QQQ will change (pending on how their oscillators react to the jump).

While QQQ has shown higher peaks & higher troughs since the declines of July, the lackluster participation rate being signaled by their current volume levels raises cause for concern still moving into the week ahead & like SPY, watching their the direction & fluctuations that their volume goes in will lend tells into where they head next.

QQQ has support at the $493.70 (Volume Sentiment: Buyers, 0.7:0*), $493.24 (Volume Sentiment: Buyers, 0.7:0*), $484.86 (Volume Sentiment: Buyers, 1.6:0*) & $480.15/share (50 Day Moving Average, Volume Sentiment: Buyers, 1.4:1) price levels, with resistance at $493.70/share (All-Time High, Volume Sentiment: Buyers, 0.7:0*) price levels.

QQQ ETF’s Price Level:Volume Sentiment Over The Past ~2 Years

IWM ETF – iShares Russell 2000 ETF’s Technical Performance Over The Past Year

Their RSI recently crossed below the neutral mark of 50 & sits currently at 47.86, while their MACD has been bearish since Wednesday.

Volumes were -38.02% below the prior years average (21,100,000 vs. 34,043,929), which is peculiar, given that the Russell has fared the best of the major four indexes in terms of volume since 4/19/2024 & is something to consider in any analysis of the small cap index.

After rounding the prior week out with a couple of bad sessions the pain continued into the new week for IWM, as the session opened lower & proceeded to decline -1.74% & meeting the support of the 10 day moving average (briefly breaking down below it) on some of the highest volume of the week.

While some may attribute this to profit taking, it seems a bit lopsided compared to the volumes of the week & a half prior’s run up & should be viewed with a skeptical eye.

Tuesday the ship continued to sink, as the session opened on a gap down beneath the 10 day moving average’s support & closed as a hanging man candle (bearish).

Volume was noticeably weaker than the previous day’s, however the emphasis here should be placed on the fact that the session opened up with all faith in the 10 DMAs support level obliterated.

Wednesday followed suit, opening on a gap down again & despite showing some bulls had entered the chat (upper shadow) the bears were still in control, forcing the session to almost test the support of the 50 day moving average beneath it.

Bulls were able to rush in & force the close to be in the top ~33% of the day’s range though, and there was a lot of shares trading hands compared to most of the rest of October based on their “high” volume.

The dim outlook continued into Thursday, when the session opened higher, tested higher & then proceeded to retrace over 50% of the prior day’s range & ultimately closed below its opening price, indicating weakness & poor spirits among market participants given the low volume of the day.

Friday the bandaid was ton off, as a high volume for the week session resulted in a bearish engulfing candle that sat almost perfectly between the resistance of the 10 DMA & support of the 50 DMA.

Every part of Friday’s candle eclipsed Thursday’s, leading to the oscillator readings mentioned above & the curling over of their 10 day moving average’s resistance which looks set to apply downward pressure on IWM’s price.

While we’ve noted in past weeks that IWM’s volume has not taken as big of a hit as the other major three index ETFs, volume & the direction it occurs in will still be very telling about the next direction IWM takes in the coming weeks & should be paid close attention to.

Much like SPY & QQQ, the relationship between price & the 10 & 50 day moving averages will be important to note as well, especially as they’re both also signaling a potential near-term head & shoulders pattern whose left shoulder formed in mid-September.

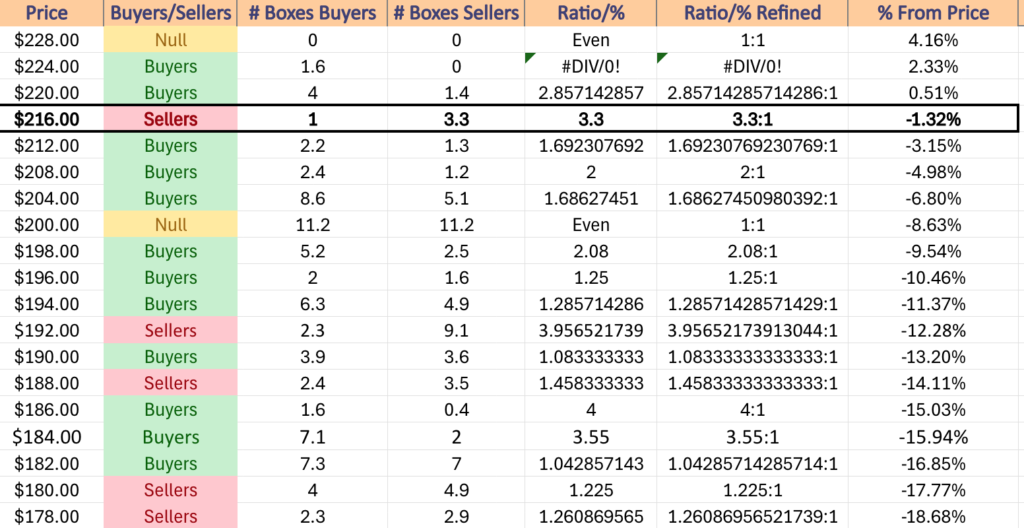

Another thing of note regarding IWM’s 50 DMA’s support is that should it break down, there are no other touch-points until $210.57/share & the 50 DMA is in s Seller dominated price block (3.3:1).

While the $208 support zone has been dominated by the Buyers 2:1 in recent history & the $210.57/share point is contained in this price block, it may not be the sturdiest of support & should be viewed with caution.

IWM has support at the $217.50 (50 Day Moving Average, Volume Sentiment: Sellers, 3.3:1), $210.57 (Volume Sentiment: Buyers, 2:1), $208.58 (Volume Sentiment: Buyers, 2:1) & $208.47/share (Volume Sentiment: Buyers, 2:1) price levels, with resistance at the $221.69 (Volume Sentiment: Buyers, 2.86:1), $222.57 (10 Day Moving Average, Volume Sentiment: Buyers, 2.86:1), $222.17 (Volume Sentiment: Buyers, 2.86:1) & $227.85/share (Volume Sentiment: Buyers, 1.6:0*) price levels.

IWM ETF’s Price Level:Volume Sentiment Over The Past ~2 Years

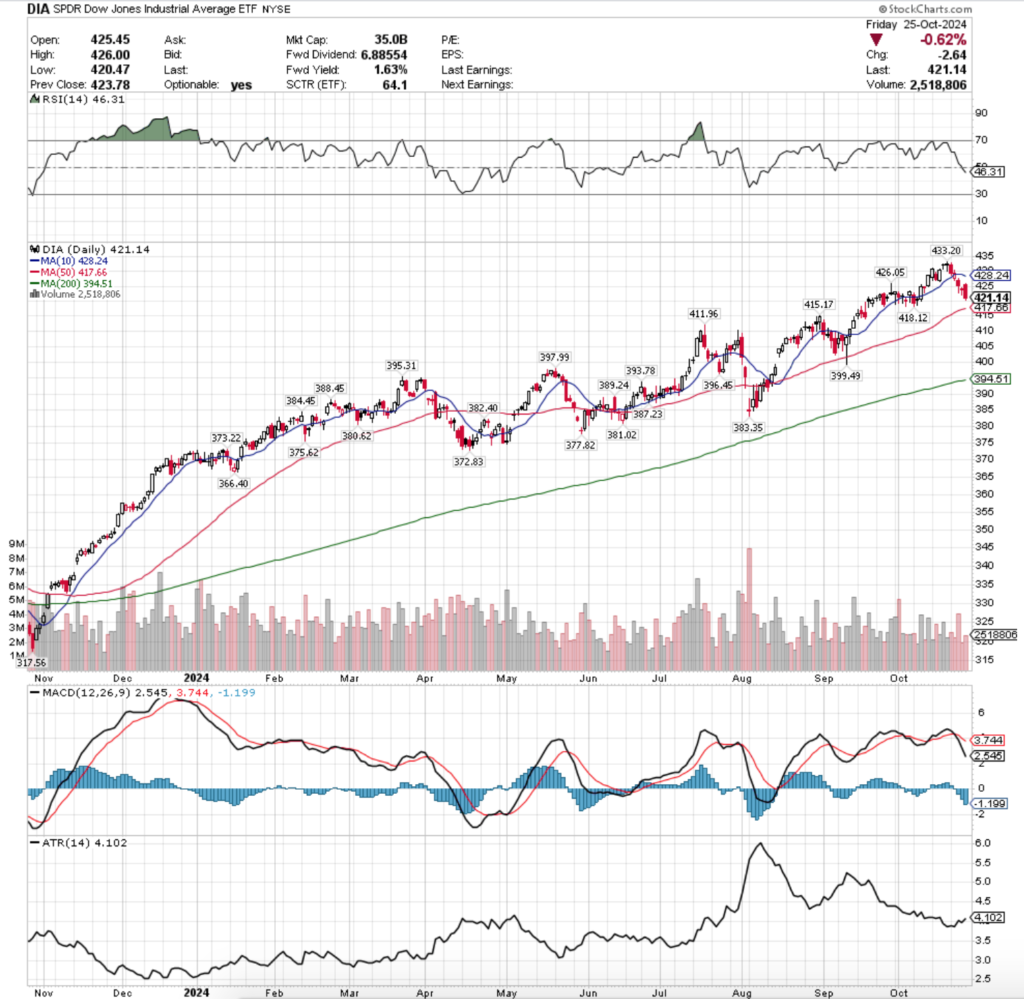

DIA ETF – SPDR Dow Jones Industrial Average ETF’s Technical Performance Over The Past Year

Their RSI also just crossed through the neutral 50 mark & sits currently at 46.31, while their MACD has also been bearish since Wednesday.

Volumes were -22.17% below the previous year’s average (2,696,000 vs. 3,464,048), as investors are even skittish on buying into the blue chip index so close to all-time highs.

The week began & ended on a weak note for DIA following a new all-time high hit on Friday & a pair or dragonfly doji candles closing out the week before.

Monday’s bearish engulfing candle set the stage for a week of pain for DIA, as it started the week off with a test of the support of the 10 day moving average.

While it didn’t break down the support level on Monday, Tuesday gapped lower on the open before turning upwards & closing near in-line with the 10 DMA’s resistance, after briefly breaking through it (upper shadow).

Wednesday the pain got worse, when the week’s highest volume session began with a gap down that ultimately tested -0.96% lower than its opening price during the session, despite bulls managing to step in & for the close to be about midway between the day’s range.

Thursday the sad song continued for DIA, as it opened on a gap lower & closed as a hanging man candle (bearish).

Friday the trend remained alive & well, as the session declined -0.62% on a bearish engulfing candle, setting this week up for more bearish performance from the looks of things.

DIA also has the same head & shoulders pattern appearing from mid-September as SPY, QQQ & IWM have & their oscillators & moving averages are also beginning to show this forming.

Keep an eye on their volume in the coming weeks, particularly which direction it appears to be moving in as that will lead prices.

Like the three aforementioned ETFs, the coming week will also be marked by where DIA’s price winds up in relation to their 10 & 50 DMAs, which as you can see looking at their chart will likely be what causes the H&S pattern to form based on the current layout.

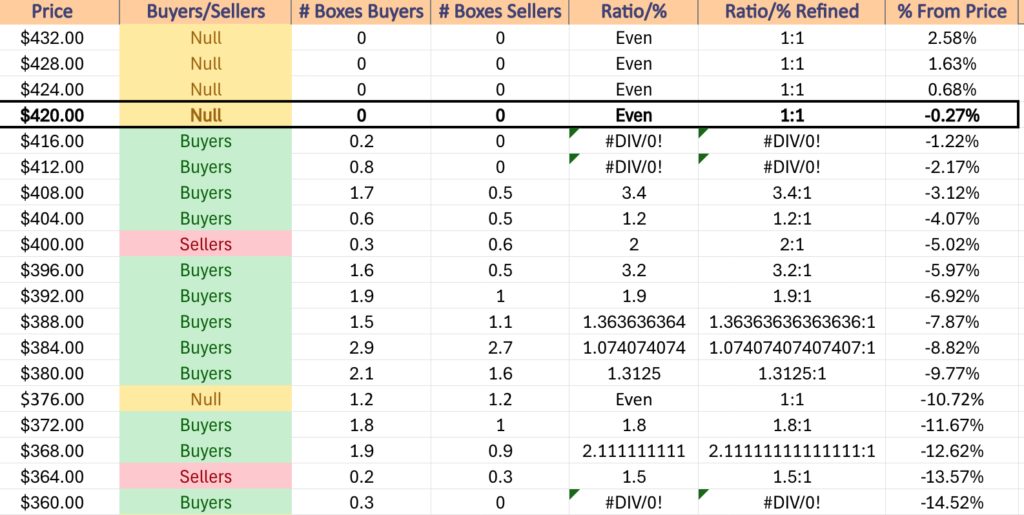

DIA has support at the $418.12 (Volume Sentiment: Buyers, 0.2:0*), $417.66 (Volume Sentiment: Buyers, 0.2:0*), $415.17 (Volume Sentiment: Buyers, 0.8:0*) & $411.96/share (Volume Sentiment: Buyers, 3.4:1) price levels, with resistance at the $426.05 (Volume Sentiment: NULL, 0:0*), $428.24 (10 Day Moving Average, Volume Sentiment: NULL, 0:0*) & $433.20/share (All-Time High, Volume Sentiment: NULL, 0:0*) price levels.

DIA ETF’s Price Level:Volume Sentiment Over The Past ~3 Years

The Week Ahead

Monday there are no major U.S. Economic Data Reports or Fed Speakers.

Acadia Realty Trust, Bank of Hawaii, CenterPoint Energy, Hope Bancorp, ON Semiconductor, PROCEPT BioRobotics & SJW all report earnings before Monday’s opening bell, followed by Agilysys, Amkor, Atlas Energy Solutions, Boot Barn Holdings, Brixmor Property, Brown & Brown, Cadence Design, Calix Networks, Camping World, Capital Southwest, CCC Intelligent Solutions, COPT Defense Properties, Crane, CVR Energy, Douglas Dynamics, Element Solutions, Encompass Health, F5 Networks, Flowserve, Ford Motor, Harmonic, Inari, Kforce, Kilroy Realty, Leggett & Platt, LTC Properties, NorthWestern, PotlatchDeltic, Rambus, Regency Centers, Safehold, SBA Communications, Skyline Champion, TransMedics Group, Trex, UFP Industries, Ultra Clean Holdings, V.F. Corp, Waste Management & Welltower after the session’s close.

S&P Case-Shiller Home Price Index (20 Cities) data comes out at 9 am on Tuesday, followed by Consumer Confidence & Job Openings Data at 10 am.

Tuesday kicks off with earnings from American Tower, Armstrong World Industries, Asbury Automotive, ATI Inc., CBIZ, CECO Environmental, Check Point Software, Comcast, Commvault Systems, Corning, CTS Corp, D.R. Horton, DT Midstream, Eagle Materials, Ecolab, Enterprise Products, ESAB Corp., Franklin Electric, Frontier Group Holdings, Graphic Packaging, H&E Equipment, Harmony Biosciences, Hayward Holdings, HNI, Hubbell, Incyte, IPG Photonics, ITT, Janus International Group, JetBlue Airways, Kiniksa Pharmaceuticals, Leidos, Masco, McDonald’s, MSCI, Northwest Bancshares, PayPal Holdings, Pfizer, Phillips 66, PJT Partners, Royal Caribbean, Scorpio Tankers, Shutterstock, SoFi Technologies, Stanley Black & Decker, Sysco, Tenet Healthcare, Xerox & Zebra Technologies, with 10x Genomics, Adtalem Global Education, Advanced Micro Devices, Alignment Healthcare, Allison Transmission, Alphabet, American Homes 4 Rent, Artisan Partners Asset Management, BioMarin Pharmaceutical, BXP, Caesars Entertainment, Cheesecake Factory, Chemed, Chipotle Mexican Grill, Chubb, DaVita, Edison International, Electronic Arts, Enovix, EQT Corp., Essex Property, Exelixis, ExlService, Expand Energy, Extra Space Storage, First Commonwealth, First Solar, FirstEnergy, FMC Corp, Huron Consulting, IDEX Corp, Ingevity, Landstar System, Littelfuse, Meritage Homes, Mirion Technologies, Modine Manufacturing, Mondelez International, NerdWallet, O-I Glass, ONEOK, Park Hotels & Resorts, PROS Holdings, Provident Financial Services, Qorvo, Reddit, Republic Services, SAGE Therapeutics, Skyward Specialty Insurance Group, Snap, STAG Industrial, Stryker, Udemy, UMB Financial Corp, Unisys, Unum Group, Varonis Systems, Visa, W.P. Carey, Werner Enterprises & Zurn Elkay Water Solutions scheduled to report after the closing bell.

Wednesday kicks off with ADP Employment data at 8:15 am, with GDP, Advanced U.S. Trade Balance in Goods, Advanced Retail Inventories & Advanced Wholesale Inventories data at 8:30 am.

AbbVie, AerCap, AFC Gamma, Allete, Ares Capital, Arvinas, Automatic Data Processing, Avanos Medical, Avnet, Axalta Coating Systems, Bausch + Lomb, Bausch Health, Biogen, Blackbaud, Brinker International, Bunge, Caterpillar, CDW, Chefs’ Warehouse, Clean Harbors, Clearway Energy, Columbus McKinnon, Curbline Properties, Dana, Eli Lilly, Exelon, Extreme Networks, Fiverr, Flex, Fortive, Garmin, Gates Industrial, GE HealthCare, Gentherm, Gibraltar Industries, GlaxoSmithKline, Global Payments, Group 1 Auto, Healthcare Realty, Hess, Hess Midstream Partners, Humana, Illinois Tool Works, IMAX, InMode, Intra-Cellular Therapies, JinkoSolar, Kirby, Kraft Heinz, Leonardo DRS, LivaNova, Martin Marietta, Materion, Monro Muffler, Navient, Neurocrine Biosciences, NiSource, NovoCure, Oil States, Omnicell, OneMain Holdings, OneSpaWorld, Option Care Health, Oshkosh, Otis Worldwide, Parsons, ProPetro, Reynolds Consumer Products, Shake Shack, Silgan Holdings, SiteOne Landscape Supply, Stepan, Terex, The Vita Coco Company, Tradeweb Markets, Trane, TTM Technologies, United Therapeutics, Verisk Analytics, Vulcan Materials, Wingstop, XPO & Zimmer Biomet are all scheduled to report earnings before Wednesday’s opening bell, followed by Meta Platforms, Acadia Healthcare, Advanced Energy, Aflac, Albany International, Alkami Technology, Allegiant Travel, Allstate, Alphatec, Altair Engineering, American Water Works, Amgen, Antero Midstream, Antero Resources, Arch Capital, Arcosa, AXIS Capital, Axos Financial, Beacon Roofing Supply, Benchmark Electronics, Bio-Rad Labs, Booking Holdings, C.H. Robinson, Cactus, Carvana, Casella Waste, CF Industries, Clorox, Cognex, Cognizant Technology Solutions, Coinbase Global, Columbia Sportswear, Compass Diversified, Comstock, Confluent, CONMED, Corcept Therapeutics, Credit Acceptance, Curtiss-Wright, Custom Truck One Source, DoorDash, eBay, Employers Holdings, Energy Recovery, Envista, EPR Properties, Equinix, Equity Residential, Ethan Allen, Etsy, Everest Group, Federal Realty, Floor & Decor, FormFactor, Four Corners Property Trust, FTAI Aviation, Gen Digital, GoDaddy, Green Brick Partners, Hanover Insurance, Herbalife Nutrition, Hercules Capital, Houlihan Lokey, Hub Group, Independence Realty Trust, Informatica, Invitation Homes, iRhythm, KLA Corporation, Lemonade, LPL Financial, Magnolia Oil & Gas, Manitowoc, Matson, MediaAlpha, Merit Medical, MetLife, MGM Resorts, Microsoft, MicroStrategy, Mid-America Apartment Communities, Mister Car Wash, Monolithic Power, Murphy USA, MYR Group, National Storage Affiliates, NETGEAR, New Mountain Finance, Nextracker, NV5 Global, Omega Health, Paramount Group, Paycom Software, Paylocity, Penumbra, Pilgrim’s Pride, PriceSmart, Procore Technologies, Prudential, Public Storage, Remitly Global, Riot Platforms, Robinhood Markets, Roku, Root, Inc., Rush Enterprises, Rush Street Interactive, Ryan Specialty Group, Silicon Motion, Sleep Number, Sprouts Farmers Market, SPX Technologies, STAAR Surgical, Starbucks, Stem, Sturm Ruger, Summit Materials, Sunnova Energy, Teekay Tankers, Teladoc, Tenable, Trupanion, Twilio, UDR, Universal Display, Ventas, Warrior Met Coal, Watts Water Technologies & WillScot Mobile Mini after the closing bell.

Personal Income, Personal Spending, PCE Index, PCE (Year-over-Year), Core PCE Index, Core PCE (Year-over-Year) & Initial Jobless Claims data are all released Thursday morning at 8:30 am, followed by Pending Home Sales data at 10 am.

Thursday morning’s earnings calls include 1-800-FLOWERS, Agios Pharmaceuticals, Allegro Microsystems, Alnylam Pharma, Altria, Alumis, Ametek, APi Group, Aptiv, Arrow Electronics, Avient, Ball Corp, Bandwidth, BCE Inc, Belden, BorgWarner, Bristol Myers Squibb, California Water Service, Canada Goose, Canadian Natural Resources, Cheniere Energy, Cinemark, CMS Energy, ConocoPhillips, Cullen/Frost, Donnelley Financial, Driven Brands, Dun & Bradstreet, Eaton, Ecovyst, EMCOR Group, Entergy, Enviri Corporation, Estee Lauder, Federal Signal, Ferrari, First Majestic Silver, Fresh Del Monte, Generac, Genesis Energy, Gildan Activewear, Grainger, Granite Construction, Green Plains, HF Sinclair, Huntington Ingalls, Hyatt Hotels, IdaCorp, IDEXX Labs, Inhibrx Biosciences, Insperity, International Paper, Intercontinental Exchange, InterDigital, IQVIA, Itron, Janus Henderson Group, Kellanova, Kimco Realty, Kontoor Brands, Kymera Therapeutics, Lancaster Colony, Laureate Education, Lazard, LendingTree, Li Auto, Lightspeed, Lincoln Electric, Lincoln National, Linde, Madrigal Pharmaceuticals, Malibu Boats, Mastercard, Merck, MGP Ingredients, Mobileye Global, Norwegian Cruise Line, Open Text, Organon, Patrick Industries, PBF Energy, Peabody Energy, Peloton Interactive, PHINIA, Quanta Services, Radware, Regeneron Pharmaceuticals, Roblox, SharkNinja, SolarWinds, Southern, STMicroelectronics, SunCoke Energy, TC Energy, Teleflex, The Cigna Group, Trinity Industries, Uber Technologies, Uniti Group, Upbound Group, Utz Brands, Vontier, WEC Energy Group, Wendy’s, Willis Towers Watson, Xcel Energy & Xylem, with Amazon.com, Apple, ACCO Brands, Agnico-Eagle Mines, Alliant Energy, Amcor, Ardelyx, Asure Software, Atlassian, BJ Restaurants, Camden Property, CNO Financial, Cohu, Concentra Group Holdings Parent, Coterra Energy, CubeSmart, Customers Bancorp, Dorman Products, Eastman Chemical, El Pollo Loco, Fox Factory Holding, Grid Dynamics, Halozyme Therapeutics, ICF International, Ingersoll-Rand, Intel, Juniper Networks, Lemaitre Vascular, MasTec, Mercer International, Onto Innovation, Quaker Chemical, Reinsurance Group of America, Sabra Health Care REIT, Select Medical, SkyWest, SM Energy, Sonoco Products, Tennant, U.S. Steel, Verra Mobility, Viavi, VICI Properties & Vir Biotechnology reporting after the closing bell.

Friday morning brings us U.S. Employment Report, U.S. Unemployment Rate, U.S. Hourly Wages & Hourly Wages Year-over-Year data at 8:30 am, followed by S&P final U.S. Manufacturing PMI data at 9:45 am, Construction Spending & ISM Manufacturing data at 10 am & Auto Sales data.

Alpha Metallurgical Resources, ArcBest, Ares Management, BrightSpring Health Services, Cardinal Health, Cboe Global Markets, Chart Industries, Charter Communications, Chevron, Church & Dwight, DigitalBridge, Dominion Energy, Enbridge, Essent Group, Exxon Mobil, fuboTV, Imperial Oil, Interface, LyondellBasell, Magna, Moog, nVent Electric, Pediatrix Medical Group, PPL Corp, Protolabs, RBC Bearings, Simon Properties, T. Rowe Price, Telus, TXNM Energy, TXNM Energy & Wayfair are all scheduled to report earnings before Friday’s opening bell.

See you back here next week!

*** I DO NOT OWN SHARES OR OPTIONS CONTRACT POSITIONS IN SPY, QQQ, IWM OR DIA AT THE TIME OF PUBLISHING THIS ARTICLE ***

The VIX closed at 20.33, indicating an implied one day move of +/-1.28% & an implied one month move of +/-5.88% for the S&P 500.

Highest Technical Rated S&P 500 Components Per 10/25/2024’s Close:

1 -PLTR

2 – UAL

3 – VST

4 – TSLA

5 – NVDA

6 – IRM

7 – AXON

8 – CEG

9 – RCL

10 – CBRE

Lowest Technical Rated S&P 500 Components Per 10/25/2024’s Close:

1 – MRNA

2 – DLTR

3 – DG

4 – ENPH

5 – WBA

6 – GPC

7 – HUM

8 – SMCI

9 – ELV

10 – EL

Highest Volume Rated S&P 500 Components Per 10/25/2024’s Close:

1 – TPR

2 – MHK

3 – DECK

4 – DLR

5 – PFG

6 – HCA

7 – NEM

8 – RMD

9 – WDC

10 – DXCM

Lowest Volume Rated S&P 500 Components Per 10/25/2024’s Close:

1 – MPC

2 – WYNN

3 – JBL

4 – FDX

5 – VTRS

6 – DELL

7 – HST

8 – VST

9 – EXR

10 – SJM

Highest Technical Rated ETFs Per 10/25/2024’s Close:

1 – TSLR

2 – TSLL

3 – NVDX

4 – NVDU

5 – NVDL

6 – TSLT

7 – TSL

8 – JNUG

9 – YINN

10 – AGQ

Lowest Technical Rated ETFs Per 10/24/2024’s Close:

1 – TSLZ

2 – TSDD

3 – TSLQ

4 – NVDQ

5 – NVD

6 – YANG

7 – MRNY

8 – NVDS

9 – JDST

10 – SSG

Highest Volume Rated ETFs Per 10/25/2024’s Close:

1 – PBJA

2 – EQLS

3 – PBAU

4 – FPAG

5 – BSJV

6 – HYKE

7 – ULE

8 – INFR

9 – HFGO

10 – PSDM

Lowest Volume Rated ETFs Per 10/25/2024’s Close:

1 – SECR

2 – MSTI

3 – XHYF

4 – NBCT

5 – MAGG

6 – SZNE

7 – NUSB

8 – USIN

9 – BHYB

10 – DWAW

Highest Technical Rated General Stocks Per 10/25/2024’s Close:

1 – DRUG

2 – CHSN

3 – MNPR

4 – PRKR

5 – BASA

6 – DOGZ

7 – CAPR

8 – GEVO

9 – AZ

10 – TVGN

Lowest Technical Rated General Stocks Per 10/25/2024’s Close:

1 – CETX

2 – ADTX

3 – MRNS

4 – WTO

5 – MMATQ

6 – TCBP

7 – PEGY

8 – BSLK

9 – BYU

10 – MULN

Highest Volume Rated General Stocks Per 10/25/2024’s Close:

1 – OUT

2 – SLG

3 – MAMA

4 – ARBB

5 – NWTN

6 – LINK

7 – ITRM

8 – SGBX

9 – UPXI

10 – WAFU

Lowest Volume Rated General Stocks Per 10/25/2024’s Close:

1 – ALPIB

2 – GASXF

3 – XCUR

4 – AIRRF

5 – CTXXF

6 – DTEGF

7 – SMAGF

8 – MCVT

9 – DSNY

10 – CHXMF

*** THE LIST ABOVE IS STRICTLY FOR INFORMATIONAL PURPOSES – I MAY OR MAY NOT HAVE OR INITIATE A LONG, SHORT, OR LONG/SHORT POSITION IN ANY NAME ABOVE AT ANY TIME ***

The VIX closed at 19.08, indicating an implied one day move of +/-1.20% & an implied one month move of +/-5.51% for the S&P 500.

Highest Technical Rated S&P 500 Components Per 10/24/2024’s Close:

1 – UAL

2 – PLTR

3 – VST

4 – CEG

5 – RCL

6 – NVDA

7 – AXON

8 – CBRE

9 – TRGP

10 – IRM

Lowest Technical Rated S&P 500 Components Per 10/24/2024’s Close:

1 – MRNA

2 – ENPH

3 – DLTR

4 – DG

5 – WBA

6 – GPC

7 – SMCI

8 – HUM

9 – ELV

10 – INTC

Highest Volume Rated S&P 500 Components Per 10/24/2024’s Close:

1 – NEM

2 – MOH

3 – TER

4 – WST

5 – TXT

6 – COO

7 – UPS

8 – IBM

9 – LH

10 – CBRE

Lowest Volume Rated S&P 500 Components Per 10/24/2024’s Close:

1 – DELL

2 – CRWD

3 – SMCI

4 – PODD

5 – VST

6 – MRO

7 – SW

8 – ORCL

9 – EPAM

10 – GLW

Highest Technical Rated ETFs Per 10/24/2024’s Close:

1 – NVDU

2 – NVDX

3 – NVDL

4 – JNUG

5 – TSLR

6 – TSLL

7 – UTSL

8 – TSLT

9 – YINN

10 – TSL

Lowest Technical Rated ETFs Per 10/24/2024’s Close:

1 – TSLZ

2 – TSDD

3 – TSLQ

4 – NVD

5 – NVDQ

6 – YANG

7 – MRNY

8 – JDST

9 – NVDS

10 – SSG

Highest Volume Rated ETFs Per 10/24/2024’s Close:

1 – GENM

2 – UDI

3 – PBJA

4 – QCON

5 – WBIY

6 – DYNI

7 – AGGS

8 – NZUS

9 – TRTY

10 – PBAU

Lowest Volume Rated ETFs Per 10/24/2024’s Close:

1 – PSMR

2 – MIG

3 – SBND

4 – SECR

5 – UCRD

6 – CBLS

7 – SHUS

8 – PAB

9 – JUNZ

10 – GVUS

Highest Technical Rated General Stocks Per 10/24/2024’s Close:

1 – DRUG

2 – MNPR

3 – CHSN

4 – BASA

5 – PRKR

6 – DOGZ

7 – TWG

8 – CAPR

9 – GEVO

10 – AZ

Lowest Technical Rated General Stocks Per 10/24/2024’s Close:

1 – MRNS

2 – CETX

3 – UAVS

4 – MMATQ

5 – WTO

6 – BYU

7 – SLXN

8 – VMAR

9 – GSIW

10 – TCBP

Highest Volume Rated General Stocks Per 10/24/2024’s Close:

1 – NXU

2 – TC

3 – CCTG

4 – OUT

5 – LGCB

6 – VEEE

7 – MNPR

8 – MRNS

9 – QLGN

10 – QNCX

Lowest Volume Rated General Stocks Per 10/24/2024’s Close:

1 – LIANY

2 – DBLVF

3 – BTSGU

4 – WHTCF

5 – FTBYF

6 – SEEL

7 – OCG

8 – ZCMD

9 – PT

10 – PROC

*** THE LIST ABOVE IS STRICTLY FOR INFORMATIONAL PURPOSES – I MAY OR MAY NOT HAVE OR INITIATE A LONG, SHORT, OR LONG/SHORT POSITION IN ANY NAME ABOVE AT ANY TIME ***

NUGT, the Direxion Daily Gold Miners Index Bull 2x Shares ETF has advanced +83.13% over the past year, adding +151.32% since their 52-week low in February of 2024, while resting -4.12% below their 52-week high set on October 22, 2024 (all figures ex-distributions).

In addition to exposure to gold miners, NUGT also offers international exposure to Canada, The U.S., Australia, South Africa, China, The U.K., Peru & Jersey.

Some of their largest holdings include Newmont Corporation (NEM), Agnico Eagle Mines Ltd. (AEM), Barrick Gold (GOLD), Wheaton Prescious Metals Corporation (WPM), Franco Nevada (FNV), Gold Fields (GFI), Zijin Mining H (ZIJMF), Northern Star Resources (NSTYY), Kinross Gold (KGC) & Anglogold (AU).

Below is a brief technical analysis of NUGT, as well as a price level:volume sentiment analysis of the price levels NUGT has traded at over the 1-2 years.

Included in this data is also their recent support & resistance levels so that readers can gain insight into how strong/weak these support/resistance levels may be in the future, based on past investor behavior.

It is not intended to serve as financial advice, but rather as an additional tool to reference while performing your own due diligence on NUGT.

Technical Analysis Of NUGT, The Direxion Daily Gold Miners Index Bull 2x Shares ETF

NUGT ETF – Direxion Daily Gold Miners Index Bull 2x Shares ETF’s Technical Performance Over The Past Year

Their RSI has just dipped back below the overbought level of 70 & sits currently at 66.78, while their MACD is still bullish, but their histogram is beginning to signal that their uptrend may be weakening in the short-term.

Volumes were -27.38% below average over the past week & a half compared to the year prior’s average (1,710,051.25 vs. 2,354,801.93) as market participants began to get nervous near their 52-week high, which may be a sign of near-term profit taking on the horizon after the run up of the past couple of weeks.

Last week began with a retest of NUGT’s 10 day moving average’s support & the session ended in a bearish engulfing candle, giving the green light higher for investors.

It should be noted that this occurred on the lowest volume of the month though, likely as market participants were unsure if it would be able to remain above the support level or not & so they patiently awaited confirmation.

Tuesday opened higher, tested lower about midway through Monday’s trading range, before running higher & closing near the highs of the day on somewhat stronger volume than Monday, but still nothing to write home about compared to the average volume of the rest of the year.

Wednesday opened on a gap higher & tested above the $54/share mark, but closed with a hint of uncertainty & doubt as the spinning top candle’s real body was concentrated near the lower range of the day’s candlestick & it closed lower than it opened.

Volumes were much higher Wednesday, which was also a function of profit taking from the past week’s run up & the bears forcing the higher end of the day’s range to near the bottom of the candlestick to close below the open.

There was still more appetite for risk on Thursday however, as the session opened on a gap higher & while it wasn’t able to close above the $54/share mark it did test above it, but again, the session resulted in a spinning top candle as there was a great deal of uncertainty about the current NUGT valuation.

Volumes dipped day-over-day, but remained strong compared to the other days’ volumes that were noted above.

Friday the risk-on theme continued with another opening gap up that briefly tested lower before powering above the $58/share price level & closing just beneath it at $57.90/share, a day-over-day gain of +7.96% on the strongest volume seen since mid-September.

Warning signals began flashing this past Monday though, as the session opened on a gap higher to $59.50, went up to $60.19/share, before NUGT’s price collapsed to close below the open at $58.06/share.

Volume on Monday was just below that of Friday’s session, likely attributed to the day’s wide trading range & the profit taking that forced the close to be lower than the open as the gap up was unable to muster up much strength.

Tuesday opened higher & pushed up to reach the new 52-week high of $60.74 before closing at $60.40 & the low volume indicated that there was trouble on the horizon for NUGT as investors had finally seemed to have had enough risk.

This lead to yesterday’s-3.68% decline that began as a gap down that attempted to break above Tuesday’s low, but ultimately the bears took over & the price began deflating.

The size of the lower shadow indicates that there was a bit of downside appetite that market participants were interested in, but the bulls were able to force the close higher.

The lack of volume though is signaling that perhaps there is more downside appetite in the tank, particularly given how overextended the past few weeks’ run up has become.

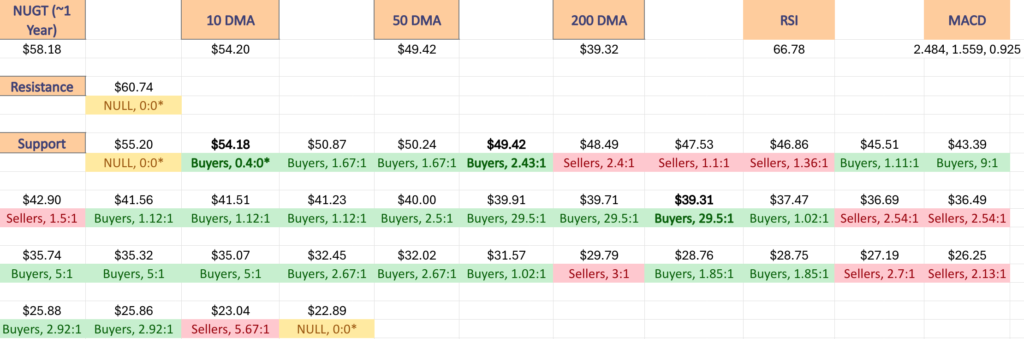

In the coming week(s) the $55.20 support level will be an area of interest to keep an eye on, as it is the nearest support level to last night’s close.

After that investors will want to focus their attention on the support of the 10 day moving average, which will continue moving higher as days pass.

Should the 10 DMA’s support not hold up, the next support level is -6.4% away (using last night’s closing prices).

Another area to keep a keen eye on this upcoming week or two is NUGT’s volume levels, as any advances will require strong volume for confirmation at these high price levels & the strength of any declines/consolidation ranges will also be evident based on market paricipation.

It is also important to explain that when reading tables in the next section that the data should be treated as a barometer that measures Buyer:Seller pressure (or Seller:Buyer).

Due to the jumpy nature described above of NUGT’s recent advances (and declines when you look at their chart before the run up described above) there are many “Buyer” dominated zones that have either a “0” in the denominator for Seller pressure, and other ratios that are near these price extremes.

With that said, when reading the data, the $54-$54.99-price level has a 0 in the denominator due to lack of downside testing in this range compared to advancing volume.

$53-53.99/share has 1.66:1 Buyers:Sellers, which can be seen as a more sturdy support level until the $54-$54.99 level is more thoroughly tested.

Similarly, based on historic behavior of the past 1-2 years the $49-49.99/share price level is considered more sturdy support than the others as it is currently Buyer dominated at a rate of 2.43:1.

Conversely, the $48-48.99/share Seller zone is considered weaker support than the Seller zones that follow it due to the strength of its ratio.

Again, this data is for informational purposes & can be used to aid your existing due diligence process, but it is not intended to serve as financial advice.

Price Level:Volume Sentiment Analysis For NUGT, The Direxion Daily Gold Miners Index Bull 2x Shares ETF

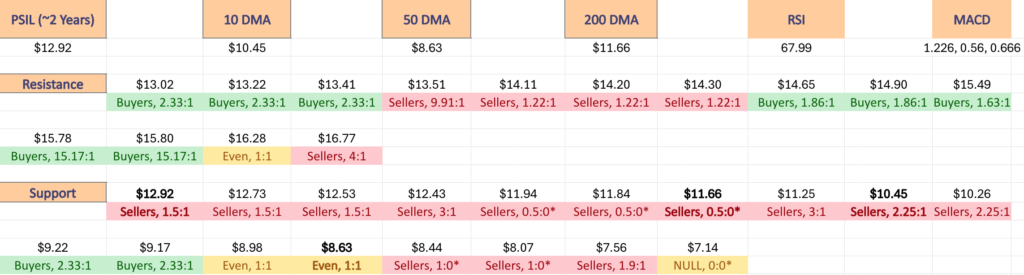

The top table below shows the support & resistance levels of NUGT from the past year’s chart, as well as their price level:volume sentiment at each, using Wednesday 10/23/24’s closing price.

The moving averages are denoted with bold.

The next charts show the volume sentiment at each individual price level NUGT has traded at over the past 1-2 years.

Beneath them is a copy & pasteable list of the same data, where the support/resistance levels are denoted in bold.

All ratios with “0” in the denominator are denoted with a “*”.

NULL values are price levels that had limited trading volume, whether it be due to gaps, quick advances or they are at price extremes; in the event that they are retested & there is more data they would have a distinct “Buyers”, “Sellers” or “Even” title.

This is not intended as financial advice, but rather another tool to consider when performing your own research & due diligence on NUGT ETF.

NUGT ETF’s Price Level:Volume Sentiment Over The Past 1-2 Years At Support & Resistance Levels

NUGT ETF’s Price Level:Volume Sentiment Over The Past 1-2 Years

Price Level:Volume Sentiment For NUGT ETF Over The Past 1-2 Years

Price Level:Volume Sentiment For NUGT ETF Over The Past 1-2 Years

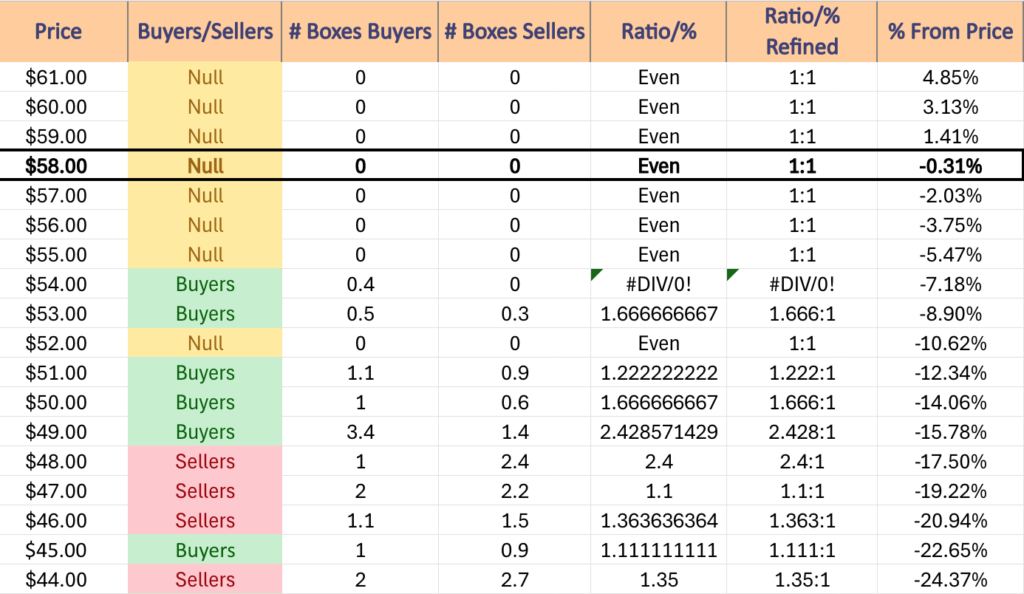

$61 – NULL – 0:0*, +4.85% From Current Price Level

$60 – NULL – 0:0*, +3.13% From Current Price Level

$59 – NULL – 0:0*, +1.41% From Current Price Level

$58 – NULL – 0:0*, -0.31% From Current Price Level – Current Price Level*

$57 – NULL – 0:0*, -2.03% From Current Price Level

$56 – NULL – 0:0*, -3.75% From Current Price Level

$55 – NULL – 0:0*, -5.47% From Current Price Level

$54 – Buyers – 0.4:0*, -7.18% From Current Price Level – 10 Day Moving Average*

$53 – Buyers – 1.67:1, -8.9% From Current Price Level

$52 – NULL – 0:0*, -10.62% From Current Price Level

$51 – Buyers – 1.22:1, -12.34% From Current Price Level

$50 – Buyers – 1.67:1, -14.06% From Current Price Level

$49 – Buyers – 2.43:1, -15.78% From Current Price Level – 50 Day Moving Average*

$48 – Sellers – 2.4:1, -17.5% From Current Price Level

$47 – Sellers – 1.1:1, -19.22% From Current Price Level

$46 – Sellers – 1.36:1, -20.94% From Current Price Level

$45 – Buyers – 1.11:1, -22.65% From Current Price Level

$44 – Sellers – 1.35:1, -24.37% From Current Price Level

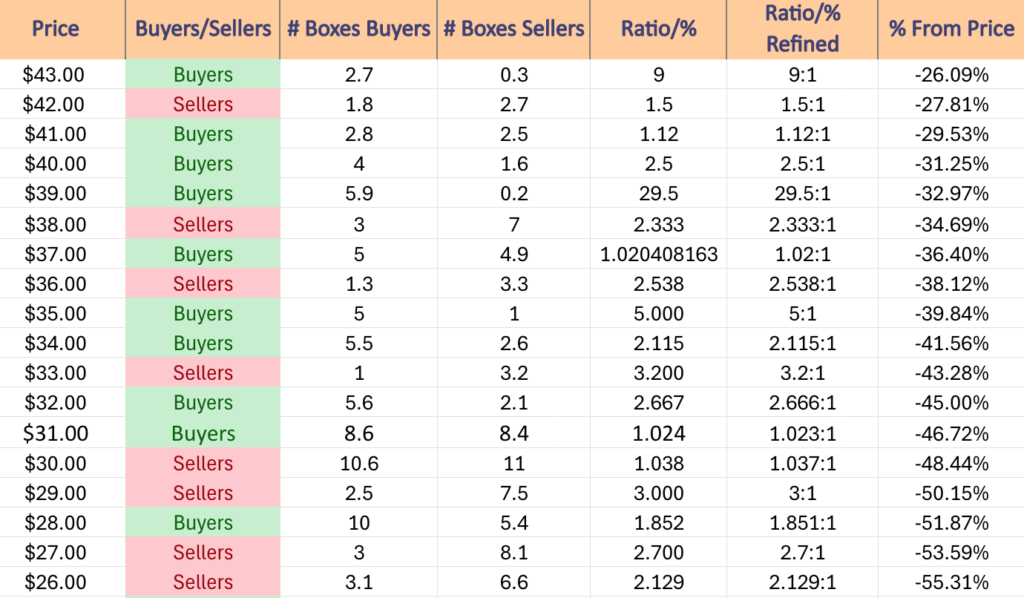

$43 – Buyers – 9:1, -26.09% From Current Price Level

$42 – Sellers – 1.5:1, -27.81% From Current Price Level

$41 – Buyers – 1.12:1, -29.53% From Current Price Level

$40 – Buyers – 2.5:1, -31.25% From Current Price Level

$39 – Buyers – 29.5:1, -32.97% From Current Price Level – 200 Day Moving Average*

$38 – Sellers – 2.33:1, -34.69% From Current Price Level

$37 – Buyers – 1.02:1, -36.4% From Current Price Level

$36 – Sellers – 2.54:1, -38.12% From Current Price Level

$35 – Buyers – 5:1, -39.84% From Current Price Level

$34 – Buyers – 2.12:1, -41.56% From Current Price Level

$33 – Sellers – 3.2:1, -43.28% From Current Price Level

$32 – Buyers – 2.67:1, -45% From Current Price Level

$31 – Buyers – 1.02:1, -46.72% From Current Price Level

$30 – Sellers – 1.04:1, -48.44% From Current Price Level

$29 – Sellers – 3:1, -50.15% From Current Price Level

$28 – Buyers – 1.85:1, -51.87% From Current Price Level

$27 – Sellers – 2.7:1, -53.59% From Current Price Level

$26 – Sellers – 2.13:1, -55.31% From Current Price Level

$25 – Buyers – 2.92:1, -57.03% From Current Price Level

$24 – Buyers – 2.18:1, -58.75% From Current Price Level

$23 – Seller s- 5.67:1, -60.47% From Current Price Level

$22 – NULL – 0:0*, -62.19% From Current Price Level

*** I DO NOT OWN SHARES OR OPTIONS CONTRACT POSITIONS IN NUGT AT THE TIME OF PUBLISHING THIS ARTICLE ***

The VIX closed at 19.24 indicating an implied one day move of +/-1.21% & an implied one month move of +/-5.56%.

Highest Technical Rated S&P 500 Components Per 10/23/2024’s Close:

1 – UAL

2 – VST

3 – PLTR

4 – CEG

5 – AXON

6 – NVDA

7 – RCL

8 – IRM

9 – TRGP

10 – NEM

Lowest Technical Rated S&P 500 Components Per 10/23/2024’s Close:

1 – MRNA

2 – ENPH

3 – DLTR

4 – DG

5 – WBA

6 – SMCI

7 – MOH

8 – ELV

9 – HUM

10 – CNC

Highest Volume Rated S&P 500 Components Per 10/23/2024’s Close:

1 – MCD

2 – CSGP

3 – ENPH

4 – STX

5 – BSX

6 – NTRS

7 – ODFL

8 – MOH

9 – GPC

10 – LH

Lowest Volume Rated S&P 500 Components Per 10/23/2024’s Close:

1 – SMCI

2 – MNST

3 – NCLH

4 – GWW

5 – EPAM

6 – DELL

7 – BR

8 – VTRS

9 – COR

10 – BAX

Highest Technical Rated ETFs Per 10/23/2024’s Close:

1 – NVDU

2 – NVDL

3 – NVDX

4 – JNUG

5 – UTSL

6 – NUGT

7 – YINN

8 – AGQ

9 – GDMN

10 – XPP

Lowest Technical Rated ETFs Per 10/23/2024’s Close:

1 – NVDQ

2 – NVD

3 – YANG

4 – MRNY

5 – JDST

6 – NVDS

7 – FXP

8 – GXLM

9 – DUST

10 – SSG

Highest Volume Rated ETFs Per 10/23/2024’s Close:

1 – NBCT

2 – INNO

3 – NPFI

4 – TOK

5 – FDM

6 – NUGO

7 – DYLG

8 – FVC

9 – SPTB

10 – KCE

Lowest Volume Rated ETFs Per 10/23/2024’s Close:

1 – OPTZ

2 – SECR

3 – KWT

4 – MAGG

5 – GVUS

6 – PSMJ

7 – SHUS

8 – MSTI

9 – FDTB

10 – NUSB

Highest Technical Rated General Stocks Per 10/23/2024’s Close:

1 – DRUG

2 – CHSN

3 – PRKR

4 – CAPR

5 – GNPX

6 – GEVO

7 – PHUN

8 – DOGZ

9 – SEVCF

10 – TWG

Lowest Technical Rated General Stocks Per 10/23/2024’s Close:

1 – CETX

2 – ADTX

3 – UAVS

4 – MURGY

5 – WTO

6 – MULN

7 – SEEL

8 – ZCAR

9 – EGRX

10 – OMEX

Highest Volume Rated General Stocks Per 10/23/2024’s Close:

1 – LRHC

2 – EEIQ

3 – SLG

4 – OUT

5 – DBVT

6 – UAVS

7 – KWE

8 – CNSP

9 – VRAX

10 – ANRO

Lowest Volume Rated General Stocks Per 10/23/2024’s Close:

1 – GASXF

2 – YELLQ

3 – FLMMF

4 – CBDBY

5 – PDPTF

6 – SFES

7 – PGTK

8 – MISVF

9 – LBSR

10 – SVT

*** THE LIST ABOVE IS STRICTLY FOR INFORMATIONAL PURPOSES – I MAY OR MAY NOT HAVE OR INITIATE A LONG, SHORT, OR LONG/SHORT POSITION IN ANY NAME ABOVE AT ANY TIME ***

NAIL, the Direxion Daily Homebuilders & Supplies Bull 3x Shares ETF has had an impressive year, advancing +238.29% while gaining +245.85% since their 52-week low set in October of 2023 & sits currently -20.18% below their 52-week high from October 18, 2024 (all figures ex-distributions).

NAIL provides investors with 3x levered exposure to the homebuilders & home building supplies industry, which have had a very strong past year as shown by their past year’s performance.

Some of NAIL’s largest holdings include D.R. Horton (DHI), Lennar Corporation (LEN), NVR (NVR), Pultegroup (PHM), Lowe’s Companies Inc. (LOW), Home Depot (HD), Sherwin Williams (SHW), Toll Brothers (TOL), Topbuild Corporation (BLD) & Builders Firstsource (BLDR).

Below is a brief technical analysis of NAIL, as well as a price level:volume sentiment analysis of the price levels NAIL has traded at over the past year.

Included in this data is also their recent support & resistance levels so that readers can gain insight into how strong/weak these support/resistance levels may be in the future, based on past investor behavior.

It is not intended to serve as financial advice, but rather as an additional tool to reference while performing your own due diligence on NAIL.

Technical Analysis Of NAIL, The Direxion Daily Homebuilders & Supplies Bull 3x Shares ETF

NAIL ETF – Direxion Daily Homebuilders & Supplies Bull 3x Shares ETF’s Technical Performance Over The Past Year

Their RSI is currently trending towards the oversold level of 30 & sits currently at the 40.04 level, while their MACD crossed over bearishly on Monday & looks to continue downward in the near-term following yesterday’s -10.1% gap down session.

Volumes over the past week & a half have been +15.92% above the prior year’s average (364,430 vs. 314,385.65), as market participants have been eager to take profits following last Friday’s reaching of a new all-time high.

Last Monday NAIL opened on a gap up on very low volume & was able to break out above the 10 day moving average’s resistance & closed the day above it, setting the stage for reaching their new all-time high later in the week.

The low volume on such a large bullish candle did add a hint of skepticism about how strong the move actually was though, as there was not a great deal of participation despite the day’s wide trading range & higher close that resulted.

Tuesday confirmed this, when despite gapping up again on the open (which also is a function of the 3x leverage at play), NAIL continued higher to the $174/share mark before the bears stepped in & forced the closing price down to $167.26 (-3.87% lower from high to close).

It should be noted that the spinning top candle is concentrated near the bottom of the day’s range, indicating that market participants were showing uncertainty in the direction as to where NAIL’s shares should be valued.

Tuesday’s session’s volume was slightly higher than Monday’s, likely due to the profit taking in that 3.87% window after a few days of gains, but it was still relatively low, indicating weakness & a lack of conviction behind the move.

Wednesday opened on another gap up at $171.38 & moved higher, but still closed as a spinning top candle at $174.26, which when paired with the even lower volumes than the prior two days had indicates that investors were on edge & becoming cautious as prices approached their previous all-time high that was set in September.

The end of the line came in sight on Thursday, when the session opened higher & closed lower, resulting in a bearish engulfing candle as investors took profits from the prior days’ gap ups, although at a low rate given the low volume of the day.

The lower shadow on the day’s candle went down to $167.67, indicating that while the bulls were able to step in & force prices higher from there for the day, market participants were growing tired & losing steam.

Friday was the last hurrah for NAIL, as it opened higher & was able to clinch a new all-time high on the highest volume it has seen in weeks, but this proved to be the top of the diving board.

Monday saw volumes that eclipsed Fridays on a declining session that saw NAIL shed -10.17% on the day & smash through the support of the 10 day moving average.

Things got worse on Tuesday, when NAIL gapped down to open below the 50 DMA & lost another -10.1% on even higher volume for the day, as market participants began running towards the exits.

It is important to note as well that in addition to the support of the 50 DMA breaking down that day, the $145.88 & $144.77 support levels were also broken through, leaving the next support level at $137.17, -3.46% below yesterday’s closing price.

After that, the next highest support level is -7.14% below yesterday’s closing level, which might normally sound like a steep decline, but NAIL is 3x leveraged making it less steep of a fall compared to an un-levered ETF.

In the coming week it will be worth keeping an eye on whether or not NAIL can begin to consolidate & form a range off of the recent-20% drop or if it will continue lower to test those next support levels.

If it is able to consolidate keep an eye on the 10 DMA & 50 DMA as they approach the price to see how they influence it higher or lower.

Another key area to watch will be their volume, as it will lend clues into what their next direction may be.

If there is an uptick in advancing volume then there may be some strength to force another run upwards, but if prices continue to move in the low volume trends that marked much of October (minus the last three days & 10/4/24) then caution should be taken moving forward as the lack of participation should be viewed as a lack of confidence in the price moves.

It should also be noted that broader indexes have been showing signs of weakness in the past week & should they see fallout NAIL will not be exempt – more on that in this week’s market review note.

Price Level:Volume Sentiment Analysis For NAIL, The Direxion Daily Homebuilders & Supplies Bull 3x Shares ETF

The top table below shows the support & resistance levels of NAIL from the past year’s chart, as well as their price level:volume sentiment at each, using Tuesday 10/22/24’s closing price.

The moving averages are denoted with bold.

The next charts show the volume sentiment at each individual price level NAIL has traded at over the past year.

Beneath them is a copy & pasteable list of the same data, where the support/resistance levels are denoted in bold.

All ratios with “0” in the denominator are denoted with a “*”.

NULL values are price levels that had limited trading volume, whether it be due to gaps, quick advances or they are at price extremes; in the event that they are retested & there is more data they would have a distinct “Buyers”, “Sellers” or “Even” title.

This is not intended as financial advice, but rather another tool to consider when performing your own research & due diligence on NAIL ETF.

NAIL ETF’s Price Level:Volume Sentiment Over The Past Year Including Support & Resistance Levels

NAIL ETF’s Price Level:Volume Sentiment Over The Past Year

Price Level:Volume Sentiment For NAIL ETF Over The Past Year

Price Level:Volume Sentiment For NAIL ETF Over The Past Year

NAIL ETF’s Price Level:Volume Sentiment Over The Past Year

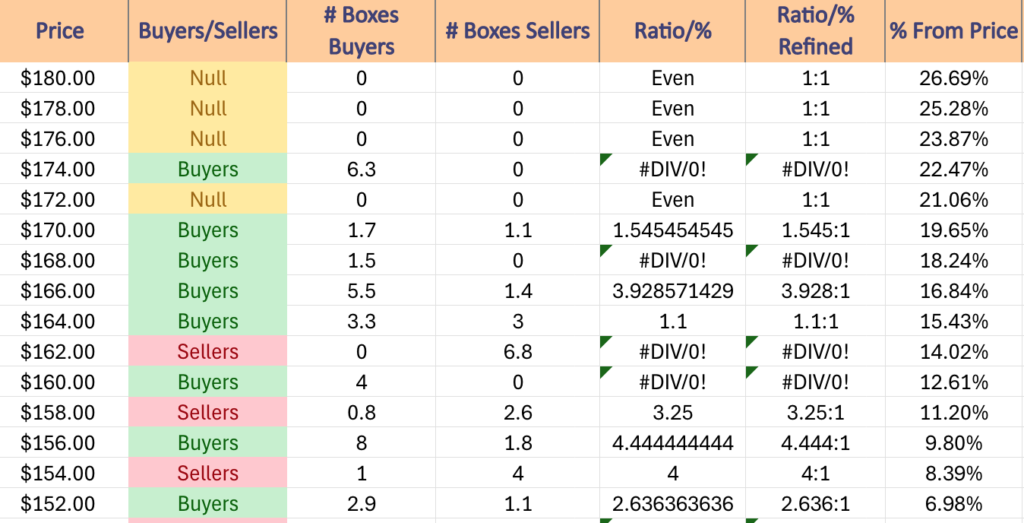

$180 – NULL – 0:0*, +26.69% From Current Price Level

$178 – NULL – 0:0*, +25.28% From Current Price Level – All-Time High*

$176 – NULL – 0:0*, +23.87% From Current Price Level

$174 – Buyers – 6.3:0*, +22.47% From Current Price Level

$172 – NULL – 0:0*, +21.06% From Current Price Level

$170 – Buyers – 1.55:1, +19.65% From Current Price Level

$168 – Buyers – 1.5:0*, +18.24% From Current Price Level

$166 – Buyers – 3.93:1, +16.84% From Current Price Level

$164 – Buyers – 1.1:1, +15.43% From Current Price Level

$162 – Sellers – 6.8:0*, +14.02% From Current Price Level

$160 – Buyers – 4:0*, +12.61% From Current Price Level – 10 Day Moving Average*

$158 – Sellers – 3.25:1, +11.2% From Current Price Level

$156 – Buyers – 4.44:1, +9.8% From Current Price Level

$154 – Sellers – 4:1, +8.39% From Current Price Level

$152 – Buyers – 2.64:1, +6.98% From Current Price Level

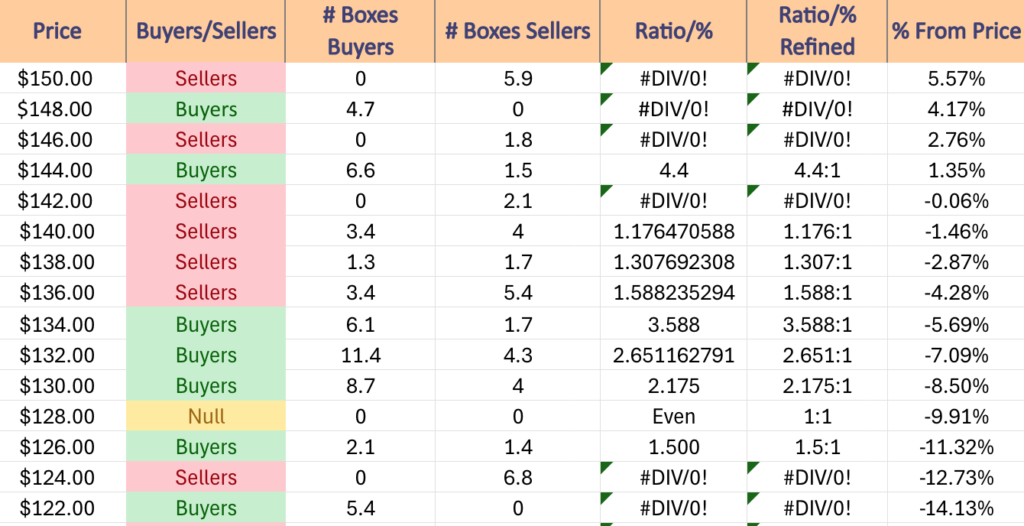

$150 – Sellers – 5.9:0*, +5.57% From Current Price Level – 50 Day Moving Average*

$148 – Buyers – 4.7:0*, +4.17% From Current Price Level

$146 – Sellers – 1.8:0*, +2.76% From Current Price Level

$144 – Buyers – 4.4:1, +1.35% From Current Price Level

$142 – Sellers 2.1:0*, -0.06% From Current Price Level – Current Price Block*

$140 – Sellers – 1.18:1, -1.46% From Current Price Level

$138 – Sellers – 1.31:1, -2.87% From Current Price Level

$136 – Seller s- 1.59:1, -4.28% From Current Price Level

$134 – Buyers – 3.59:1, -5.69% From Current Price Level

$132 – Buyers – 2.65:1, -7.09% From Current Price Level

$130 – Buyers – 2.18:1, -8.5% From Current Price Level

$128 – NULL – 0:0*, -9.91% From Current Price Level

$126 – Buyers – 1.5:1, -11.32% From Current Price Level

$124 – Sellers – 6.8:0*, -12.73% From Current Price Level

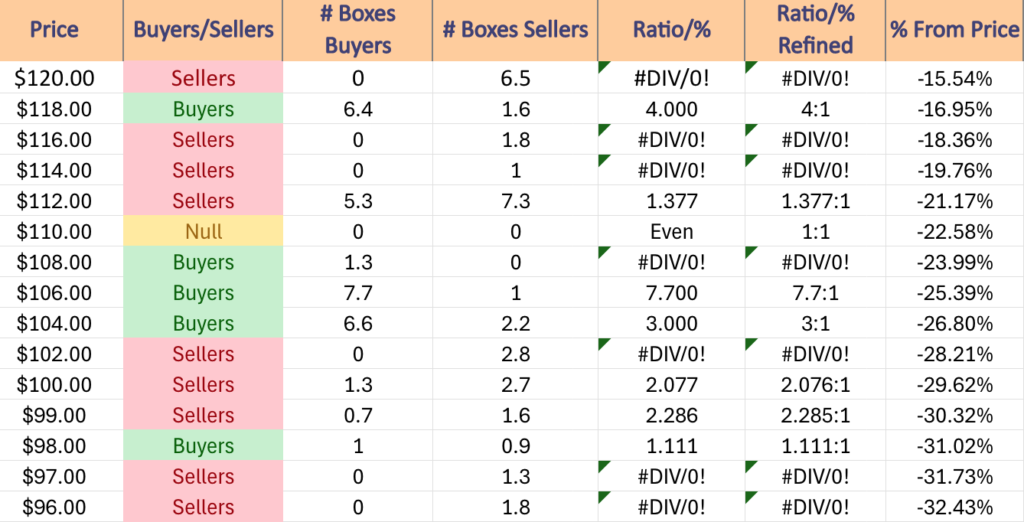

$122 – Buyers – 5.4:0*, -14.13% From Current Price Level – 200 Day Moving Average*

$120 – Sellers – 6.5:0*, -15.54% From Current Price Level

$118 – Buyers – 4:1, -16.95% From Current Price Level

$116 – Sellers – 1.8:0*, -18.36% From Current Price Level

$114 – Sellers – 1:0*, -19.76% From Current Price Level

$112 – sellers – 1.38:1, -21.17% From Current Price Level

$110 – NULL – 0:0*, -22.58% From Current Price Level

$108 – Buyers – 1.3:0*, -23.99% From Current Price Level

$106 – Buyers – 7.7:1, -25.39% From Current Price Level

$104 – Buyers – 3:1, -26.8% From Current Price Level

$102 – Sellers – 2.8:0*, -28.21% From Current Price Level

$100 – Sellers – 2.08:1, -29.62% From Current Price Level

$99 – Sellers – 2.29:1, -30.32% From Current Price Level

$98 – Buyers – 1.11:1, -31.02% From Current Price Level

$97 – Sellers – 1.3:0*, -31.73% From Current Price Level

$96 – Sellers – 1.8:0*, -32.43% From Current Price Level

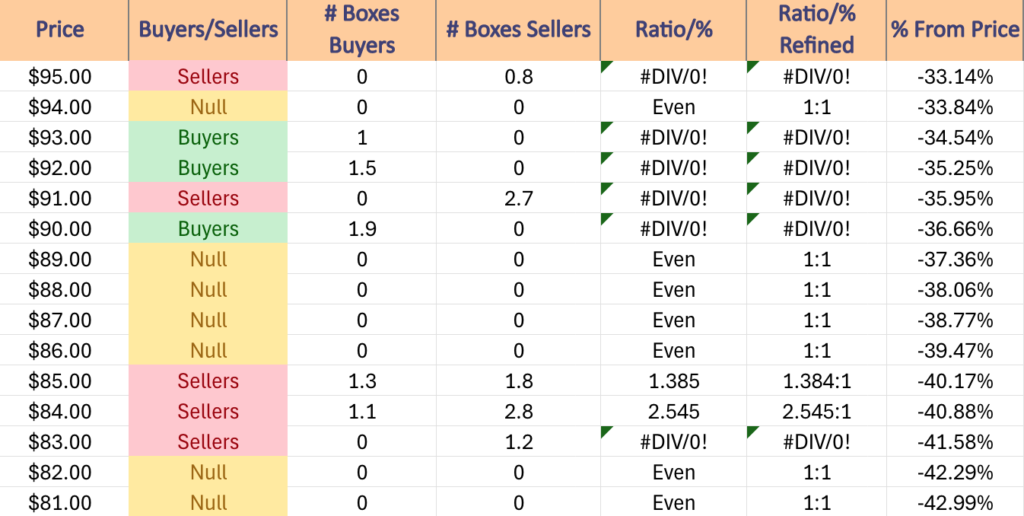

$95 – Sellers – 0.8:0*, -33.14% From Current Price Level

$94 – NULL – 0:0*, -33.84% From Current Price Level

$93 – Buyers – 1:0*, -34.54% From Current Price Level

$92 – Buyers – 1.5:08, -35.25% From Current Price Level

$91 – Sellers – 2.7:0*, -35.95% From Current Price Level

$90 – Buyers – 1.9:0*, -36.66% From Current Price Level

$89 – NULL – 0:0*, -37.36% From Current Price Level

$88 – NULL – 0:0*, -38.06% From Current Price Level

$87 – NULL – 0:0*, -38.77% From Current Price Level

$86 – NULL – 0:0*, -39.47% From Current Price Level

$85 – Sellers – 1.38:1, -40.17% From Current Price Level

$84 – Sellers – 2.55:1, -40.88% From Current Price Level

$83 – Sellers – 1.2:0*, -41.58% From Current Price Level

$82 – NULL – 0:0*, -42.29% From Current Price Level

$81 – NULL – 0:0*, -42.99% From Current Price Level

*** I DO NOT OWN SHARES OR OPTIONS CONTRACT POSITIONS IN NAIL AT THE TIME OF PUBLISHING THIS ARTICLE ***

The VIX closed at 18.2, indicating an implied one day move of +/-1.15% & an implied one month move of +/-5.26% for the S&P 500.

Highest Technical Rated S&P 500 Components Per 10/22/2024’s Close:

1 – UAL

2 – PLTR

3 – VST

4 – NVDA

5 – AXON

6 – CEG

7 – RCL

8 – NCLH

9 – NEM

10 – CCL

Lowest Technical Rated S&P 500 Components Per 10/22/2024’s Close:

1 – MRNA

2 – DLTR

3 – DG

4 – GPC

5 – SMCI

6 – WBA

7 – ELV

8 – HUM

9 – MOH

10 – CNC

Highest Volume Rated S&P 500 Components Per 10/22/2024’s Close:

1 – GPC

2 – SHW

3 – MMM

4 – GE

5 – NUE

6 – GM

7 – PM

8 – DGX

9 – PCAR

10 – REGN

Lowest Volume Rated S&P 500 Components Per 10/22/2024’s Close:

1 – MNST

2 – HSIC

3 – EPAM

4 – INCY

5 – CE

6 – SW

7 – AVGO

8 – INVH

9 – CRWD

10 – DPZ

Highest Technical Rated ETFs Per 10/22/2024’s Close:

1 – NVDX

2 – NVDL

3 – NVDU

4 – JNUG

5 – NUGT

6 – AGQ

7 – YINN

8 – UTSL

9 – GDMN

10 – SILJ

Lowest Technical Rated ETFs Per 10/22/2024’s Close:

1 – NVDQ

2 – NVD

3 – YANG

4 – JDST

5 – MRNY

6 – NVDS

7 – SSG

8 – ZSL

9 – DUST

10 – FXP

Highest Volume Rated ETFs Per 10/22/2024’s Close:

1 – NVBT

2 – PBNV

3 – JUNP

4 – PVI

5 – UAPR

6 – MINN

7 – HYBB

8 – INFR

9 – PBAU

10 – ESMV

Lowest Volume Rated ETFs Per 10/22/2024’s Close:

1 – SECR

2 – IQSM

3 – RAYD

4 – SHDG

5 – SDSI

6 – SHUS

7 – BHYB

8 – RHRX

9 – MCSE

10 – SXQG

Highest Technical Rated General Stocks Per 10/22/2024’s Close:

1 – DRUG

2 – GNPX

3 – SEVCF

4 – DOGZ

5 – GEVO

6 – PRKR

7 – CAPR

8 – TWG

9 – CANB

10 – WLGS

Lowest Technical Rated General Stocks Per 10/22/2024’s Close:

1 – UAVS

2 – ZPTA

3 – ADTX

4 – HPCO

5 – SEEL

6 – PEGY

7 – VMAR

8 – MULN

9 – EDBL

10 – EGRX

Highest Volume Rated General Stocks Per 10/22/2024’s Close:

1 – HIHO

2 – ENSC

3 – OUT

4 – TWO

5 – INDP

6 – NDRA

7 – HYZN

8 – PNBK

9 – CYCC

10 – ULY

Lowest Volume Rated General Stocks Per 10/22/2024’s Close:

1 – ALPIB

2 – SFES

3 – MRZM

4 – WHTCF

5 – BANL

6 – QUISF

7 – NSRCF

8 – PLSDF

9 – XCUR

10 – BCTF

*** THE LIST ABOVE IS STRICTLY FOR INFORMATIONAL PURPOSES – I MAY OR MAY NOT HAVE OR INITIATE A LONG, SHORT, OR LONG/SHORT POSITION IN ANY NAME ABOVE AT ANY TIME ***

PSIL, the AdvisorShares Psychedelics ETF has declined -9.65% over the past year, falling -24% from its 52-week high in March of 2024, while having rebounded +80.95% from its 52-week low set in October of 2024 (all figures ex-distributions).

PSIL ETF is designed to give investors exposure to the growing field of using psychedelics for mental healthcare research.

It also gives exposure to companies in the U.S., Canada, Europe, the U.K. & Australasia for investors looking to get more international exposure in their portfolios.

Some of its top holdings include Mind Medicine Inc. (MNMD), Cybin Inc. (CYBN), Incannex Healthcare Inc. (IXHL), GH Research PLC (GHRS), Alkermes PLC (ALKS), Atai Life Sciences NV (ATAI), Clearminded Medicine Inc. (CMND), Quantum Biopharma LTD. (QNTM), Sage Therapuetics (SAGE) & Relmada Therapuetics (RLMD).

Below is a brief technical analysis of PSIL, as well as a price level:volume sentiment analysis of the price levels PSIL has traded at over the past 2-3 years.

Included in this data is also their recent support & resistance levels so that readers can gain insight into how strong/weak these support/resistance levels may be in the future, based on past investor behavior.

It is not intended to serve as financial advice, but rather as an additional tool to reference while performing your own due diligence on PSIL.

Technical Analysis Of PSIL, The AdvisorShares Psychedelics ETF

PSIL ETF – AdvisorShares Psychedelics ETF’s Technical Performance Over The Past Year

Their RSI is re-approaching the overbought level of 70 for the second time in a week & currently sits at 67.99, while their MACD is still bullish in the wake of last Tuesday’s session where shares jumped +99.49% day-over-day, but the histogram is beginning to wane.

Volumes were +1,891.94% above the prior year’s average over the past six sessions (211,996.67 vs. 10,642.72), mostly due to the major gaining session of 10/15/2024 & the subsequent profit taking/chasing that followed.

Before we get into the last week, PSIL had been in a steady decline for the past seven months, which will be important to keep in mind when we get into the next section.

Last Monday, PSIL began to show signs of life just two days after reaching a fresh 52-week & all-time low price of $7.14/share.

Despite happening on low volume, shares opened on a gap up & ran from an opening price of $7.31/share to the closing & day’s high price of $7.85 (+7.39% open to close gain for the day).

Tuesday also opened on a gap up at $7.99/share & proceeded to run higher on the second highest volume of the year to a high of $15.80 to close just lower at $15.66 for the day.

Given that this close was higher than 98% of their past year’s closing prices there was a great deal of profit taking on Wednesday, when the session opened lower at $15/share, retraced down to $12.80/share but was able to find footing & rally back to close at $13.85/share.

Wednesday naturally had the highest volume of the past year between people taking profits, people cashing out of long-held positions & other market participants trying to jump in & chase after the recent major gains in hopes that prices would continue to rally higher.

Thursday the declines continued, but the volume & day’s range were both much lower & the profit taking began to die down & a new consolidation range began to find footing near the $12.50/share mark.

Friday confirmed that investors were indeed with the $12.50 mark as the session opened slightly below it, before testing up as high as $13.01 (Thursday’s high was $13.02) & settling for the day at $12.63/share.

While the real body of Friday’s candle was focused on the lower third of the day’s range, volume was the third highest of the day as there appears to have been a mix of profit taking & risk-off into the weekend selling on the advancing session.

Monday’s session had glimmers of optimism, but also flashed caution lights for PSIL ETF.

The session opened on a gap higher, tested down to $0.05 lower than Friday’s close before powering higher to close the day +2.3%.

Volumes were above average Monday, but paled in comparison to the preceding five sessions which indicates weakness in sentiment, but the day’s high was $13.04, so there was appetite for higher prices than the prior two sessions.

Something to watch in the coming week is how PSIL moves in relation to broader markets, which look set to experience heightened volatility in the near-term (more on that in this week’s market review note).

If major indexes see major fallout they will not be immune, but they may fare better in the wake of the recent price run up & beginning of a new trading range establishment.

With that in mind, it will be important to have an understanding of how their support levels have previously been treated by market participants.

There are many in the support zone of $12.43-12.92, but if prices break down through that we will not see support again until $11.94-11.84 (pending the 10 day moving average doesn’t get above those levels first, which will depend on how long it takes for said test to play out).

Another key area to watch is the $12.92/share mark, which is yesterday’s closing price & also a support/resistance level from December of 2023.

In the event of upside movement that crosses through that & sets it as a support level, if prices continue up to $13.00/share they enter a Buyer dominated price zone, which may help them find footing to continue climbing.

If they don’t & it serves as resistance then PSIL will be stuck in a Seller dominated zone(s), as shown in the table below.

Before reading the table below, recall the note above of how PSIL had been in steady decline for most of the past seven months.

This would mean that a majority of their past year’s price levels are skewed towards Seller’s being the victorious force at play.

Most of the upside action from that time period came from last Tuesday’s jump, which will not be reflected in each price level’s data.

With that said, when using the ratios below that favor the Sellers, it is important to consider the magnitude of the Sellers:Buyers at each price zone compared to one another.

If a zone has 3:1 Sellers:Buyers & the next zone has only 1.08:1 Sellers:Buyers, it should be inferred that the former is more likely to be weaker than the latter based on historic behavior.

Once these zones have been tested more thoroughly the ratios will even out more & some may even flip to be Buyer dominated.

Again, this is not intended to serve as financial advice, but rather as a barometer of sentiment that can be used with your other due diligence practices.

Price Level:Volume Sentiment Analysis For PSIL, The AdvisorShares Psychedelics ETF

The top table below shows the support & resistance levels of PSIL from the past year’s chart, as well as their price level:volume sentiment at each, using Monday 10/22/24’s closing price.

The moving averages are denoted with bold.

The next charts show the volume sentiment at each individual price level PSIL has traded at over the past 2-3 years.

Beneath them is a copy & pasteable list of the same data, where the support/resistance levels are denoted in bold.

All ratios with “0” in the denominator are denoted with a “*”.

NULL values are price levels that had limited trading volume, whether it be due to gaps, quick advances or they are at price extremes; in the event that they are retested & there is more data they would have a distinct “Buyers”, “Sellers” or “Even” title.

This is not intended as financial advice, but rather another tool to consider when performing your own research & due diligence on PSIL ETF.

Price Level:Volume Sentiment For PSIL, The AdvisorShares Psychedelics ETF Over The Past 2-3 Years

Price Level:Volume Sentiment For PSIL, The AdvisorShares Psychedelics ETF Over The Past 2-3 Years

PSIL, AdvisorShares Psychedelics ETF’s Price Level:Volume Sentiment Over The Past 2-3 Years

PSIL, AdvisorShares Psychedelics ETF’s Price Level:Volume Sentiment Over The Past 2-3 Years

Price Level:Volume Sentiment For PSIL, The AdvisorShares Psychedelics ETF Over The Past 2-3 Years

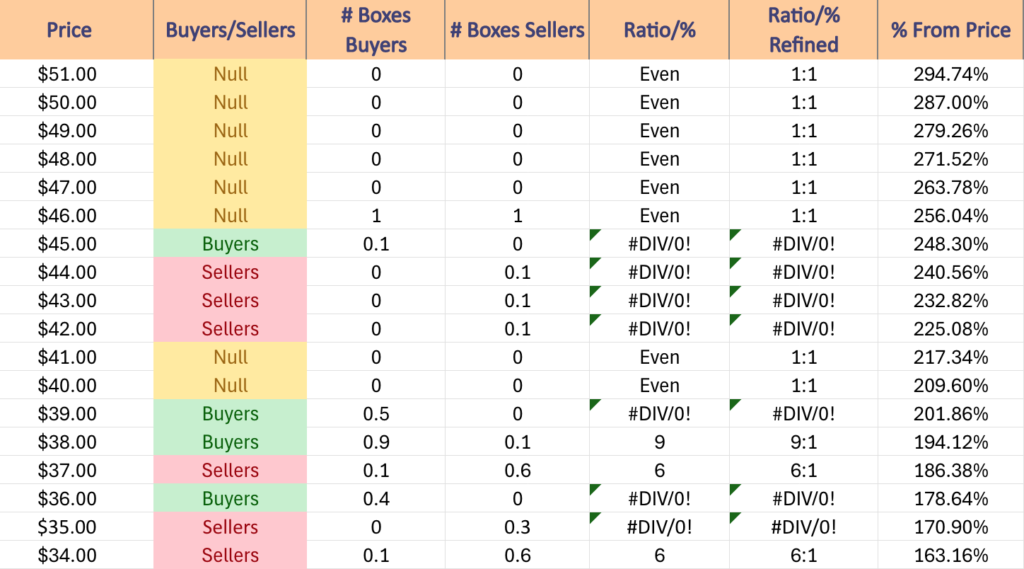

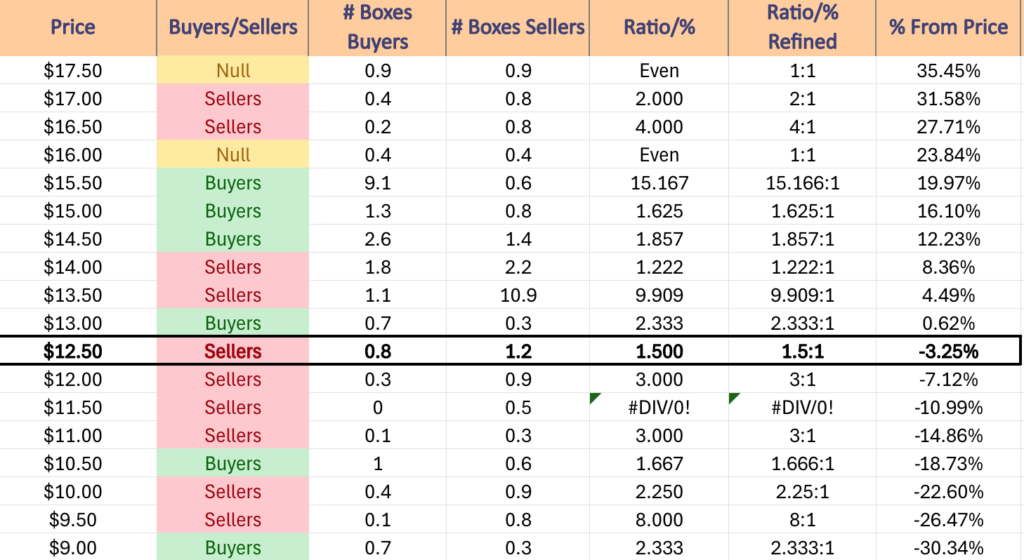

$51 – NULL – 0:0*, +294.74% From Current Price Level

$50 – NULL – 0:0*, +287% From Current Price Level

$49 – NULL – 0:0*, +279.26% From Current Price Level

$48 – NULL – 0:0*, +271.52% From Current Price Level

$47 – NULL – 0:0*, +263.78% From Current Price Level

$46 – Even – 1:1, +256.04% From Current Price Level

$45 = Buyers – 0.1:0*, +248.3% From Current Price Level

$44 – Sellers – 0.1:0*, +240.56% From Current Price Level

$43 – Sellers – 0.1:0*, +232.82% From Current Price Level

$42 – Sellers – 0.1:0*, +225.08% From Current Price Level

$41 – NULL – 0:0*, +217.34% From Current Price Level

$40 – NULL – 0:0*, +209.6% From Current Price Level

$39 – Buyers – 0.5:0*, +201.86% From Current Price Level

$38 – Buyers – 9:1, +194.12% From Current Price Level

$37 – Sellers – 6:1, +186.38% From Current Price Level

$36 – Buyers – 0.4:0*, +178.64% From Current Price Level

$35 – Sellers – 0.3:0*, +170.9% From Current Price Level

$34 – Sellers – 6:1, +163.16% From Current Price Level

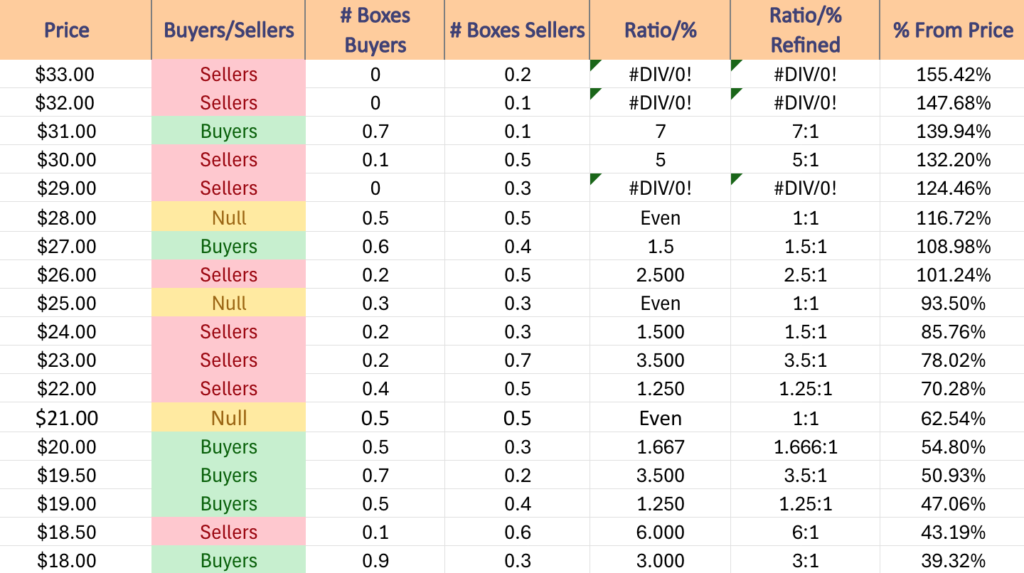

$33 – Seller s- 0.2:0*, +155.42% From Current Price Level

$32 – Sellers – 0.1:0*, +147.68% From Current Price Level

$31 – Buyers – 7:1, +139.94% From Current Price Level

$30 – Sellers – 5:1, +132.2% From Current Price Level

$29 – Sellers – 0.3:0*, +124.46% From Current Price Level

$28 – Even – 1:1, +116.72% From Current Price Level

$27 – Buyers – 1.5:1, +108.98% From Current Price Level

$26 – Sellers – 2.5:1, +101.24% From Current Price Level

$25 – Even – 1:1, +93.5% From Current Price Level

$24 – Sellers – 1.5:1, +85.76% From Current Price Level

$23 – Sellers – 3.5:1, +78.02% From Current Price Level

$22 – Sellers – 1.25:1, +70.28% From Current Price Level

$21 – Even – 1:1, +62.54% From Current Price Level

$20 – Buyers – 1.67:1, +54.8% From Current Price Level

$19.50 – Buyers – 3.5:1, +50.93% From Current Price Level

$19 – Buyers – 1.25:1, +47.06% From Current Price Level

$18.50 – Sellers – 6:1, +43.19% From Current Price Level

$18 – Buyers – 3:1, +39.32% From Current Price Level

$17.50 – Even – 1:1, +35.45% From Current Price Level

$17 – Sellers – 2:1, +31.58% From Current Price Level

$16.50 – Sellers – 4:1, +27.71% From Current Price Level

$16 – Even – 1:1, +23.84% From Current Price Level

$15.50 – Buyers – 15.17:1, +19.97% From Current Price Level

$15 – Buyers – 1.63:1, +16.1% From Current Price Level

$14.50 – Buyers – 1.86:1, +12.23% From Current Price Level

$14 – Sellers – 1.22:1, +8.36% From Current Price Level

$13.50 – Sellers – 9.91:1, +4.49% From Current Price Level

$13 – Buyers – 2.33:1, +0.62% From Current Price Level

$12.50 – Sellers – 1.5:1, -3.25% From Current Price Level – Current Price Block & 10 Day Moving Average**

$12 – Sellers – 3:1, -7.12% From Current Price Level

$11.50 – Sellers – 0.5:0*, -10.99% From Current Price Level – 200 Day Moving Average*

$11 – Sellers – 3:1, -14.86% From Current Price Level

$10.50 – Buyers – 1.67:1, -18.73% From Current Price Level

$10 – Sellers – 2.25:1, -22.6% From Current Price Level

$9.50 – Sellers – 8:1, -26.47% From Current Price Level

$9 – Buyers – 2.33:1, -30.34% From Current Price Level

$8.50 – Even – 1:1, -34.21% From Current Price Level – 50 Day Moving Average*

$8 – Sellers – 1:0*, -38.08% From Current Price Level

$7.50 – Sellers – 1.9:1, -41.95% From Current Price Level

$7 – NULL – 0:0*, -45.82% From Current Price Level

*** I DO NOT OWN SHARES OR OPTIONS CONTRACT POSITIONS IN PSIL AT THE TIME OF PUBLISHING THIS ARTICLE ***