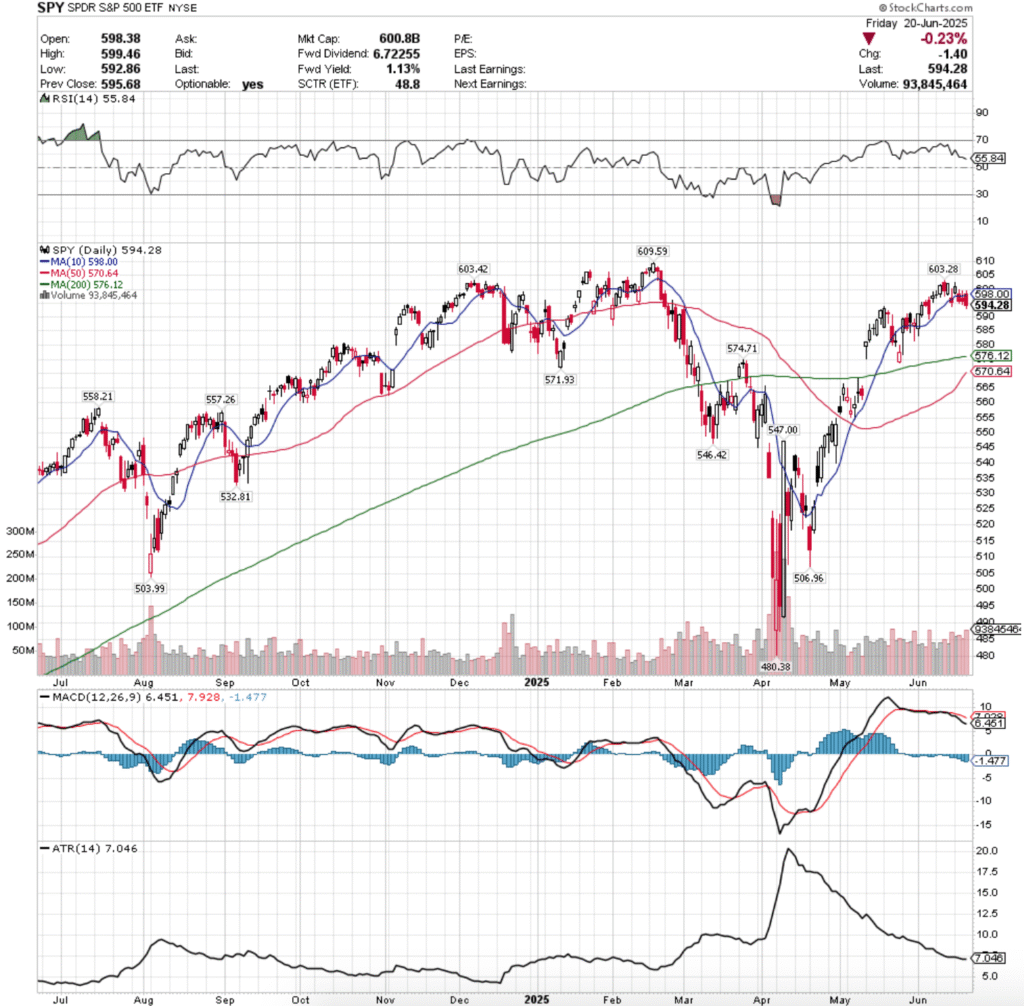

SPY, the SPDR S&P 500 ETF declined -0.46% for the week, while the VIX closed the week at 20.62, indicating an implied one day move of +/-1.3%, and a one month implied move of +/-5.96%.

SPY ETF – SPDR S&P 500 ETF’s Technical Performance Over The Past Year

Their RSI is declining towards the neutral 50-mark & sits current at 55.84, while their MACD is bearish, with the histogram implying that there may be more declines on the near-term horizon.

Volumes were +42.48% higher than the prior year’s average levels (83,212,500 vs. 58,401,952), which is cause for concern given that aside from Monday’s gap up open that caused an advance, the entire holiday week was declining with lower shadows indicating that there is more Seller pressure on the horizon.

Monday the week began on the only advancing session, which is of note due to the rest of the week resulting in declines & it was the third highest volume of the four sessions.

While the week opened on a gap up, the lack of participation was disappointing from a sustainability perspective.

Tuesday the cracks became exposed, opening on a gap down that was unable to break above $599.98/share & ended up breaking down though the support of the 10 day moving average on higher volume than Monday.

Wednesday things got even fisher, as the session produced lower highs & lower lows, forming a bearish harami pattern with Tuesday’s candle on the week’s lowest volume heading into the holiday Thursday & the resistance of the 10 day moving average kept SPY subdued.

Friday’s candle opened on a gap higher, attempted to crack the $600/share level, but ultimately declined forming a bearish engulfing pattern with Wednesday’s session on the highest volume of the week.

The story of this week is going to be focused on Iran, PCE & Powell’s testimony to the House.

To the upside the $603.28-.42/level needs to be broken through to see any type of advances.

This will prove tricky though as like noted last week there is a bearish head & shoulders pattern emerging for SPY that’s shoulders are at those two prices.

There’s going to need to be major, consistent advancing volume in order for that to happen, which should be noted.

The head is the $609.59/share level, which is SPY’s all-time high, and will need a lot of participation to break down.

The consolidation case has SPY oscillating around the 10 day moving average, with perhaps a minor pump when the 50 day moving average crosses through the 200 DMA bullishly, but should that happen there is another, smaller head & shoulders that would form from mid-May’s gap up, leading to the following.

The declining case gets tricky, as there is limited support at SPY’s current price level nearby, which means that there is likely going to be a closing on said window that occurred in mid-May, and the long-term trend line will be tested as support.

In the best case scenario there SPY will oscillate around the 200 DMA awaiting an upside or downside catalyst, but the price level that the 200 DMA resides in is historically Seller oriented, which adds fuel to any declines.

$570.64/share is the current downside target level to watch, but that will change daily as it is the 50 day moving average (Per Friday’s close).

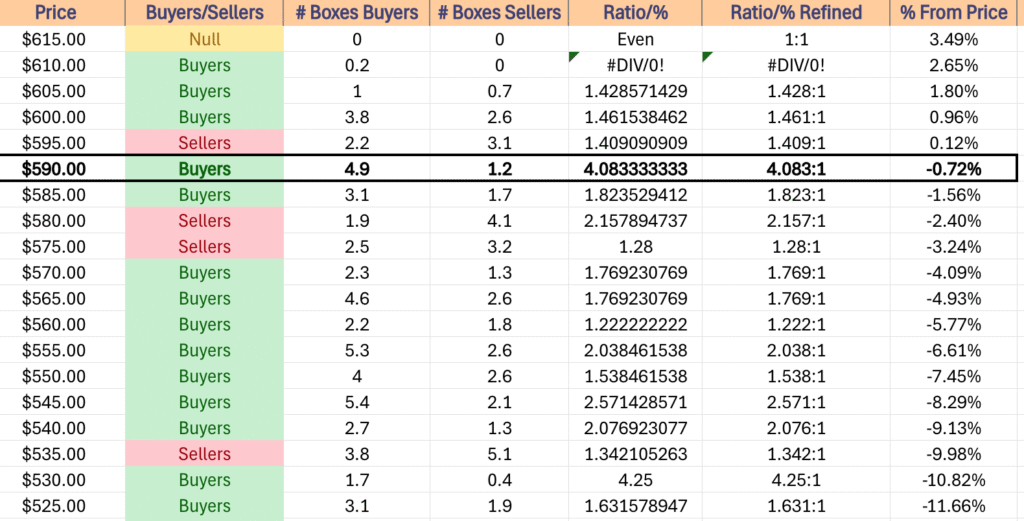

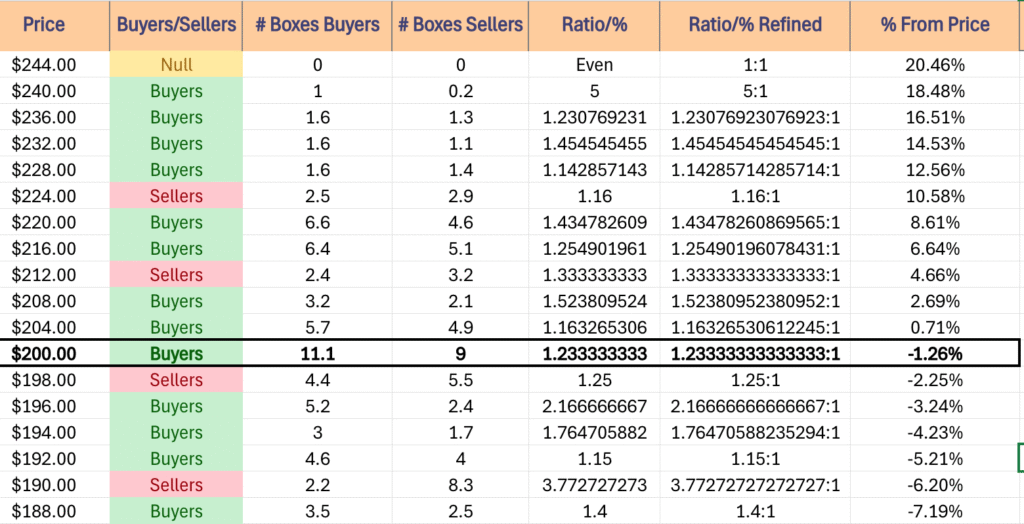

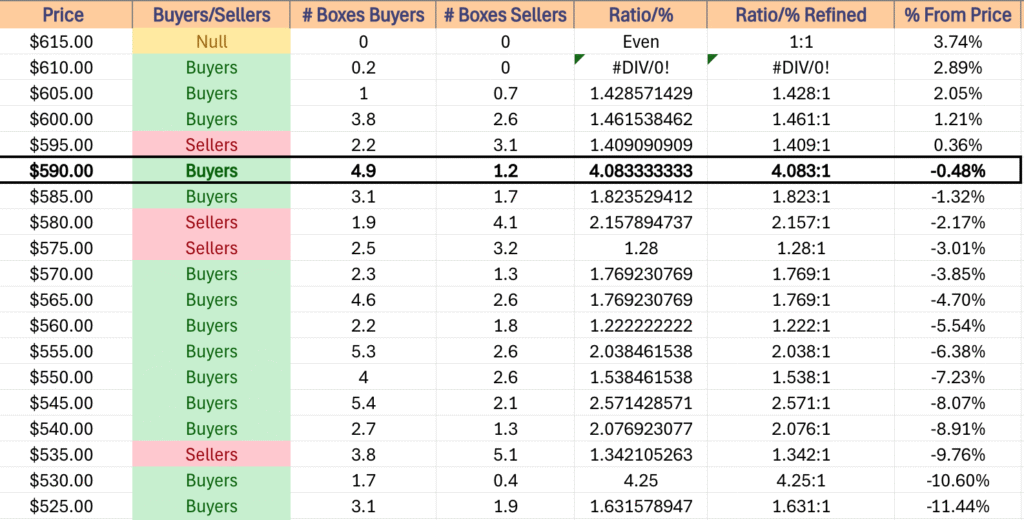

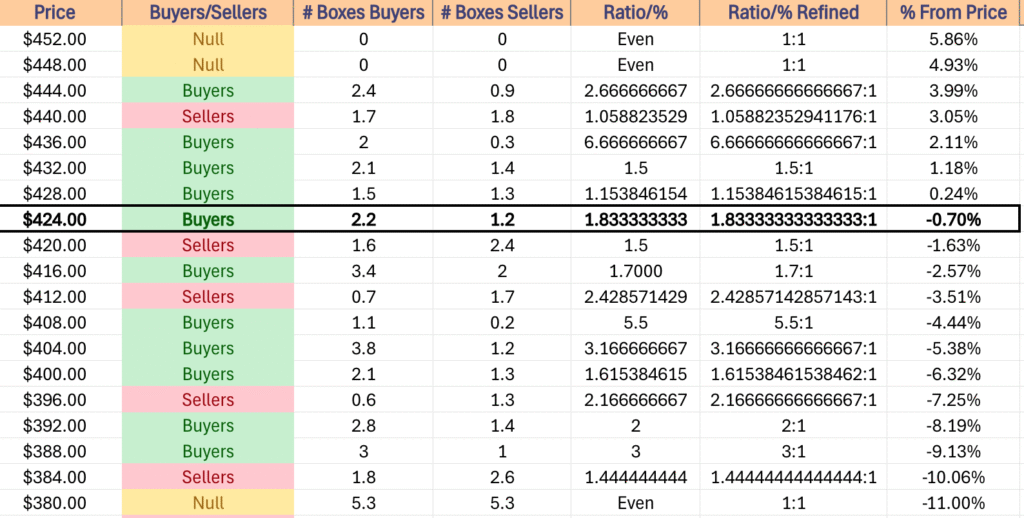

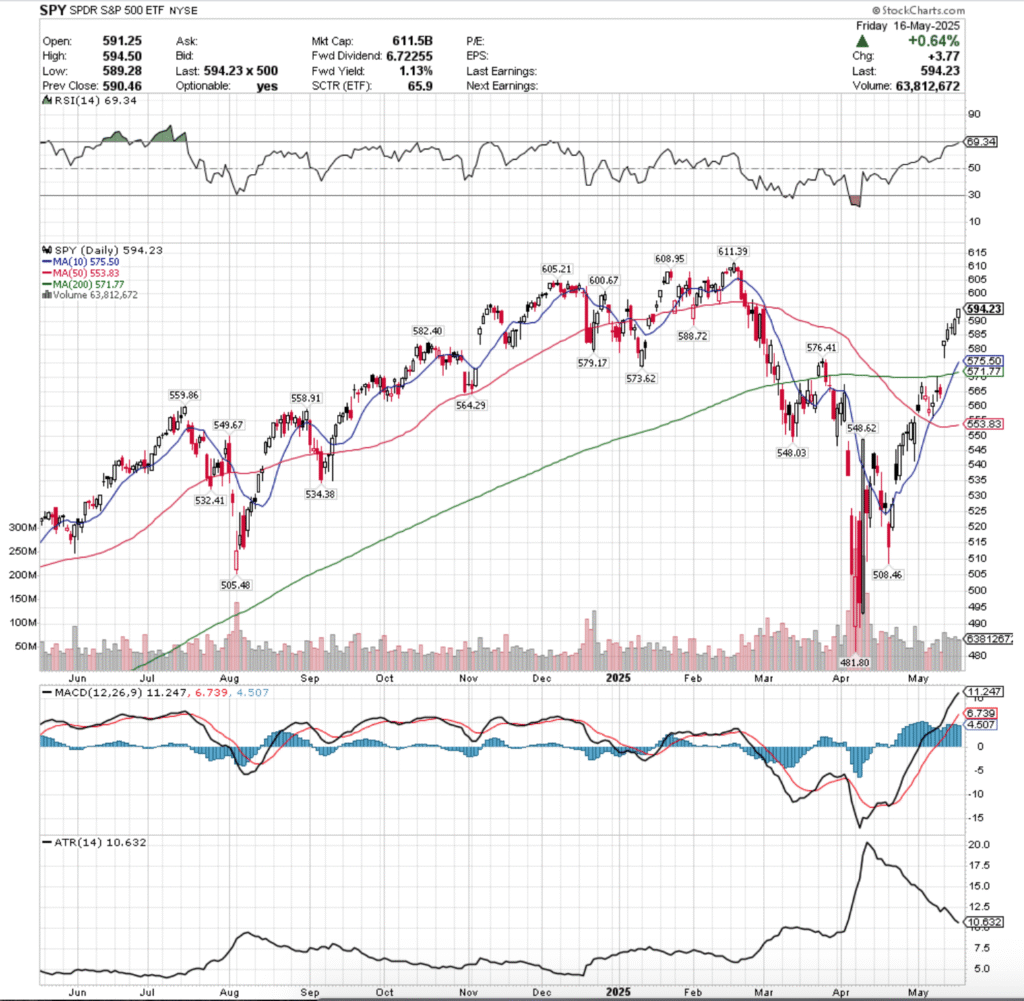

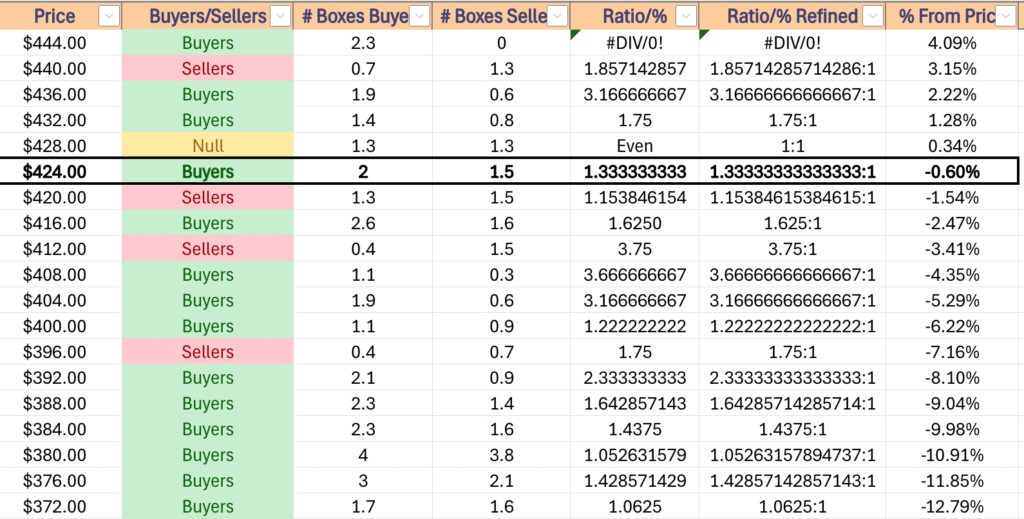

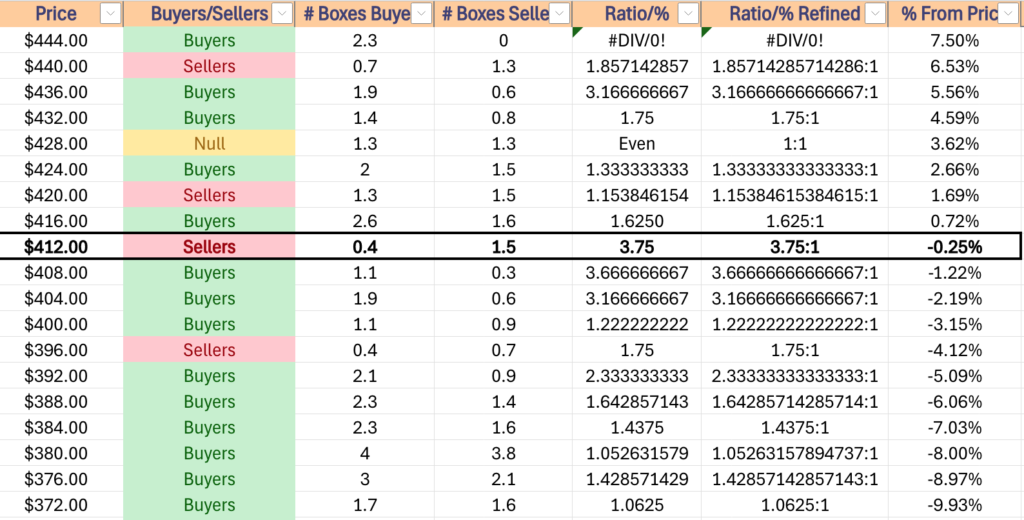

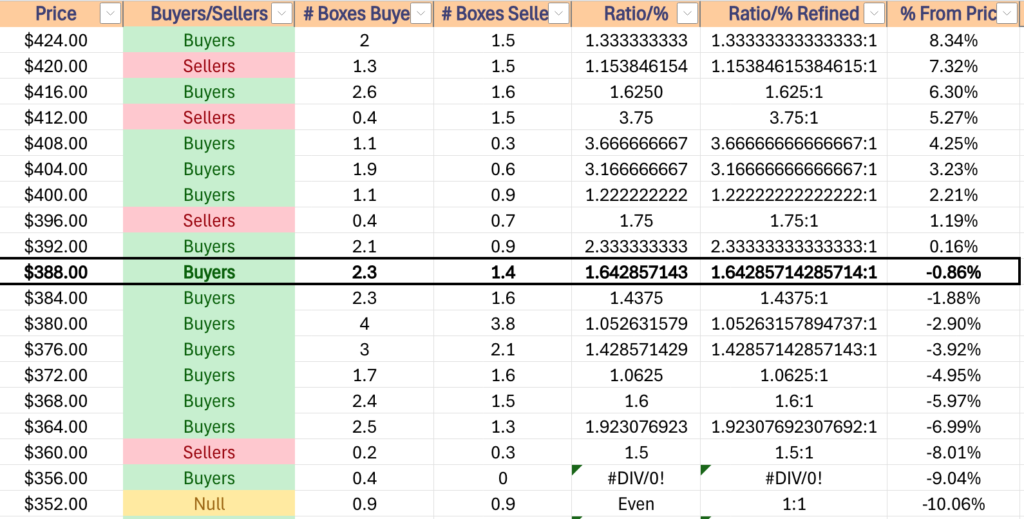

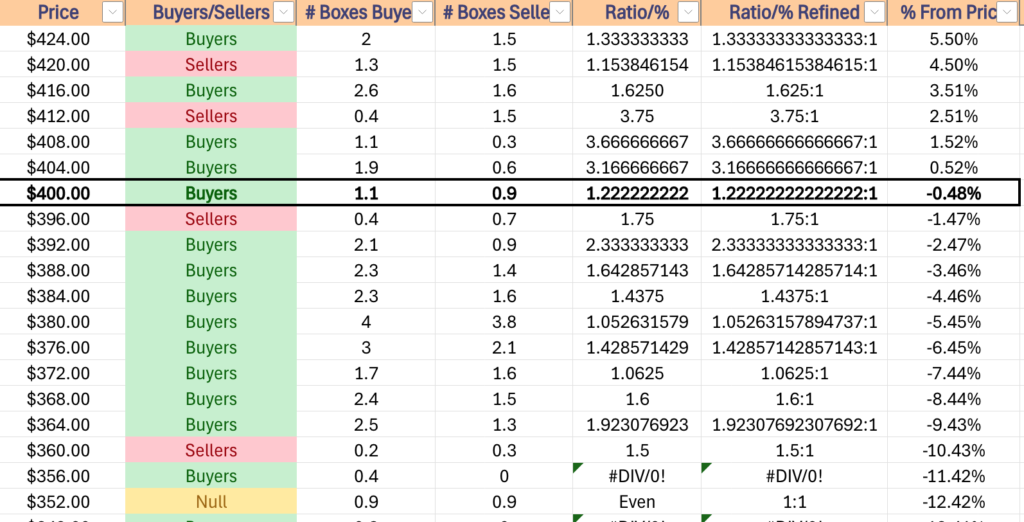

SPY has support at the $576.12 (200 Day Moving Average, Volume Sentiment: Sellers, 1.28:1), $574.71 (Volume Sentiment: Buyers, 1.77:1), $571.93 (Volume Sentiment: Buyers, 1.77:1) & $570.64/share (Volume Sentiment: Buyers, 1.77:1) price levels, with resistance at the $598.00 (Volume Sentiment: Sellers, 1.41:1), $603.28 (Volume Sentiment: Buyers, 1.46:1), $603.42 (Volume Sentiment: Buyers, 1.46:1) & $609.59/share (All-Time High, Volume Sentiment: Buyers, 1.43:1) price levels.

SPY ETF’s Price Level:Volume Sentiment Over The Past ~4 Years

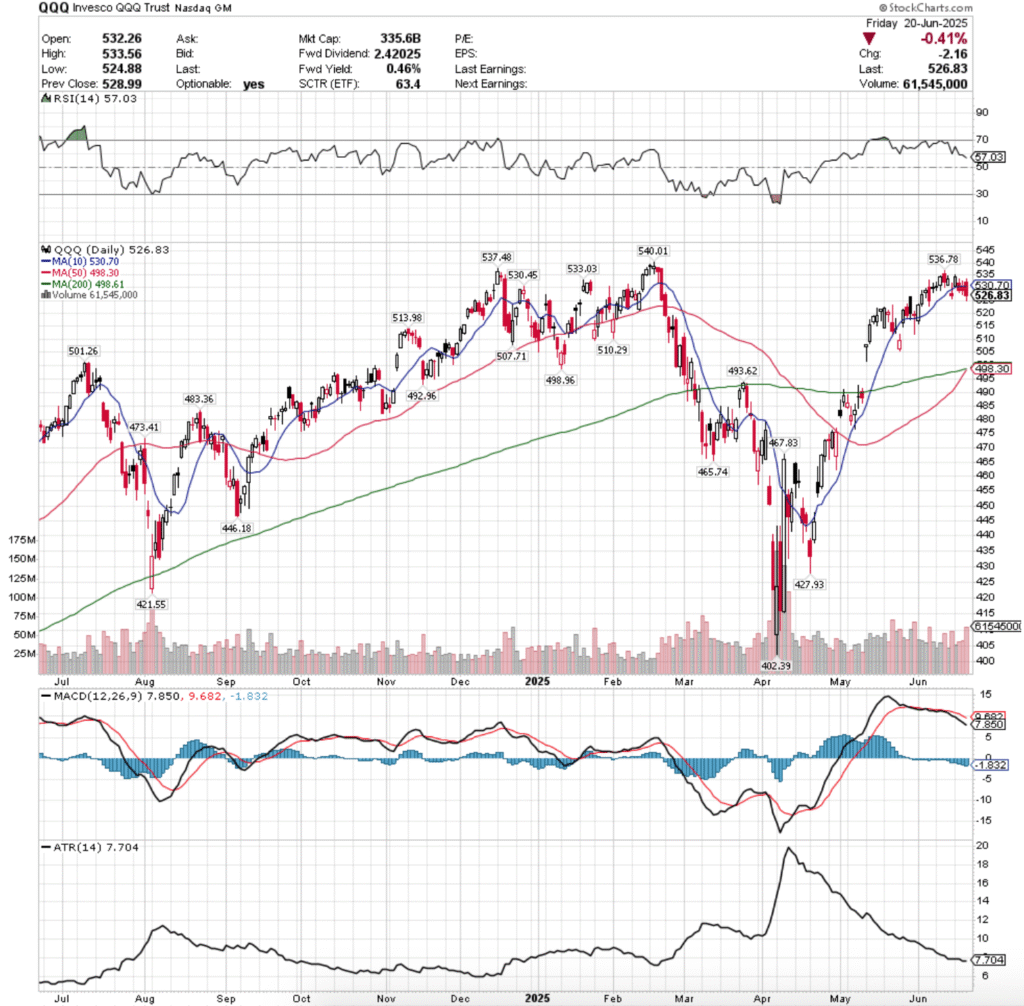

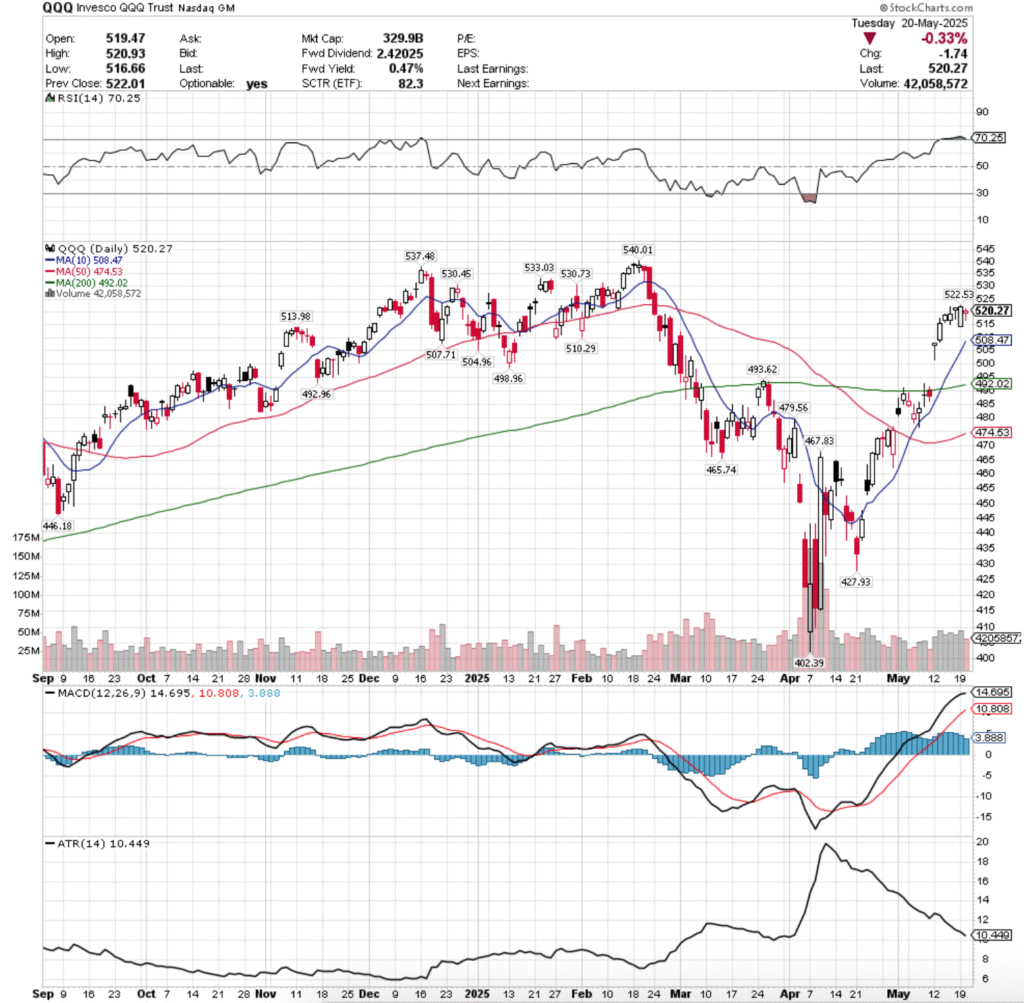

QQQ, the Invesco QQQ Trust ETF dipped -0.02% last week, and much like SPY it was mostly only that muted of a decline due to Monday’s gap up open.

QQQ ETF – Invesco QQQ Trust ETF’s Technical Performance Over The Past Year

Their RSI is trending down towards the neutral 50 level at 57.03, while their MACD is bearish & looks to signal more trouble on the near-term horizon.

Volumes were +19.62% higher than the previous year’s average (46,355,000 vs. 38,750,598), which paints a bleaker picture when you factor in that the weekest session of the week was the only advancing one, signaling that there was quite a bit of risk being taken off of the table.

QQQ’s week looked an awful lot like SPY’s with only a few small differences.

Monday’s gap up session for QQQ was their weakest volume of the week, which was quite telling about the rest of the week’s performance.

Tuesday opened lower, and while there was briefly an attempt higher the Sellers came out in droves to force a breakdown of the 10 day moving average’s support.

Wednesday this theme continued on higher declining volume, as Sellers emerged more & more throughout the week & there was more of a risk-off sentiment emerging that looks poised to carry over into the new week.

Wednesday’s candle formed a bearish harami, which was bearishly engulfed by Friday’s candle on even higher volume, which is even more bleak.

Like SPY, the upside case is relying on there not being a bearish head & shoulders pattern emerging, where the shoulders are $536.78 & $537.48/share.

Those levels need to be broken through in order for there to be a run at QQQ’s all-time high of $540.01 (the head).

Consolidation case is also like SPY’s, with the only difference being that their 50 day moving average is forming a bullish golden cross today, which may provide a brief pump, but unlikely based on the volume trends of last week.

To the downside QQQ’s first two support levels have been historically Seller zones, which will lead it down into the window formed by mid-May’s gap up & will likely force re-test of the long-term trendline.

For this week the 200 Day moving average is a good place to look from a downside perspective, as the $498-500/share is going to be a pivotal support level.

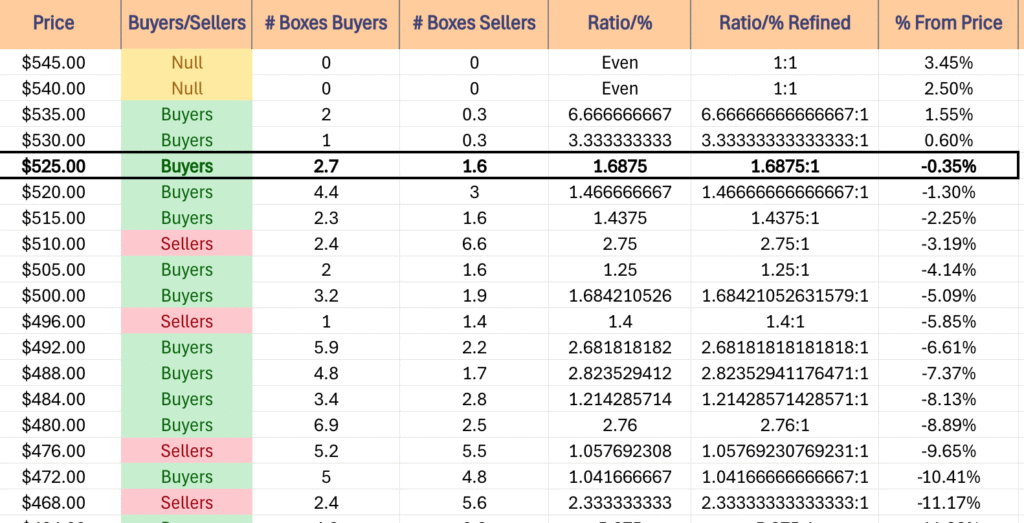

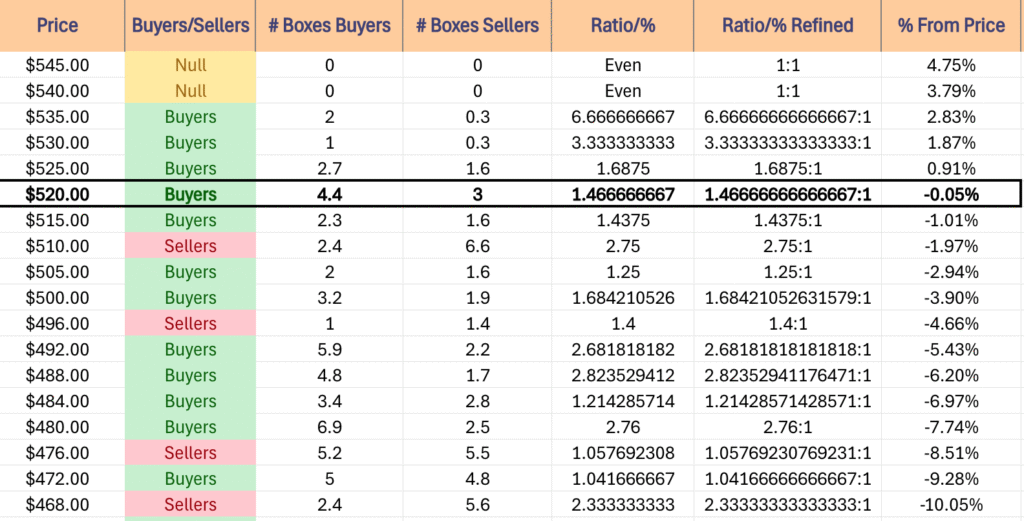

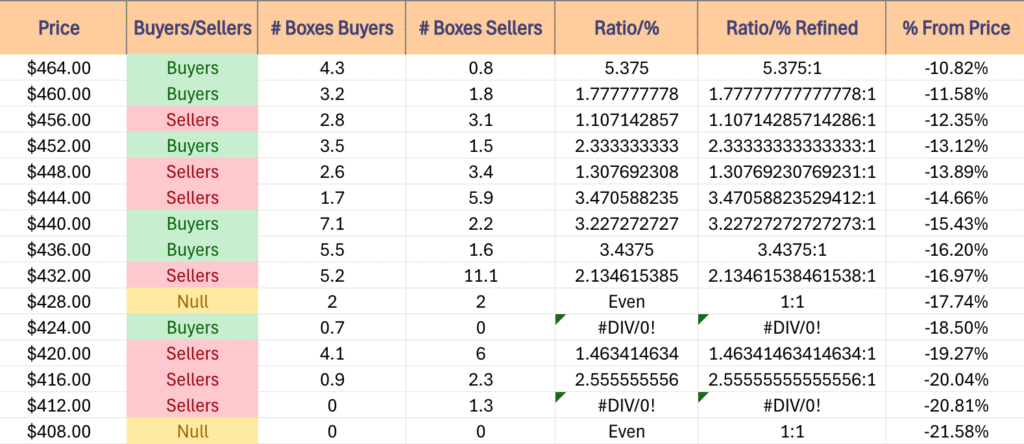

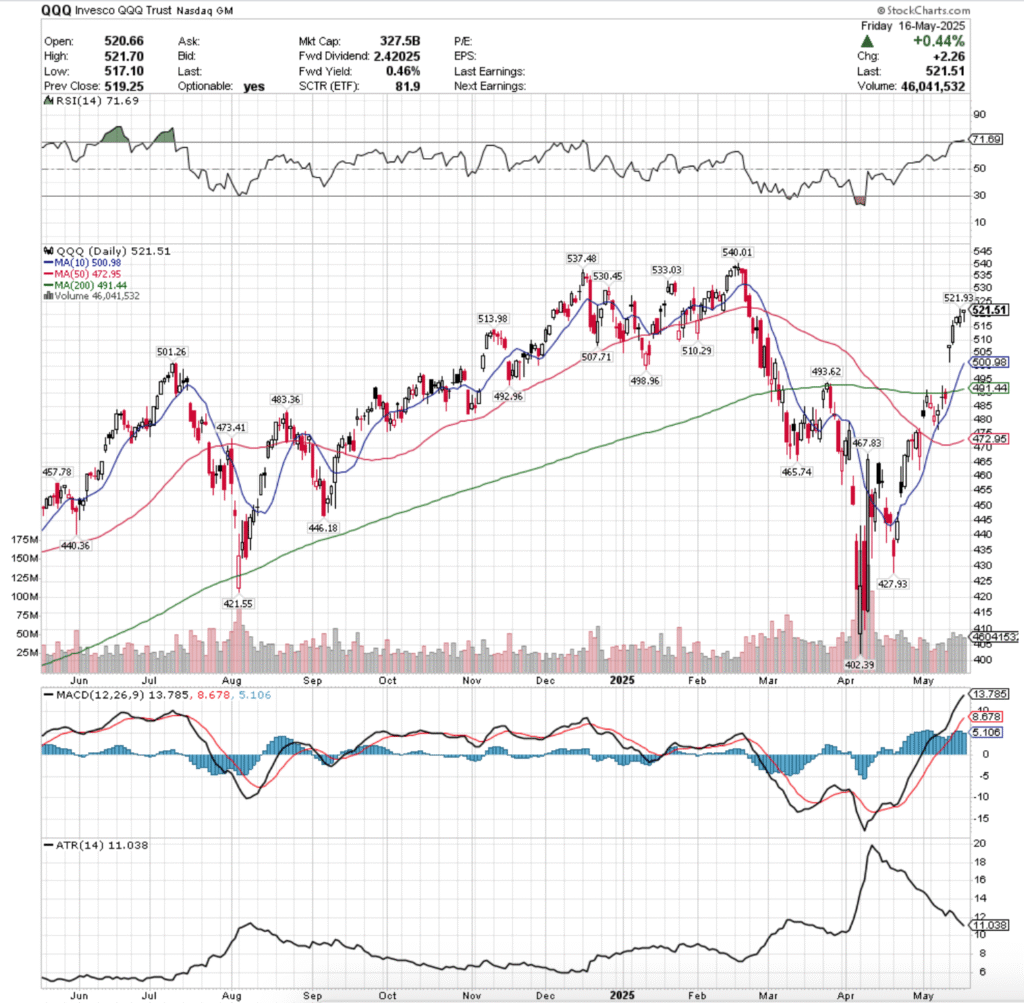

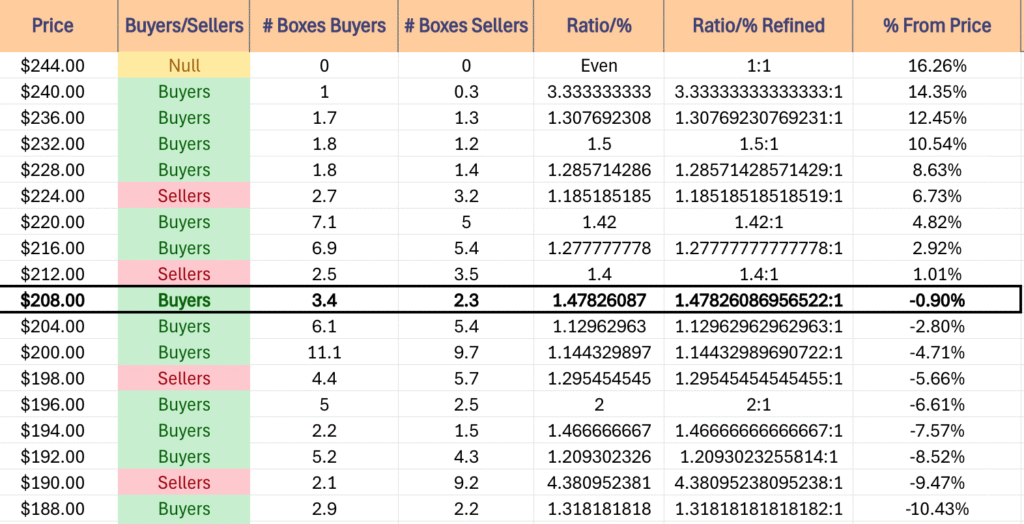

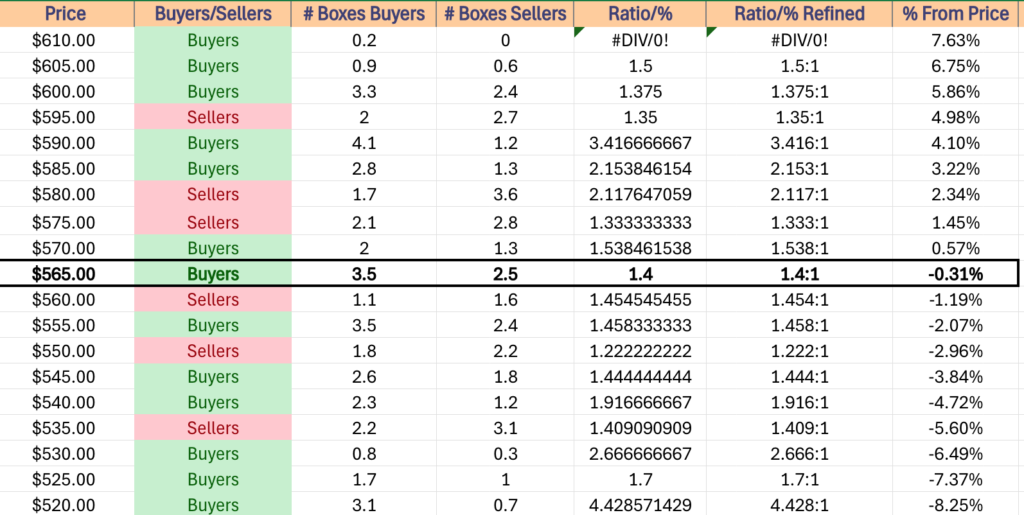

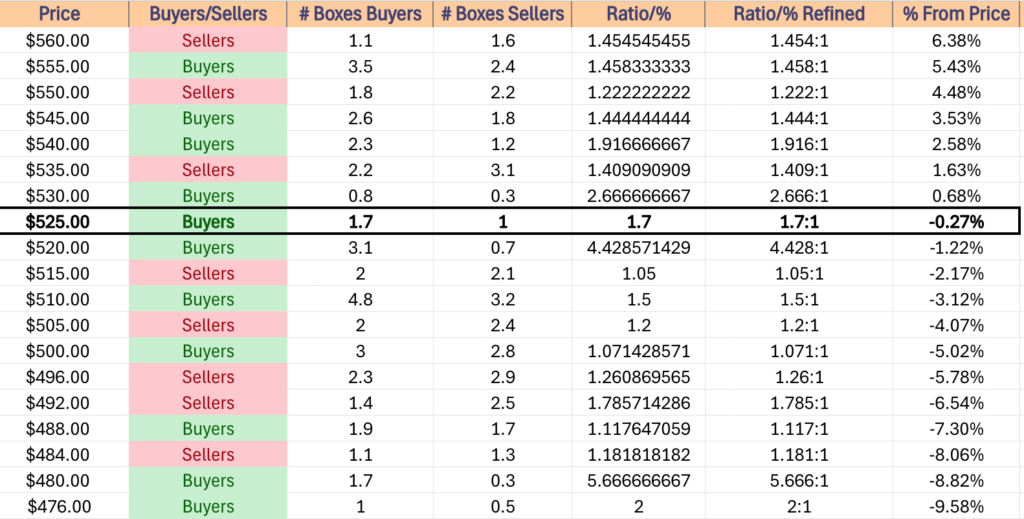

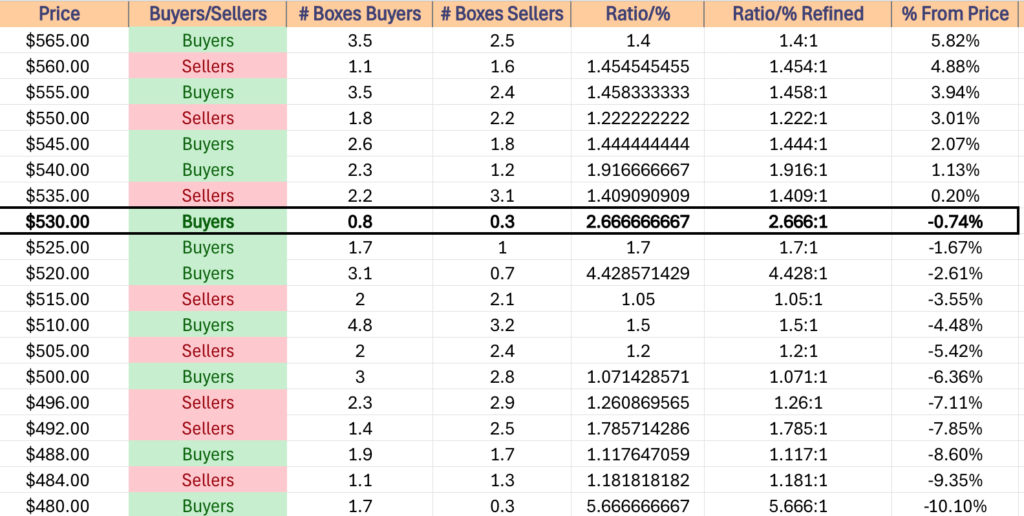

QQQ has support at the $513.98 (Volume Sentiment: Sellers, 2.75:1), $510.29 (Volume Sentiment: Sellers, 2.75:1), $507.71 (Volume Sentiment: Buyers, 1.25:1) & $501.26/share (Volume Sentiment: Buyers, 1.68:1) price levels, with resistance at the $530.45 (Volume Sentiment: Buyers, 3.33:1), $530.70 (Volume Sentiment: Buyers, 3.33:1), $533.03 (Volume Sentiment: Buyers, 3.33:1) & $536.78/share (Volume Sentiment: Buyers, 6.67:1) price levels.

QQQ ETF’s Price Level:Volume Sentiment Over The Past ~1 Year

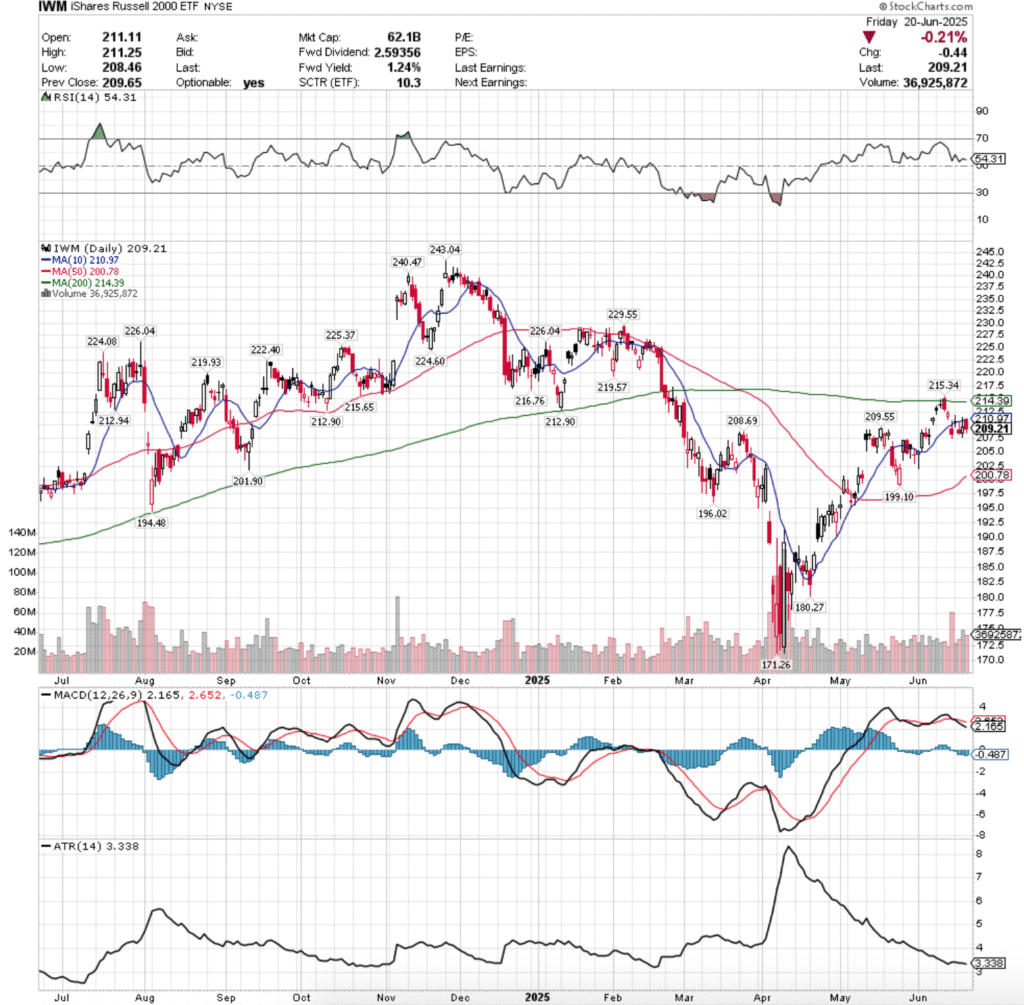

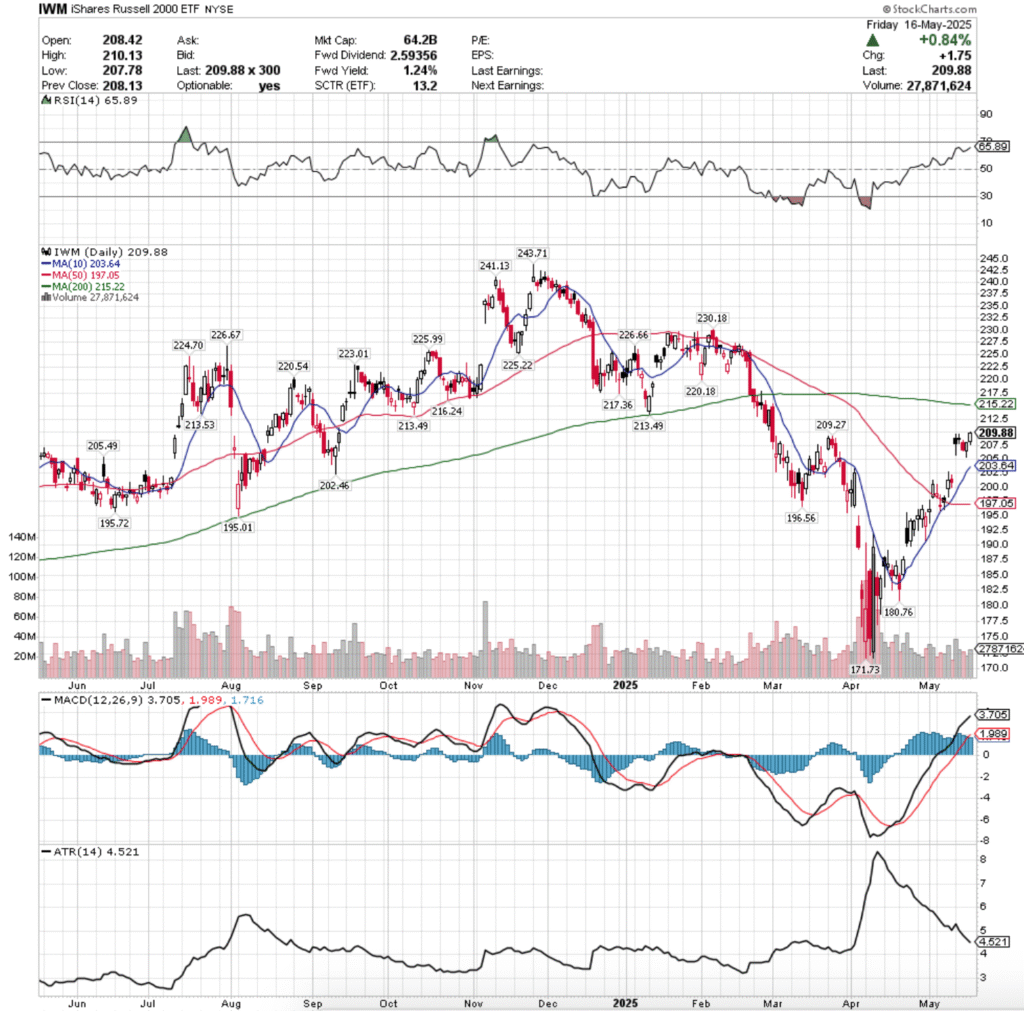

IWM, the iShares Russell 2000 ETF advanced +0.15% for the week, as there was a rotation into the small cap index after much of the past two months showed more people buying into its larger peers.

IWM ETF – iShares Russell 2000 ETF’s Technical Performance Over The Past Year

Their RSI is also declining back towards the neutral 50 level despite a stronger weekly performance than the aforementioned indexes & is currently at 54.31, while their MACD is bearish, and looks content on heading lower based on last week’s performance.

Volumes were +15.86% higher than the prior year’s average (35,410,000 vs. 30,562,351), but while Wednesday’s advancing volume led the pack in terms of strongest performing day, Friday’s risk-off move signaled that there is still quite a bit of uncertainty out there among market participants.

IWM saw a different type of week, bucking the trend of the major indexes declining for the week.

Monday opened on a gap up, and resulted ina high wave doji candle that closed in-line with the 10 day moving average, indicating that there was a strong tie to price & the short-term trendline & despite the wide trading range of the day the session produecd the lowest volume of the week.

Tuesday opened on a gap lower, attempted a run up to the resistance of the 10 day moving average, but promptly fell & resulted in a declining session.

Wednesday was the crown jewel of IWM’s week, as the session resulted in the week’s highest volume & a bullish engulfing candle, but there was a problem.

The 10 day moving average’s resistance held strong & to the downside market participants were willing to test the $207.50/share level, indicating that there was some pent up downside appetite that we had not been seeing previously.

Friday left a sour taste for IWM’s week, when the small cap index opened on a gap up in-line with the 10 day moving average, only to progress lower throughout the session & close -0.21% on the week’s second highest volume.

Risk-off into the weekend was the theme, and profits were taken to safety.

The coming week will likely hinge greatly on the other major indexes’ performances, but to the upside the $212.90/share level will be a target that needs to be overcome, as there are two resistance touch-points there.

After that the 200 day moving average comes into view, as the price has not been above the long-term trendline since February of 2025.

Consolidation looks much like SPY & QQQ’s short-term bearish head & shoulders formation forming from May’s gap up session.

To the downside the main place to keep an eye on is the 50 day moving average, as it is the gatekeeper to a Seller dominated price zone.

If it doesn’t hold up as support there is likely to be a run at the 52-week low given the unfilled gap from mid-April in the $187.50-190 range.

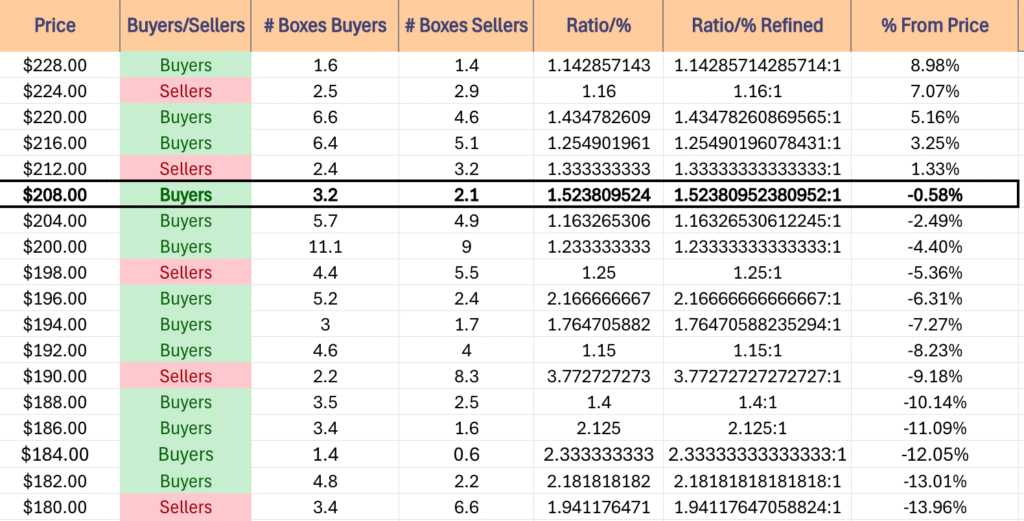

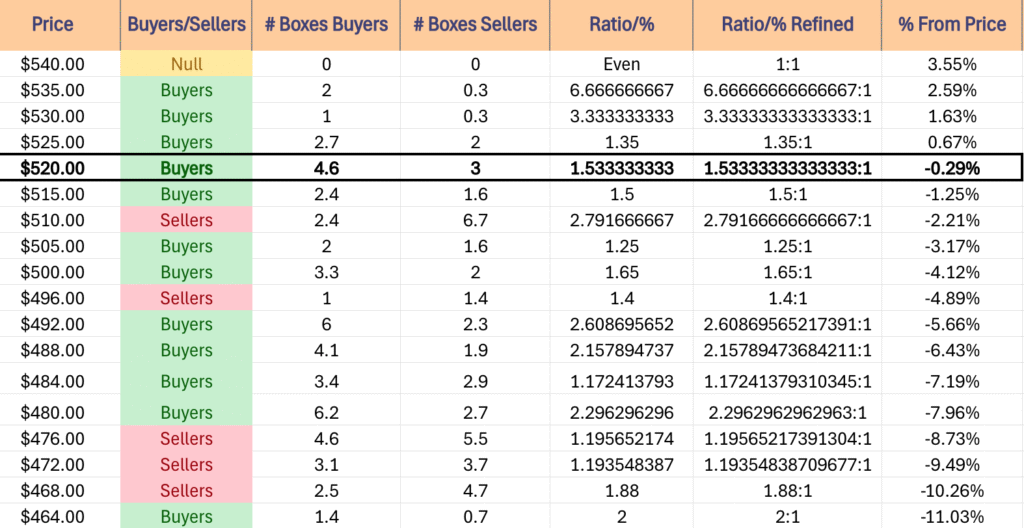

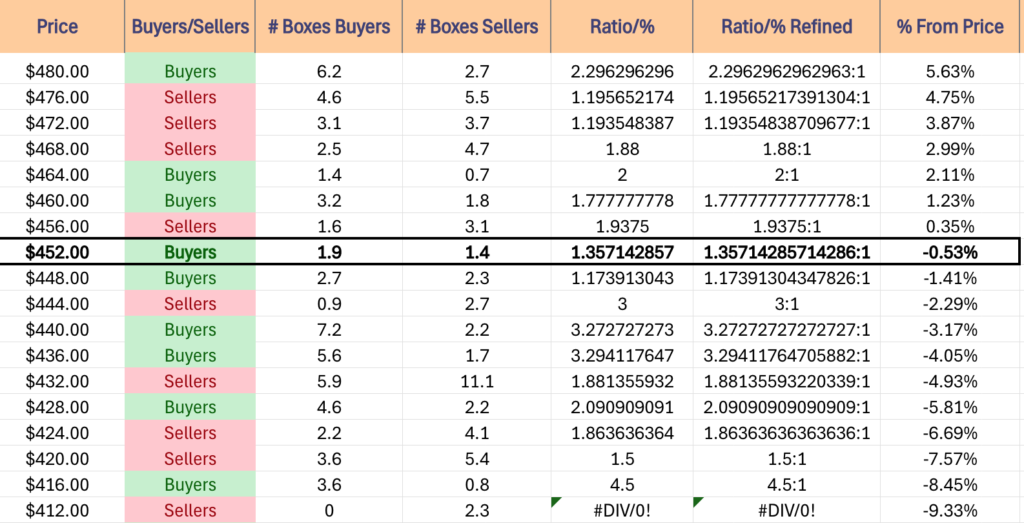

IWM has support at the $208.69 (Volume Sentiment: Buyers, 1.52:1), $201.90 (Volume Sentiment: Buyers, 1.23:1), $200.78 (50 Day Moving Average, Volume Sentiment: Buyers, 1.23:1) & $199.10/share (Volume Sentiment: Sellers, 1.25:1) price levels, with resistance at the $209.55 (Volume Sentiment: Buyers, 1.52:1), $210.97 (10 Day Moving Average, Volume Sentiment: Buyers, 1.52:1), $212.90 (2 Touch-Points, Volume Sentiment: Sellers, 1.33:1) & $212.94/share (Volume Sentiment: Sellers, 1.33:1) price levels.

IWM ETF’s Price Level:Volume Sentiment Over The Past ~3 Years

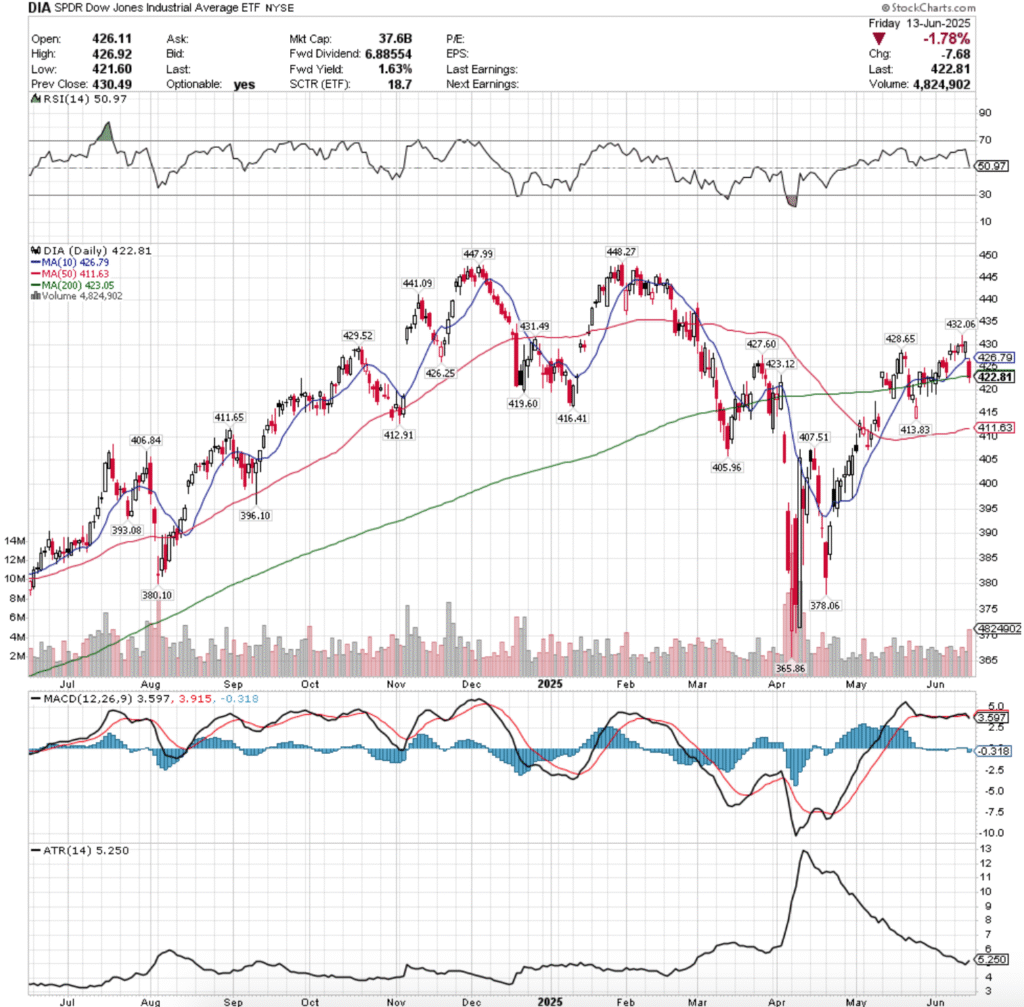

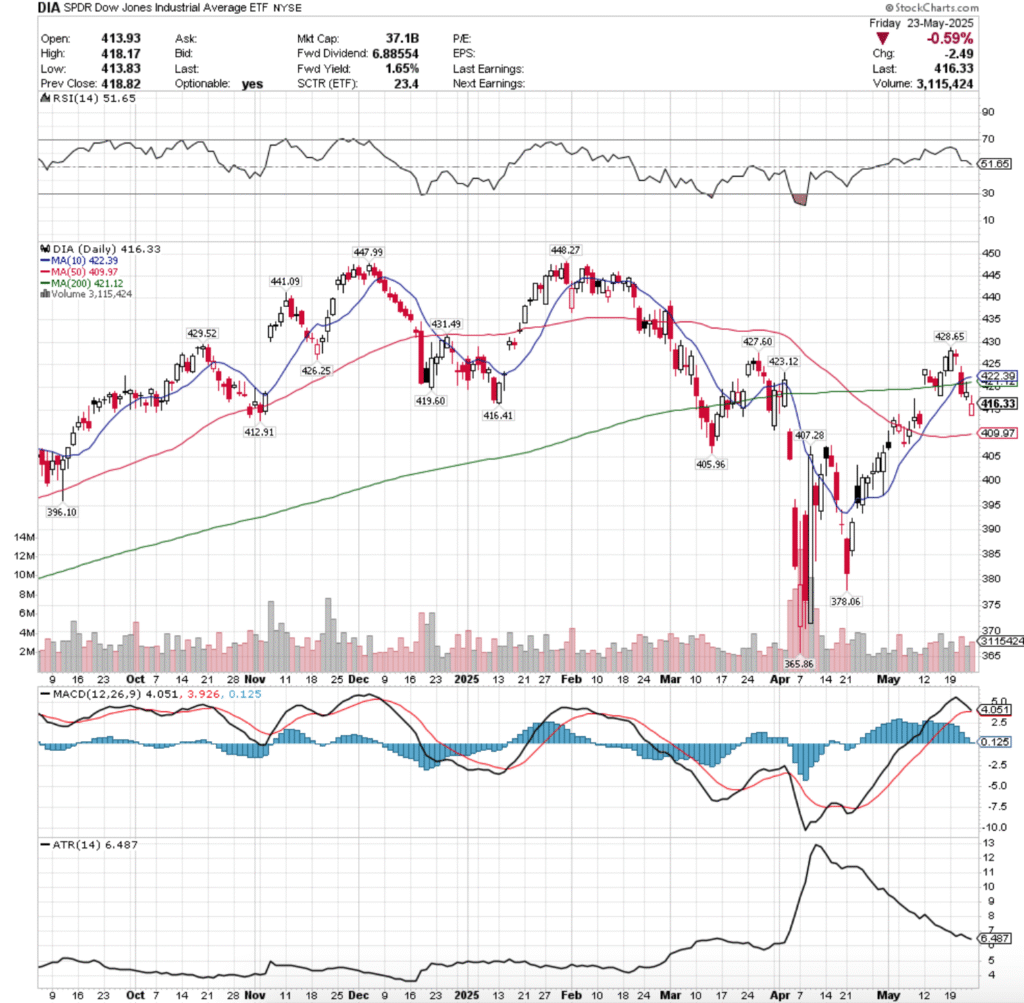

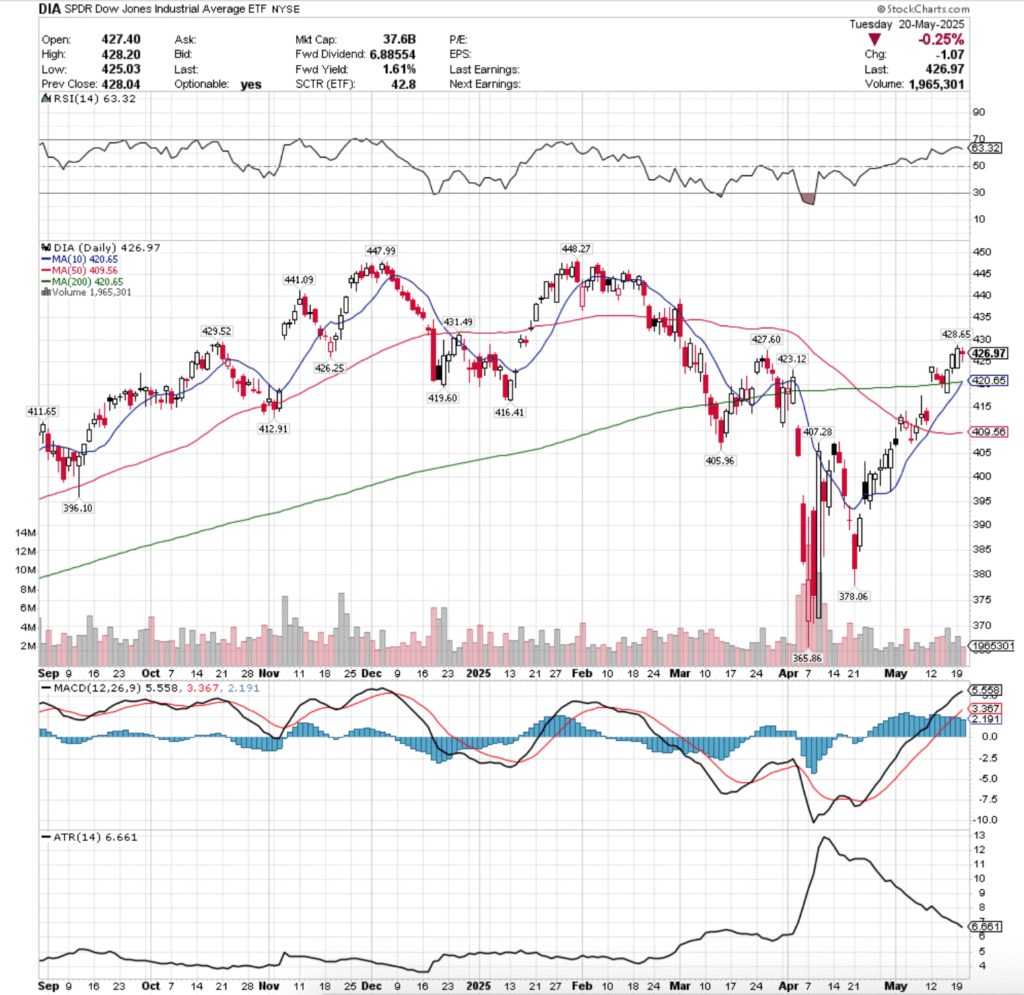

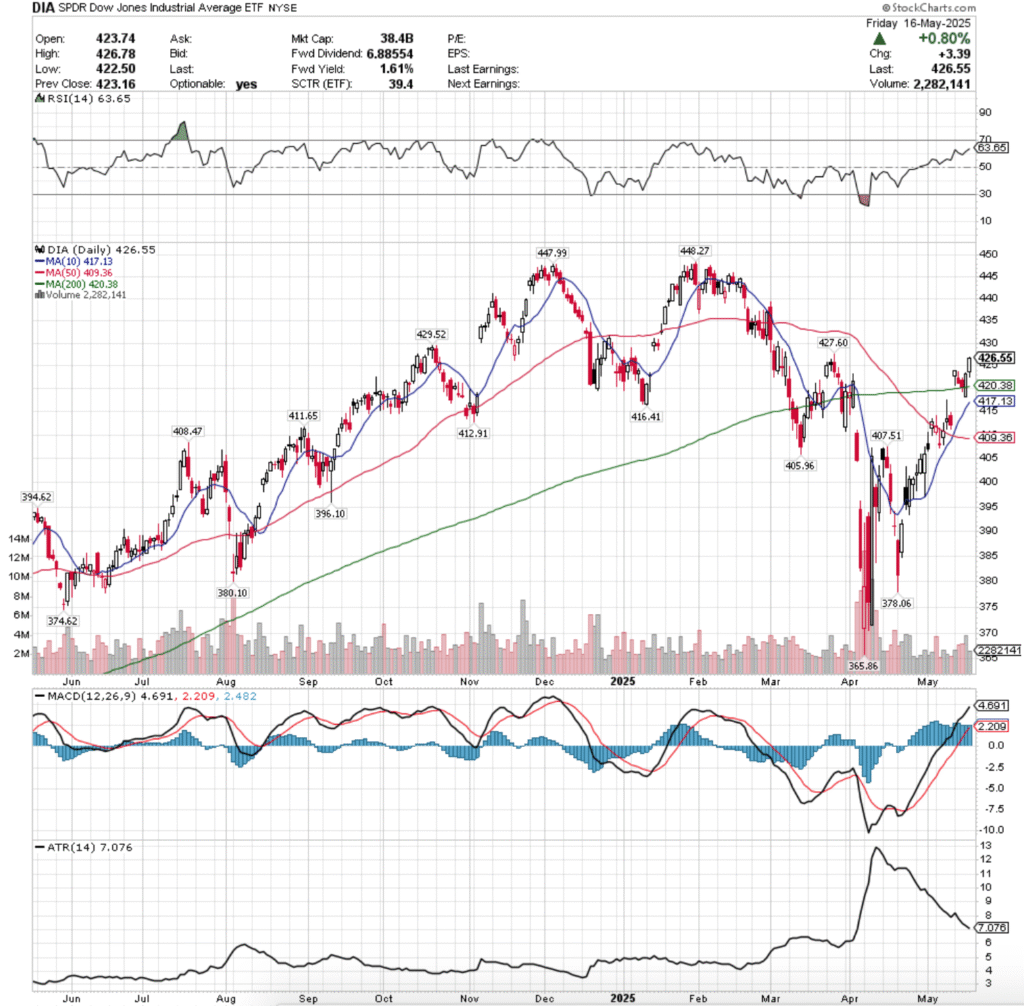

DIA ETF – SPDR Dow Jones Industrial Average ETF’s Technical Performance Over The Past Year

Their RSI is flat at 50.68, straddling the neutral 50-level, while their MACD is bearish & stretching lower indicating that there is likely more short-term pain to come.

Volumes were -4.14% below the prior year’s average levels (3,057,500 vs. 3,189,681), which paints an interesting picture given Friday had the best volume of the week on an advancing session, but given that it closed below both its opening price & the 200 DMA paints a gloomy picture.

DIA’s week kicked off on a gap up open on the second highest volume of the week, which was able to temporarily break above the 10 day moving average’s resistance, but the proved to be short-lived and profit taking forced the session to close near the previous Friday’s open.

Tuesday opened on a gap down, but showed mixed signals as the lowest volume session of the week tested the resistance of the 10 day moving average but was rejected, before the 200 day moving average was tested & the long-term trendline showed signs of fatigue.

Wednesday was more of the same, but the real body of the session’s candle stayed on the lower end of the daily range, on slightly higher volume, indicating that there was a bit of hesitancy & risk aversion in the air.

Friday opened on a gap higher, but the week’s highest volume session resulted in a lot of profit-taking that drove prices to break down though the 200 day moving average temporarily, before closing lower than the day’s open just below the 200 day moving average.

Looking at their 10 day moving average vs. the 200 DMA we appear to have more pain on the horizon for DIA, but the upside case revolves heavily around breaking above the 200 & 10 day moving averages first, which appears unlikely without a massive shift in advancing volume.

Should we see that, the $430.83 is the high water target in the near-term.

The consolidation case also has the making of a bearish head & shoulders pattern emerging, with declines likely to come in the wake of the 10 DMA death crossing through the 200 DMA, but until then DIA will likely oscillate around & in between the two trendlines.

In the event of decline DIA has a bit of a headwind on the horizon, as once their first support levels is broken through the next 3+ are all in Seller dominated price zones, which will potentially lead to a re-test of the $410.48 or $406.35/share level, depending on where it manages to find footing.

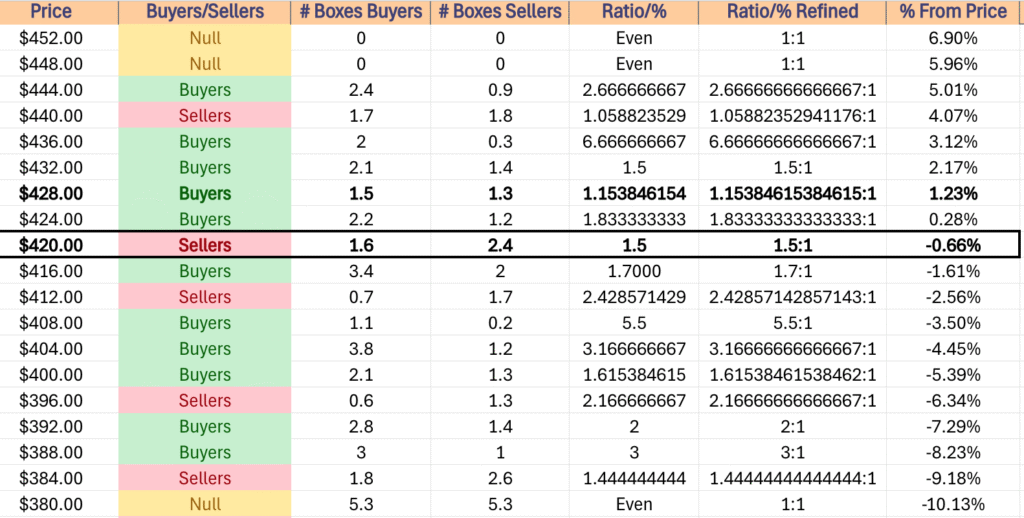

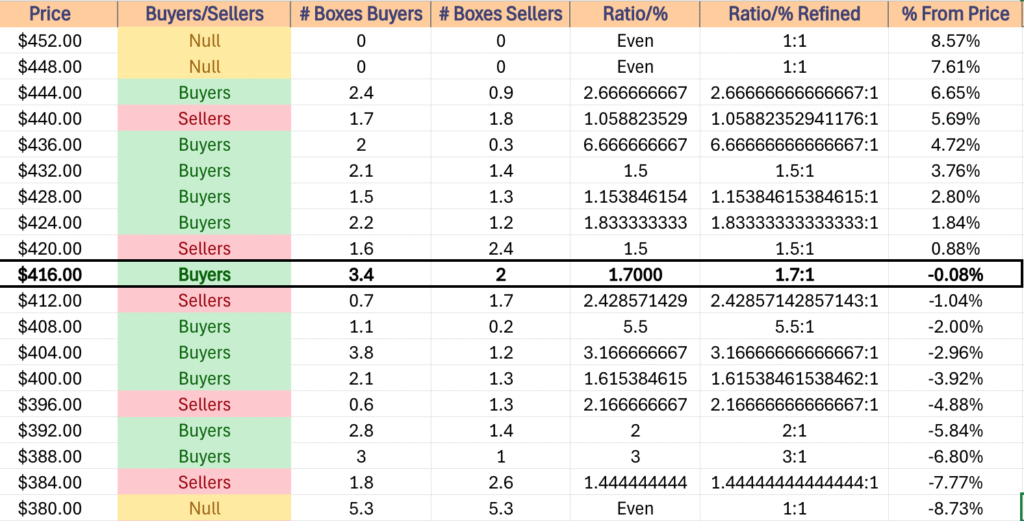

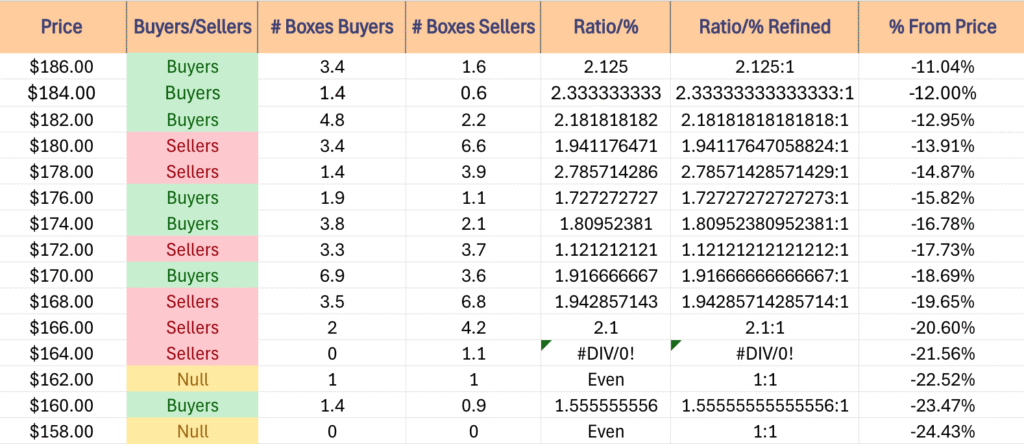

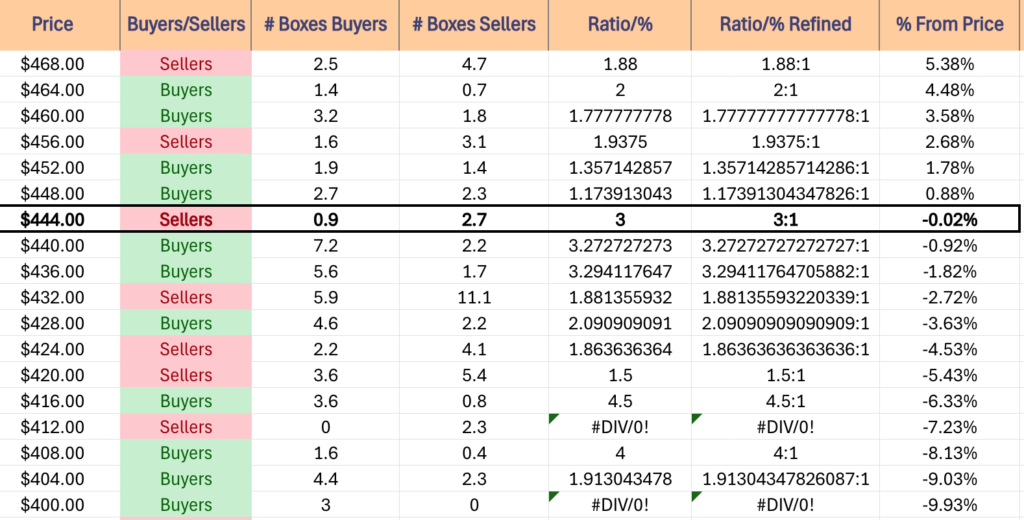

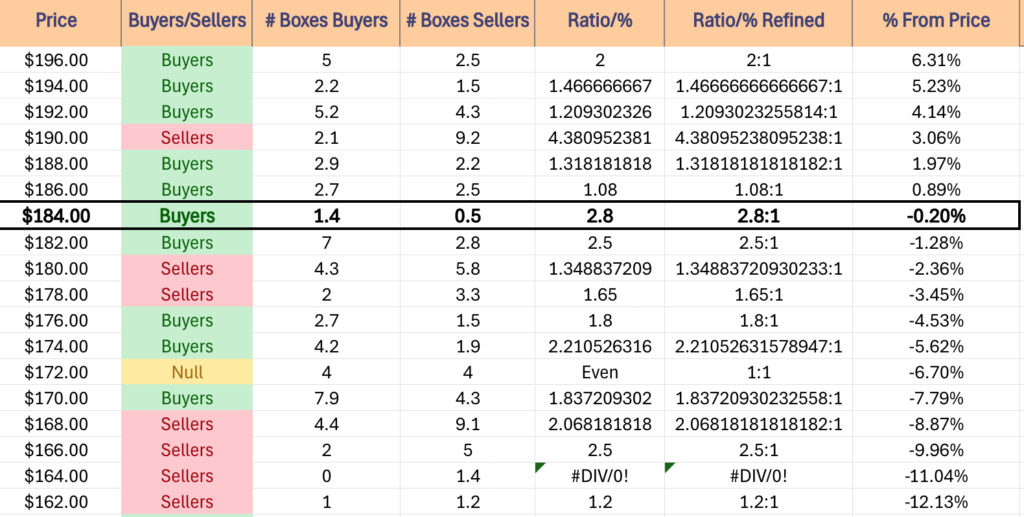

DIA has support at the $418.41 (Volume Sentiment: Buyers, 1.7:1), $415.23 (Volume Sentiment: Sellers, 2.43:1), $413.51 (50 Day Moving Average, Volume Sentiment: Sellers, 2.43:1) & $412.66/share (Volume Sentiment: Sellers, 2.43:1) price levels, with resistance at the $421.92 (Volume Sentiment: Sellers, 1.5:1), $422.16 (200 Day Moving Average, Volume Sentiment: Sellers, 1.5:1), $425.04 (Volume Sentiment: Buyers, 1.83:1) & $425.23/share (10 Day Moving Average, Volume Sentiment: Buyers, 1.83:1) price levels.

DIA ETF’s Price Level:Volume Sentiment Over The Past ~4 Years

The Week Ahead

Monday the week kicks off with S&P Flash U.S. Services PMI & S&P Flash U.S. Manufacturing PMI data at 9:45 am, followed by Existing Home Sales data at 10 am.

Commercial Metals & Fact set report earnings before Monday’s opening bell, followed by KB Home after the session’s close.

S&P Case-Shiller Home Price Index (20 Cities) data comes out Tuesday morning at 9 am, before Fed President Hammack speaks at 9:15 am, Consumer Confidence data is released at 10 am, and Fed Chair Powell testifies to the House Financial Service Committee at 10 am as well.

Tuesday morning begins with earnings calls from Carnival & TD Synnex, before FedEx, AeroVironment, BlackBerry & Worthington Enterprises report after the closing bell.

Wednesday morning begins with New Home Sales data at 10 am.

General Mills, Paychex & Winnebago report earnings before Wednesday’s opening bell, followed by Micron Technology, H.B. Fuller, Jefferies, MillerKnoll, Steel case & Worthington Steel after the session closes.

Advanced U.S. Trade Balance In Goods, Advanced Retail Inventories, Advanced Wholesale Inventories, Initial Jobless Claims, Durable-Goods Orders, Core Durable-Goods Orders & GDP (Second Revision) data all come out Thursday at 8:30 am, before Fed President Hammack speaks at 9 am & Pending Home Sales data at 10 am.

Acuity, Lindsay Corp., McCormick & Walgreens Boots Alliance report earnings before Thursday morning’s opening bell, before Nike & Concentrix report after the session’s closing bell.

Friday the week winds down with Personal Income, Personal Spending, PCE Index, PCE Year-over-Year, Core PCE Index & Core PCE Index (Year-over-Year) at 8:30 am before Consumer Sentiment (Final) data comes out at 10 am.

Apogee Enterprises reports earnings on Friday morning.

See you back here next week!

*** I DO NOT OWN SHARES OR OPTIONS CONTRACT POSITIONS IN SPY, QQQ, IWM OR DIA AT THE TIME OF PUBLISHING THIS ARTICLE ***

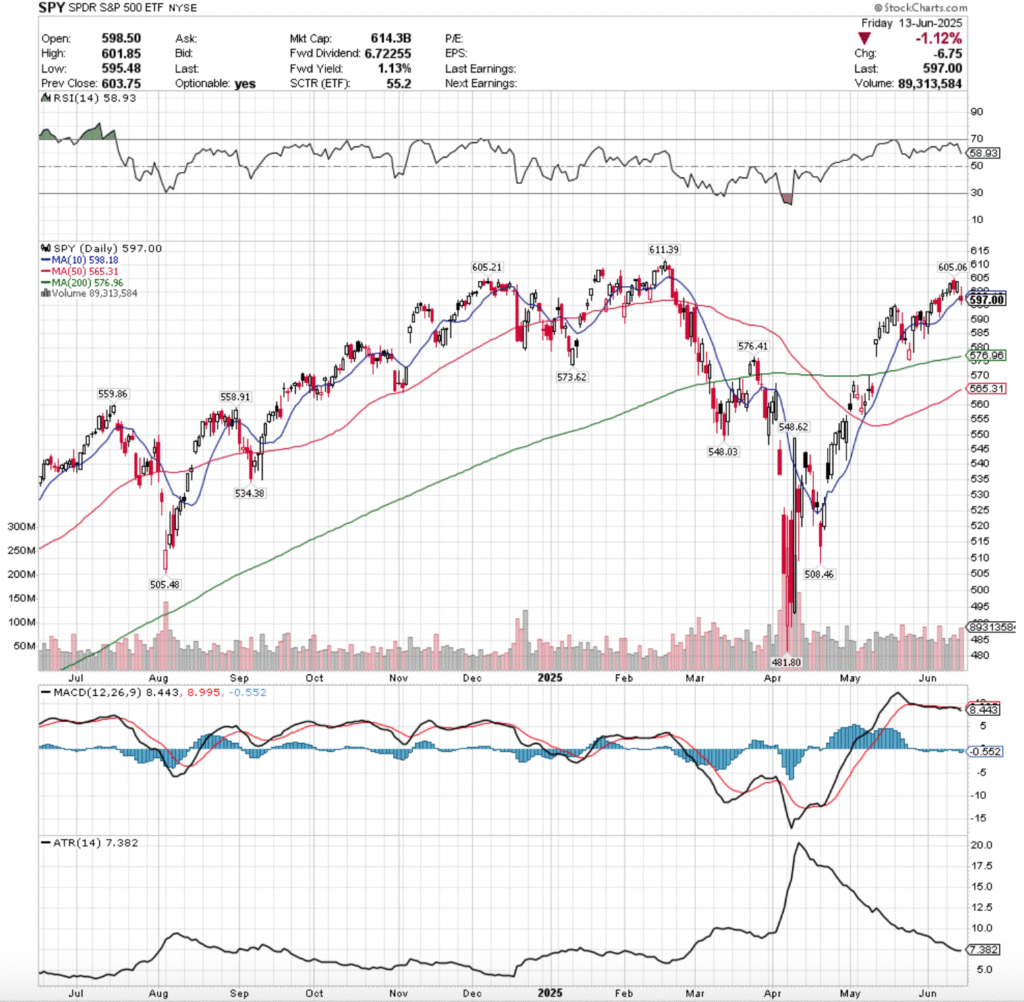

SPY, the SPDR S&P 500 ETF lost -0.36% this week, while the VIX closed at 20.82, indicating an implied one day move of +/-1.31 & a one month implied move of +/-6.02%.

SPY ETF – SPDR S&P 500 ETF’s Technical Performance Over The Past Year

Their RSI is trending down towards the neutral 50 mark & is currently at 58.93 & their MACD is bearish, but still relatively flat; however their histogram is signaling that bearishness is likely to continue & expand next week.

Volumes were +19.92% higher than the prior year’s average (69,314,000 vs. 57,801,235), with Friday’s bearish session seeing the highest level of the week, as market participants were eager to take risk off of the table before the weekend in the wake of Israel & Iran’s conflict escalating.

Last week kicked off on a note of uncertainty for SPY, as the session opened in line with Friday’s close & produced the lowest volume of the week to close as a doji candle, indicating that there was not much confidence & market participants were more in a “wait & see” type of mood.

Tuesday opened higher, retraced much of Monday’s candle to the downside, before pushing higher to close at $603.08/share on slightly better volume.

Wednesday confirmed the feelings of unease, as a gap up open managed to break above the $605/share mark temporarily, before plunging down & exposing the vulnerability in broader markets on the week’s second highest volume as market participants took chips off of the table following the gains of Tuesday.

Thursday opened lower & made a run at Wednesday’s opening price but failed to reach it as there was not enough positive sentiment in the market, and that inability to hit Wedneday’s open or high signaled that there is clearly an impediment at the $605/share level.

Friday was the epitome of a ris-off day, as a gap down open led to a brief stint above $600/share again, but profits were quickly taken from the table & SPY was forced down to $595.48 before closing at $597/share ont he highest volume of the week.

Looking to the coming week there are a few things to take into consideration.

Firstly, the $605/share level looks to be forming the shoulders of a potential bearish head & shoulders pattern on the one year chart with the $611.39/share level, which will be an area of focus in the coming week.

There is also another head & shoulders pattern brewing on a more short-term level bearishly that began with the gap up on May 12, 2025 which will be something to watch, as it may well become an island top when the gap created that day gets filled.

The bullish case for SPY is now incredibly simple, the $605-605.99/share zone needs to be broken through & it needs solid advancing volume if it is to be sustainable.

If that can’t happen, we don’t see a run at the all-time high of $611.35/share, much less it broken through.

There is likelihood of a squeeze higher situation early in the week where a mix of short-covering & “last hurrah” profit seekers pump prices up before Wednesday’s FOMC decision, but if $605 holds up as a resistance point/doesn’t get retested it’s a signal of bearishness.

The consolidation case remains the same as it has for the past month in our notes, oscillations around the 10 day moving average, but keep an eye on the 50 DMA approaching the 200 DMA bullishly, as a golden cross may boost confidence briefly & lead to some advances.

The consolidation case looks to be the best case scenario at the moment, as there is limited data & earnings coming out this week, minus the FOMC decision & earnings/reports on the state of homebuilders & the housing market, as well as some US absed manufacturing data on a shortened holiday week (Thursday the market is closed).

To the downside there begins to be some pockets of concern given how SPY has recently performed.

One of the most important things to watch heading into this week is that when things do cool off, how far support levels are away from SPY’s closing price.

There is a very easy to visualize ~3% decline on the horizon when you look at SPY’s support levels heading into the new week, where the 200 day moving average comes into play.

All eyes should be on there if we see any declines this week, as the long-term trend line is likely to be retested.

The long-term trend line is ~-3.36% lower than Friday’s close & will likely be retested in the event of any declines given how few support levels SPY has at this point.

That’s where to fixate attention to at the moment, particularly when you reference the table below for their historic price level sentiment.

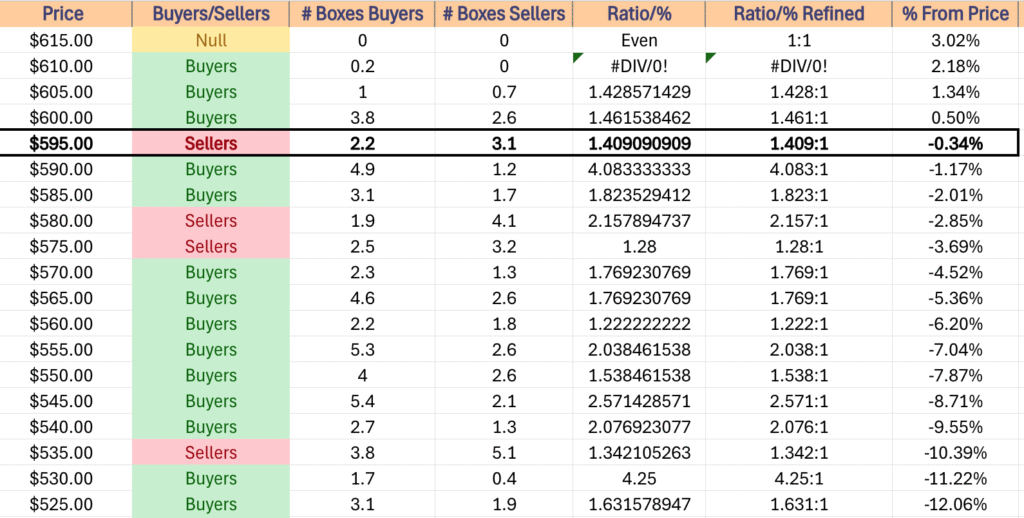

SPY has support at the $576.96 (200 Day Moving Average, Volume Sentiment: Sellers, 1.28:1), $576.41 (Volume Sentiment: Sellers, 1.28:1), $573.62 (Volume Sentiment: Buyers, 1.77:1) & $565.31/share (Volume Sentiment: Buyers, 1.77:1) price levels, with resistance at the $598.18 (10 Day Moving Average, Volume Sentiment: Sellers, 1.41:1), $605.06 (Volume Sentiment: Buyers, 1.43:1), $605.21 (Volume Sentiment: Buyers, 1.43:1) & $611.39/share (All-Time High, Volume Sentiment: Buyers, 0.2:0*) price levels.

SPY ETF’s Price Level:Volume Sentiment Over The Past ~3 Years

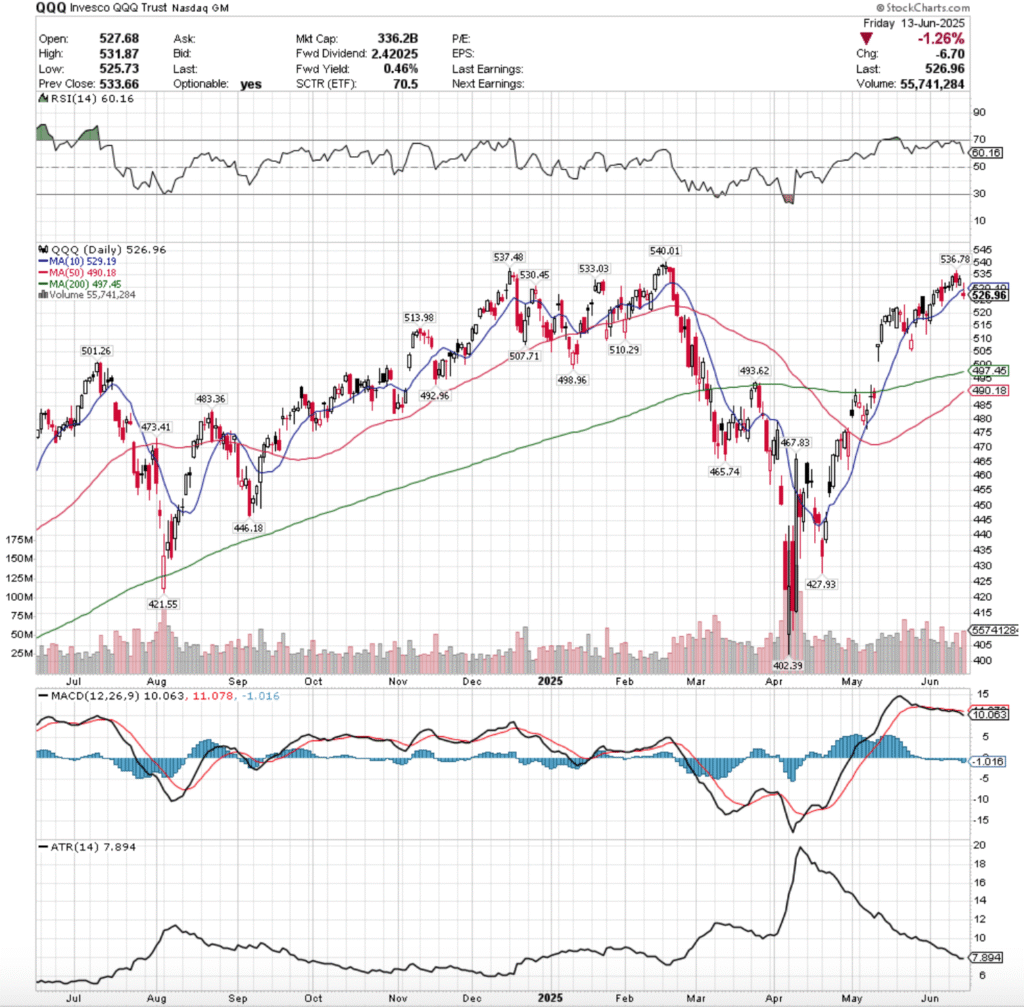

QQQ, the Invesco QQQ Trust ETF dropped -0.56% last week, as the tech heavy index was saved in part by Oracle’s earnings call.

QQQ ETF – Invesco QQQ Trust ETF’s Technical Performance Over The Past Year

Their RSI is trending down back towards the neutral 50-mark & is currently at 60.16, while their MACD is still bearish, with their histogram implying that there is more declines & sour sentiment on the horizon.

Volumes were +13.36% higher than the previous year’s average (43,592,000 vs. 38,452,988), led primarily by Wednesday & Friday’s declining sessions, which were the two highest volume days of the week.

Monday started off similar to SPY, another low volume doji session as market participants digested the week prior’s data & looked ahead to plan the approach to the following week that is short & features an FOMC decision.

Tuesday opened on a gap higher, tested back below the $520/share mark, but was able to grind higher on slightly better volume than the previous day.

Wednesday opened on a gap up to above $535, but was unable to gain stable footing & wound up declining throughout the session, reverting back towards the 10 day moving average & indicating that the sh0rt term trend had not been broken out from.

Thursday opened on a gap down, but the weak volume session managed to squeeze QQQ higher briefly, but the lack of participation was noted.

It was felt on Friday when QQQ opened on a gap down, tried to retrace higher & break back to where it had spent the week, but was unable to as profits were taken & prices were forced lower, causing a -1.26% decline & forcing the close & open to both take place below the resistance of the 10 day moving average.

Looking ahead to this week, that negative sentiment is in the air & any bullishness is making a run at all-time highs, so unless we see a real shift in rising advancing volume or a surprise bit of FOMC news there’s not much to watch beyond the $540.01/share mark.

There is a growing concern about the potential bearish head & shoulders pattern from November where the ATH is the head & $537.48 & $536.78/share are the left & right shoulder respectively, which will be something to watch.

The consolidation case here is the same as usual, oscillations around the 10 day moving average, waiting for an upside or downside catalyst to strike, while also awaiting a potential small short-term pump from the 50 & 200 DMA’s golden cross that is impending.

The downside case has the $507.71/share price level in target, as the three higher support levels are all Seller dominated & this resides in the window created in early May that needs to be filled.

Should this get retested, the 200 day moving average’s support will come into question & likely see a re-test, as the long-term trendline is beginning to look less stable.

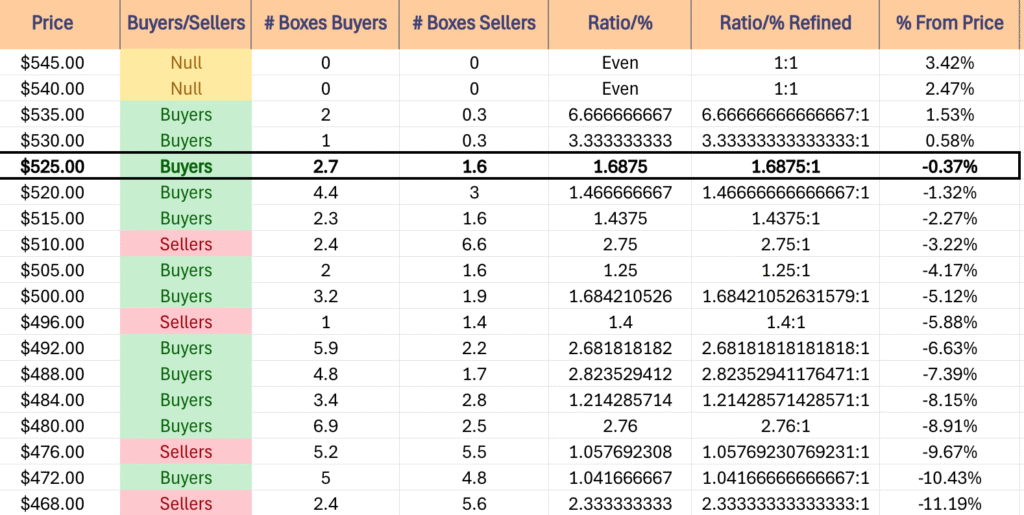

QQQ has support at the $513.98 (Volume Sentiment: Sellers, 2.75:1), $510.29 (Volume Sentiment: Sellers, 2.75:1), $510.29 (Volume Sentiment: Sellers, 2.75:1) & $507.71/share (Volume Sentiment: Buyers, 1.25:1) price levels, with resistance at the $529.19 (10 Day Moving Average, Volume Sentiment: Buyers, 1.69:1), $530.45 (Volume Sentiment: Buyers, 3.33:1), $533.03 (Volume Sentiment: Buyers, 3.33:1) & $536.78/share (Volume Sentiment: Buyers, 6.67:1) price levels.

QQQ ETF’s Price Level:Volume Sentiment Over The Past ~1 Year

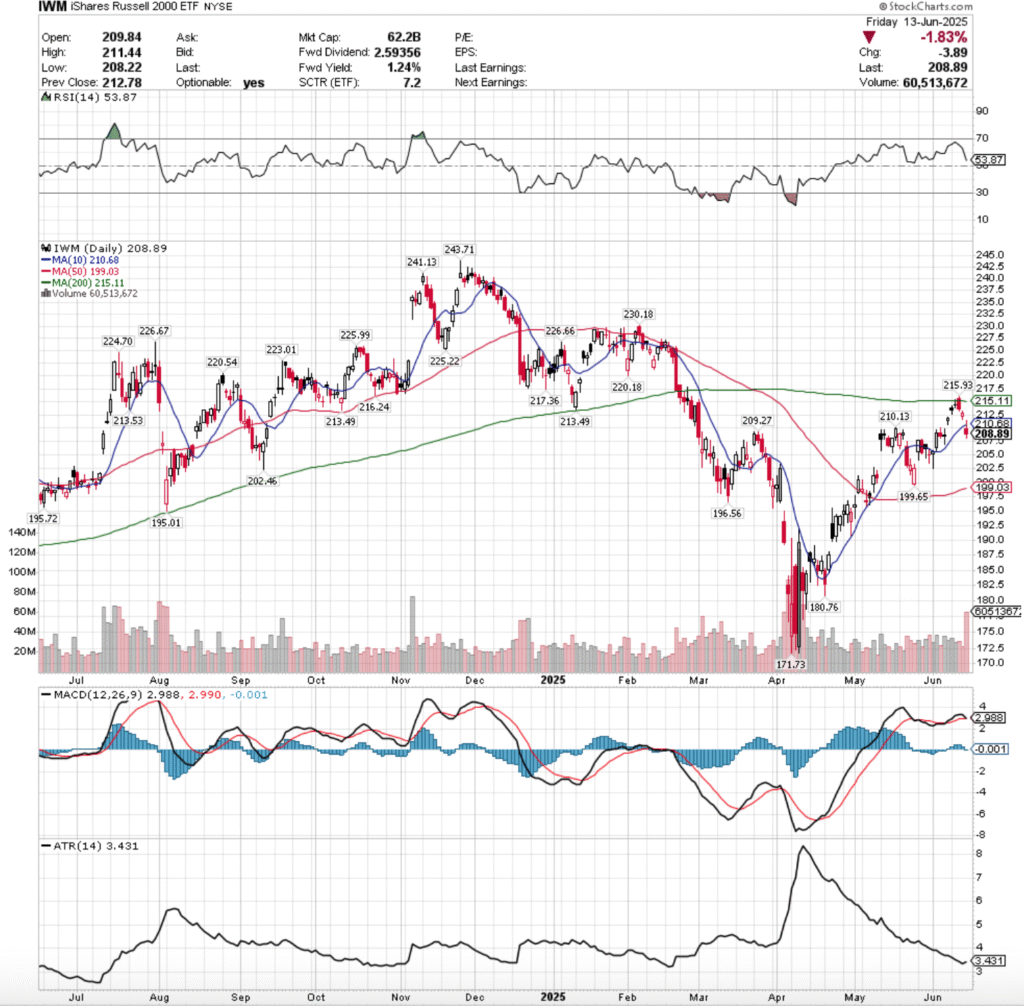

IWM, the iShares Russell 2000 ETF declined -1.42% last week, as the small cap index fell back out of favor among market participants.

IWM ETF – iShares Russell 2000 ETF’s Technical Performance Over The Past Year

Their RSI is trending back towards the neutral 50-level, currently at 53.87, while their MACD is set to cross over bearishly on Monday’s open.

Volumes were +19.04% higher than the previous year’s average (36,244,000 vs. 30,446,096), which is cause for concern given that the declining volume on Friday eclipsed the rest of the week, hitting levels not seen since early April 2025.

Monday opened the week up on a gap up on the week’s second highest volume, but there was a major warning sign flashed as the volume indicates short-term profit taking & the day closed as a hanging man candle that closed lower than it opened.

Tuesday again gapped higher on the open, this time on less volume indicating skepticism in the strength behind the recent advances, and the gravestone doji candle signaled that there was about to be a risk-off move.

Wednesday confirmed this, as the open was on a gap up to above the resistance of the 200 day moving average, but quickly chips were taken off of the table & the long-term trendline prevailed.

Thursday opened on a gap lower & experienced a short-term pump intraday that forced the close to be higher than the open, but the low volume & nature of the previous few sessions did not make for a convincing bullish case.

Friday this continued, where a gap down open to below the support of the 10 day moving average occurred, IWM made a run to break above the short-term moving average & failed as intraday profits were collected, and the result was a -1.83% day on high declining volume, indicating that there’s more pain to come.

Heading into a new week, the bullish case requires a successful retest of the $210.13/share resistance level, which would then with enough advancing volume behind it lead to a retest of the $214.49/share level, which has two resistance levels, which happens to reside in a Seller dominated zone.

Should that test succeed, we see a long-term trendline retest on the horizon, but that’s getting ahead of ourselves, particiularly if we get there via gap ups

The consolidation case is an oscillation around the 10 DMA, while we await a catalyst to move SPY, QQQ or DIA & carry IWM with it.

To the downside, the primary focal point now is the 50 day moving avearge’s support, which is moving upwards which may help IWM prevent declines, but is certainly the gatekeeper to the downside.

If the 50 DMA breaks down, the 2025 year low price is the last test that matters.

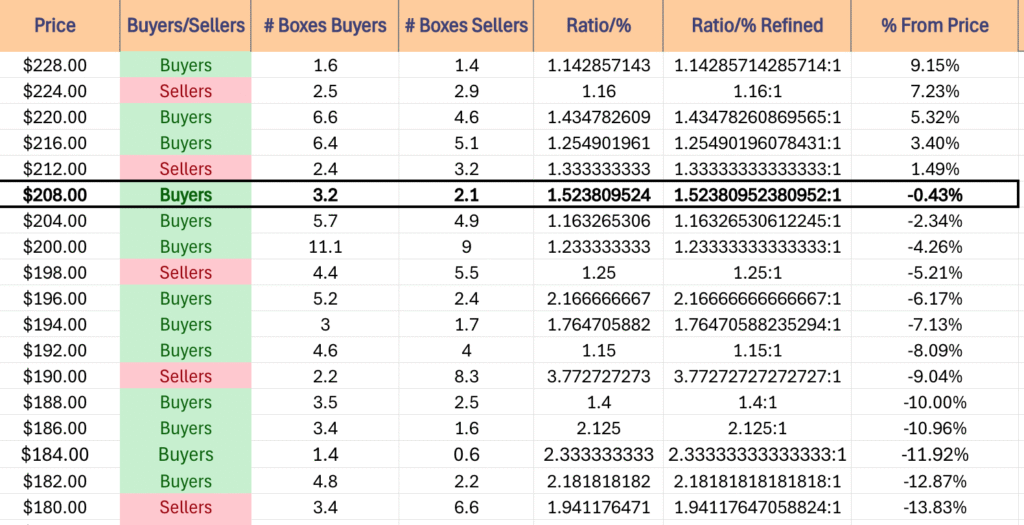

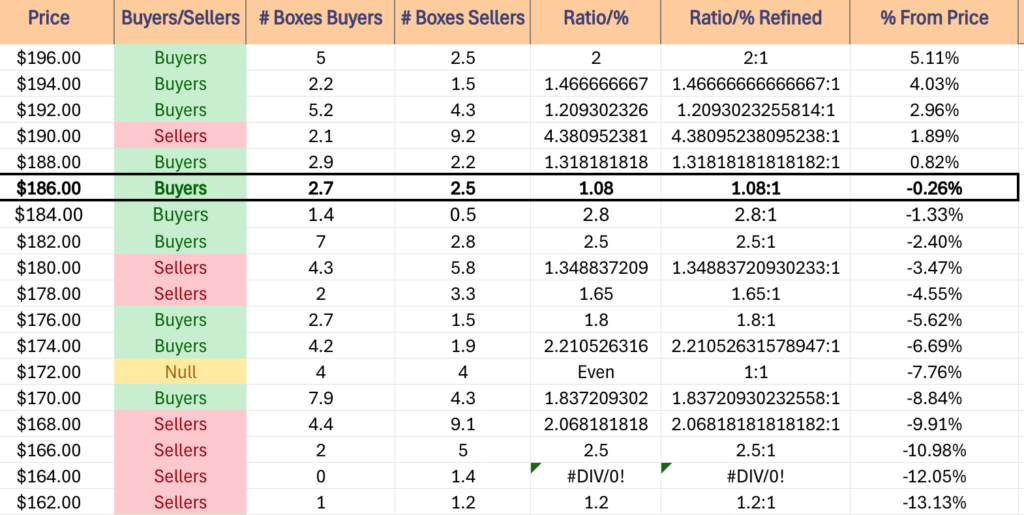

IWM has support at the $202.46 (Volume Sentiment: Buyers, 1.23:1), $199.65 (Volume Sentiment: Sellers, 1.25:1), $199.03 (50 Day Moving Average, Volume Sentiment: Sellers, 1.25:1) & $196.56/share (Volume Sentiment: Buyers, 2.17:1) price levels, with resistance at the $209.27 (Volume Sentiment: Buyers, 1.53:1), $210.13 (Volume Sentiment: Buyers, 1.53:1), $210.68 (10 Day Moving Average, Volume Sentiment: Buyers, 1.53:1) & $214.49/share (2 Touch-Points, Volume Sentiment: Sellers, 1.33:1) price levels.

IWM ETF’s Price Level:Volume Sentiment Over The Past ~2-3 Years

DIA ETF – SPDR Dow Jones Industrial Average ETF’s Technical Performance Over The Past Year

Their RSI is trending downwards & near neutral at 50.97, while their MACD crossed over the signal line bearishly on Friday.

Volumes were -4.79% lower than the previous year’s average (3,028,000 vs. 3,180,398), which like IWM is cause for concern based on Friday’s declining session’s volume eclipsing most of 2025’s volumes, only outdone by early April’s.

The week was marked by “wait & see”/”hold on” as Monday opened the week up with a high wave doji and mediocre volume indicating a sense of complacency & uncertainty among market participants.

Tuesday advanced on weak volume, before another high wave doji on Wednesday for a decline on the second highest volume of the week that marked the high water mark.

Thursday opened on a gap down that tested the support of the 10 day moving average, but was able to advance in the end to close above $430/share.

Friday showed the cracks in DIA where the gap down open below the 10 day moving avearge’s resistance only carried lower, testing the support of the 200 day moving average & breaking down through the long-term trendline to close below it on the day.

Currently the 200 DMA is DIA’s likely main place to stay this week, osciallating around waiting for a catalyst to the upside or downside.

They’re currently not set up for upside or downside breakouts as most of the blue chip index owners have been sitting on their hands waiting for an upside/downside catalyst, which will continue into this week.

To the downside if there’sa breakdown keep an eye on the 50 day moving average’s support.

DIA has support at the $419.60 (Volume Sentiment: Buyers, 1.7:1), $416.41 (Volume Sentiment: Buyers, 1.7:1), $413.83 (Volume Sentiment: Sellers, 2.43:1) & $412.91/share (Volume Sentiment: Sellers, 2.43:1) price levels, with resistance at the $423.05 (200 Day Moving Average, Volume Sentiment: Sellers, 1.5:1), $423.12 (Volume Sentiment: Sellers, 1.5:1), $426.25 (Volume Sentiment: Buyers, 1.83:1) & $426.79/share (10 Day Moving Average, Volume Sentiment: Buyers, 1.83:1) price levels.

DIA ETF’s Price Level:VOlume Sentiment Over The Past ~4 Years

The Week Ahead

Monday the week kicks off with Empire State Manufacturing Survey data at 8:30 am.

Lennar is the only major earnings report on Monday, which will take place after the session’s close.

U.S. Retail Sales, Retail Sales minus Autos, Import Price Index & Import Price Index minus Fuel data are scheduled for release at 8:30 am on Tuesday, before Industrial Production & Capacity Utilization data at 9:15 am, and Business Inventories & Home Builder Confidence Index data at 10 am.

Tuesday begins with Jabil & Wiley reporting earnings before the session’s open, before La-Z-Boy’s report comes after the closing bell.

Wednesday will be an important day to watch, with Housing Starts, Building Permits & Initial Jobless Claims data due out at 8:30 am, followed by the FOMC Interest Rate Decision at 2pm & Fed Chair Powell’s Press Conference at 2:30 pm.

GMS & Korn/Ferry report earnings before Wednesday’s opening bell, with Smith & Wesson Brands reporting after the session’s close.

There is no economic data nor earnings reports scheduled for release on Thursday.

Friday the week winds down with Philadelphia Fed Manufacturing Survey Data at 8:30 am.

Darden Restaurants, Accenture, CarMax & Kroger all report earnings before Friday morning’s opening bell.

See you back here next week!

*** I DO NOT OWN SHARES OR OPTIONS CONTRACT POSITIONS IN SPY, QQQ, IWM OR DIA AT THE TIME OF PUBLISHING THIS ARTICLE ***

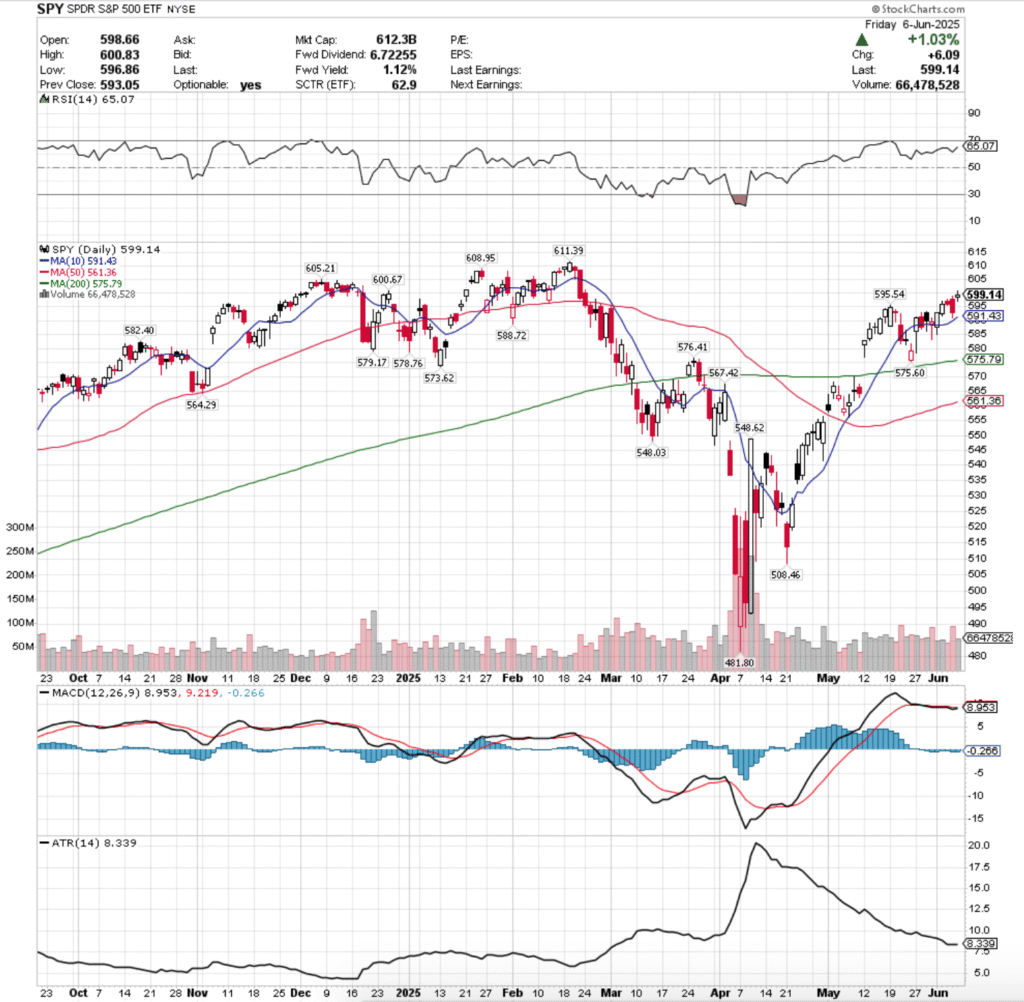

SPY, the SPDR S&P 500 ETF gained +1.65% last week, while the VIX closed the week at 16.77, indicating an implied move of +/-1.06% & an implied one month move of +/-4.85%.

SPY ETF – SPDR S&P 500 ETF’s Technical Performance Over The Past Year

Their RSI is trending higher towards overbought levels, sitting currently at 65.07, while their MACD is bearish, but is relatively flat in the wake of last week’s performance.

Volumes were +19.32% higher than the prior year’s average levels (68,316,000 vs. 57,254,701), which adds an interesting twist to the week, given that the highest volume session was a declining day.

Last week opened up on Monday in-line with the 10 day moving average, temporarily broke down through its support, before rallying into the close to close near the day’s high for a gain of +0.56%.

Tuesday that trend continued, as the session opened near Monday’s close & there was a risk-on appetite & SPY managed to close out +0.57%.

Wednesday is where trouble began to brew for SPY & market participants began to show a bit of anxiety & uncertainty, as the week’s lowest volume session resulted in a spinning top candle & closed -0.03% lower on the day after a gap up open.

The indecision marked by the spinning top is important, as SPY was <1% from that key resistance level of $600.67/share that we pointed out last week as an area of interest.

Thursday continued this, as SPY opened higher, before declining -0.48% on the strongest volume of the week & forming a bearish engulfing pattern with Wednesday’s candle.

While the support of the 10 day moving average managed to hold up, the day’s lower shadow indicates that there was a bit of unease among market participants & cracks were beginning to form.

Friday opened on a gap higher, but closed as a spinning top, indicating that there was quite a bit of indecision & uncertainty heading into the weekend, even though the session advanced +1.03%.

Friday’s high was able to temporarily break just above the previously noted $600.68/share resistance level, but was unable to gain any type of footing there & declined to close below it.

Heading into the new week, that will be a key area for any upside potential, as it is the gatekeeper for SPY’s all-time highs.

This level will likely be at least retested in the coming week, and as mentioned in prior months there will need to be a significant increase in consistent advancing volume to break above this resistance level.

Data for historic volume sentiment at these levels are skewed towards Buyers because of the nature of all-time highs, so it will require a more hands on approach to viewing trends in volume in the next week for any upside price movements.

There is a great deal of focus on today’s trade meeting between the US & China in London, as well as inflation data that comes in the form of CPI & PPI later this week.

There are also going to be clues about the state of the consumer when J.M. Smucker & Chewy report earnings, and Oracle’s report may also have potential to move the market in the short-term.

However, given that the Fed speakers have mostly all hinted at rates staying higher for longer/being in no rush to cut rates based on current data, it is difficult to see much of an upside catalyst in the near-term.

The consolidation case for SPY continues to be oscillations around the 10 day moving average until there is an upside or downside catalyst to force a breakout.

In the event that this is the way things play out, there is reason to watch the 50 day moving average’s approach to the 200 DMA, as a golden cross here may provide a temporary bump to SPY’s price as the medium-term trendline crosses over the long-term trend line bullishly.

In the event that his happens, pay attention to day-over-day volume trends to gain insight into how market participants are positioning themselves & what the future sentiment is likely to be.

To the downside there is an interesting set up, as over the past ~3 years the price zone that SPY is in has historically been dominated by the Sellers.

In the event that this trend continued they find support at the 10 day moving average, which is in a Buyer zone, as is their next support level as well.

Should these get tested though, the significance of the short-term trendline breaking down may force more selling in SPY (particularly if that 50 DMA golden cross doesn’t occur in the meantime) which then puts SPY’s next (4th) support level in a Seller zone.

In the event of decline, look at the 200 DMA’s support level, which sits -3.9% from the closing price of Friday’s session.

If the long-term trend is tested again & doesn’t hold up, we are likely going to see continued declines in the near-to-mid term.

The table below provides more volume sentiment data that may be useful in assessing the strength/weakness of support/resistance levels in re-tests.

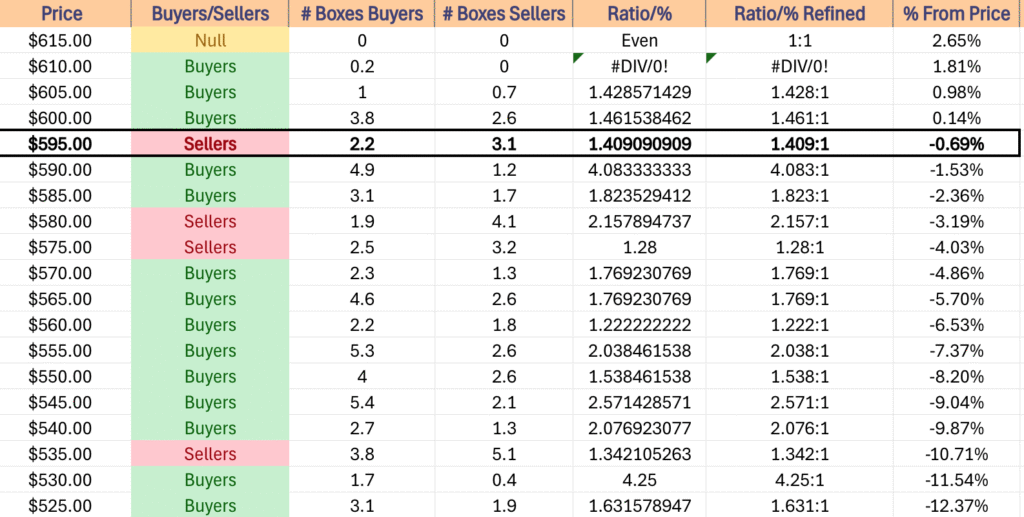

SPY has support at the $595.54 (Volume Sentiment: Sellers, 1.41:1), $591.43 (10 Day Moving Average, Volume Sentiment: Buyers, 4.08:1), $588.72 (Volume Sentiment: Buyers, 1.82:1) & $582.40/share (Volume Sentiment: Sellers, 2.16:1) price levels, with resistance at the $600.67 (Volume Sentiment: Buyers, 1.46:1), $605.21 (Volume Sentiment: Buyers, 1.43:1), $608.95 (Volume Sentiment: Buyers, 1.43:1) & $611.39/share (All-Time High, Volume Sentiment: Buyers, 1.43:1) price levels.

SPY ETF’s Price Level:Volume Sentiment Over The Past ~3 Years

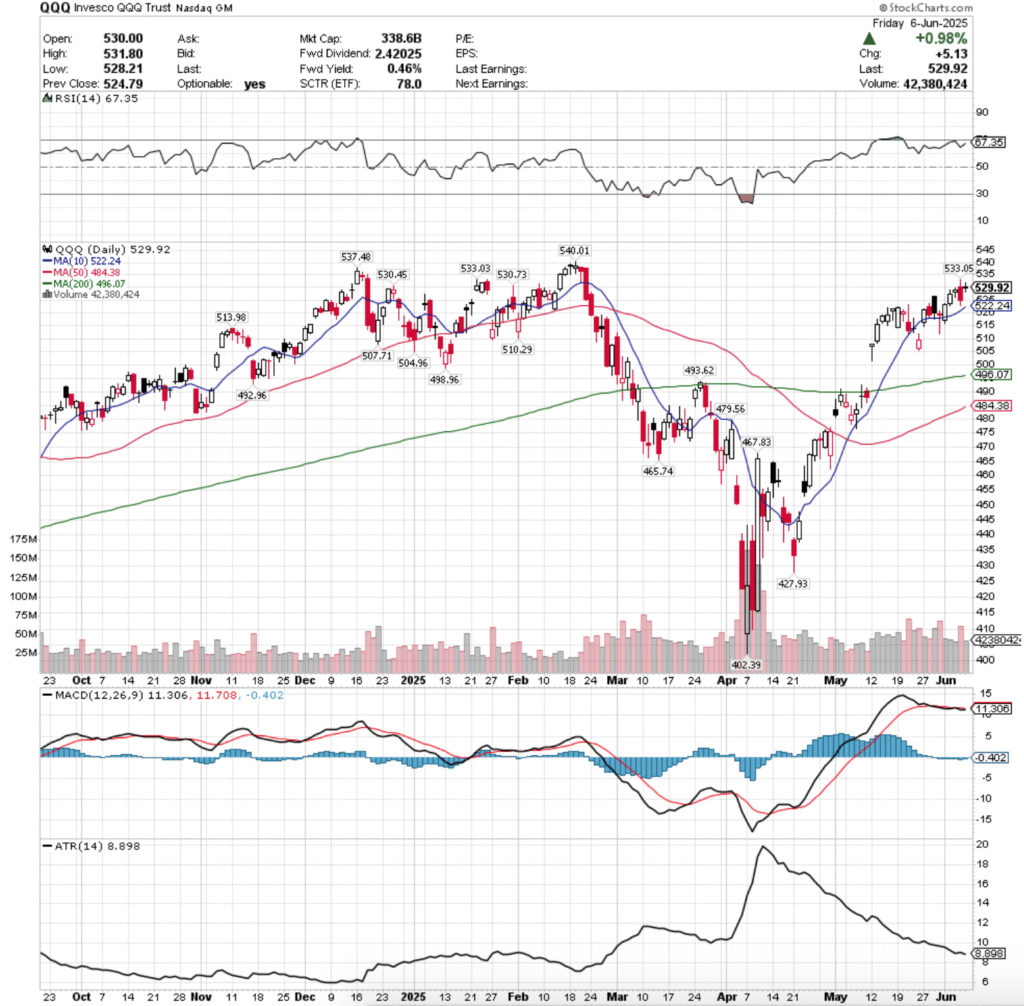

QQQ, the Invesco QQQ Trust ETF added +2.08% last week, as the tech-heavy index was able to muster some gains while closing in on its all-time high.

QQQ ETF – Invesco QQQ Trust ETF’s Technical Performance Over The Past Year

Their RSI is advancing towards the overbought level of 70, sitting currently at 67.35, while their MACD is bearish, but moving relatively flat after last week’s performance.

Volumes were +22.86% higher than the prior year’s average levels (46,790,000 vs. 38,083,028), which like SPY’s above has a little air of caution around it.

Monday QQQ opened just below the resistance of the 10 day moving average, but was able to break above it & close for an advancing session on the week’s second highest volume (highest for advancing sessions).

Tuesday opened on a gap higher & the march higher continued throughout the session, with the small lower shadow & longer upper shadow indicating that there had been a bit of profit taking during the session.

Wednesday though signaled a tale of caution on the horizon, as market participants began to be a little uneasy about how close QQQ had approached its all-time high & the session opened on a gap up, but closed as a hanging man candle (bearish).

Thursday confirmed this sentiment, when a gap higher open tested higher to reach $533.05/share, before profit taking commenced & QQQ formed a bearish engulfing pattern on a declining session with the week’s highest volume & QQQ closed down -0.75%.

The high volume can certainly be attributed to short-term & intraday profit taking, but it also is beginning to look like market participants are beginning to show signs of nervousness, as Friday’s candle showed.

Friday wound the week down in an interesting manner, as despite the session closing up +0.98%, there were many signs of weakness heading into the weekend.

Firstly, the session closed as a doji that’s real body was contained in the upper portion of Wednesday’s candle.

While the session advanced day-over-day, it closed lower than it opened, owing the adance to the jump in opening price from Thursday’s close.

This formed a bearish harami cross, indicating that there is still quite a bit of negative sentiment out there for QQQ & that there was a limited amount of risk being willing to be taken into the weekend.

This week, to the upside QQQ is still below the $530-530.99 & $533-533.99/share resistance zones as of Friday’s close, which will be the primary target to watch.

The good news, is that there is Buyer sentiment historically in these zones, but the bad news is that it is attributed to the fact that they’re so close to QQQ’s all-time high, so the ratio will ultimately be diluted over time & re-tests.

Like SPY, there will need to be sustainable, higher advancing volumes in the coming week to power through those zones higher & should they be broken above but volumes are weak the rally should be viewed with skeptical brow.

It will also be wise to watch the 50 DMA as it approaches the 200 DMA, as in the event of a golden cross there may be a bump to the upside as the mdeium-term trendline crosses bullishly through the long-term trend line.

The consolidation case is still oscillations around the 10 day moving average, with a keen eye open in the event that we see an island top from the gap in early May.

In the event that there is downside movement, look to see that window be filled, with a re-test of the 200 day moving average likely, especially given the Seller pressure below Friday’s closing price.

Should we get one, the 200 DMA is in a Seller dominated zone historically, which adds a bit of trouble for the long-term trend.

The table below can help assess the strength/weakness of QQQ’s support/resistance levels in the event of re-tests.

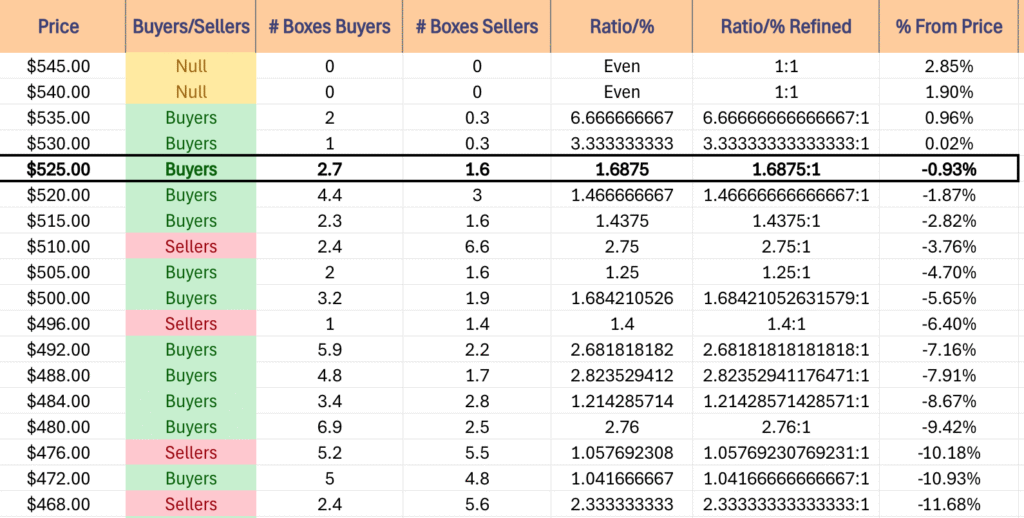

QQQ has support at the $522.24 (10 Day Moving Average, Volume Sentiment: Buyers, 1.47:1), $513.98 (Volume Sentiment: Sellers, 2.75:1), $510.29 (Volume Sentiment: Sellers, 2.75:1) & $507.71/share (Volume Sentiment: Buyers, 1.25:1) price levels, with resistance at the $530.45 (Volume Sentiment: Buyers, 3.33:1), $530.73 (Volume Sentiment: Buyers, 3.33:1), $533.03 (Volume Sentiment: Buyers, 3.33:1) & $533.05/share (Volume Sentiment: Buyers, 3.33:1) price levels.

QQQ ETF’s Price Level:Volume Sentiment Over The Past ~1 Year

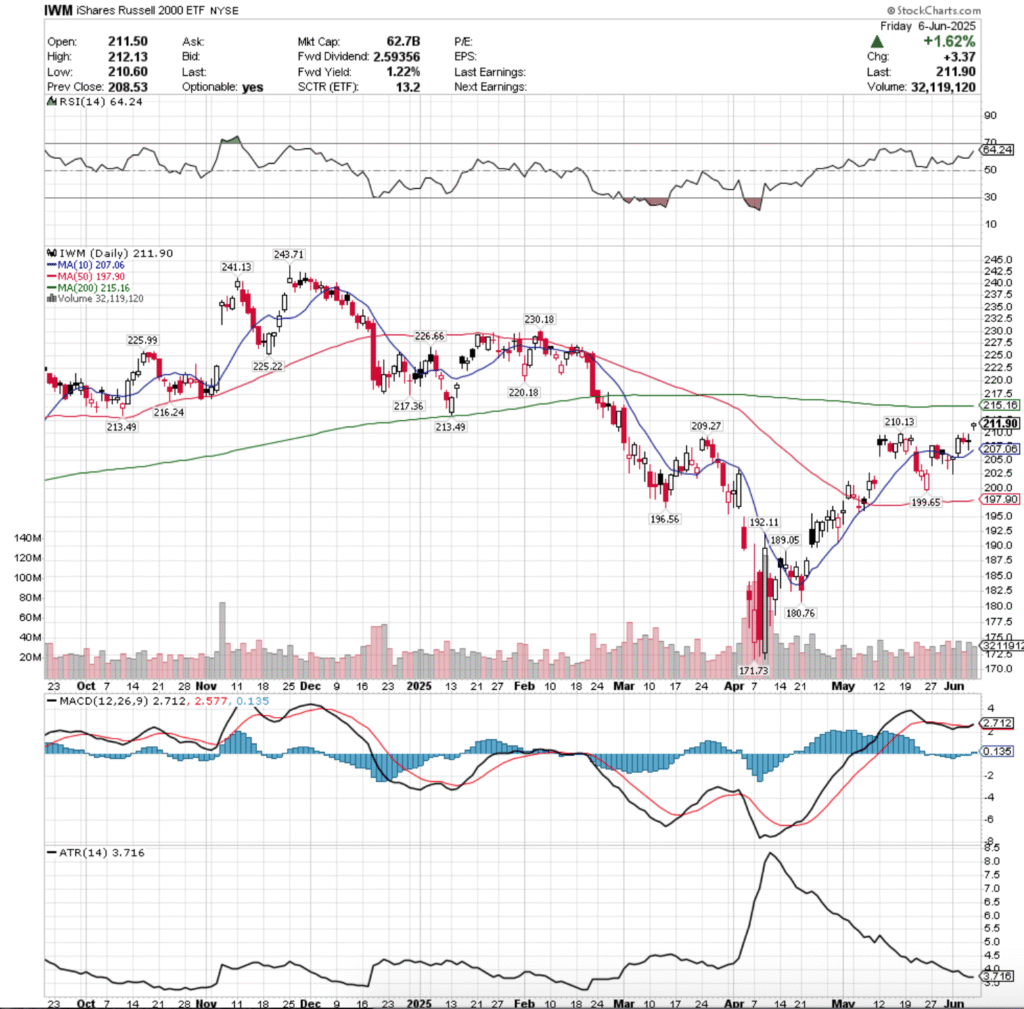

IWM, the iShares Russell 2000 ETF advanced +3.33% last week, faring the strongest of the major four index ETFs after a few slumping weeks at the back of the pack.

IWM ETF – iShares Russell 2000 ETF’s Technical Performance Over The Past Year

Their RSI is trending higher towards overbought levels, sitting currently at 64.24, while their MACD crossed over bullishly on Friday on account of the day’s gap up session.

Volumes were +7.83% higher than the prior year’s average (32,636,000 vs. 30,265,697), which while IWM advanced the most last week, is not necessarily a great picture given the gappy nature of the week.

Monday the small cap index opened below the 10 DMA, tested down to ~$202.50, before ending the day as a hammer candle & signaling that there was a bit of juice in the tank for IWM after weeks of underperforming the 3 other majors.

Tuesday opened on a gap up, tested briefly down to the support of the 10 day moving average, before powering higher on the highest volume of the week.

Wednesday saw some profits taking after the gains of the previous two days, as the day’s high was $210.01 & from there saw losses, closing down day-over-day -0.28%.

Wednesday’s volume was the lowest of the week, but given the underperformance that IWM has had relative to the other major indexes that’s not necessarily a bad sign.

Thursday saw another high volume session similar to Monday’s, but the day closed +0.04% as a doji, indicating that there was a bit of uncertainty looming over IWM.

This was confirmed Friday when IWM opened on a gap up, stayed within a relatively tight range for the day & closed out as a hanging man.

This indicated that there was not much interest in carrying risk into the weekend, and also formed a window that will need to be closed in the coming week(s).

The upside case for IWM moving forward relies around whether or not they can break above the 200 day moving average, changing their long-term trend.

This brings with itself some challenges, as the 200 DMA & the resistance level between it & the price both reside in Seller dominated price zones, which will require a bit of advancing volume to get through.

The consolidation case looks currently like oscillations around the 10 DMA, dipping into the window caused by Friday & breaching closer to the 200 DMA until we see a downside or upside catalyst.

The downside case occurs if there is some declining momentum as IWM fills Friday’s gap, which in turn would turn attention to he $199.65/share support level & the 50 day moving average.

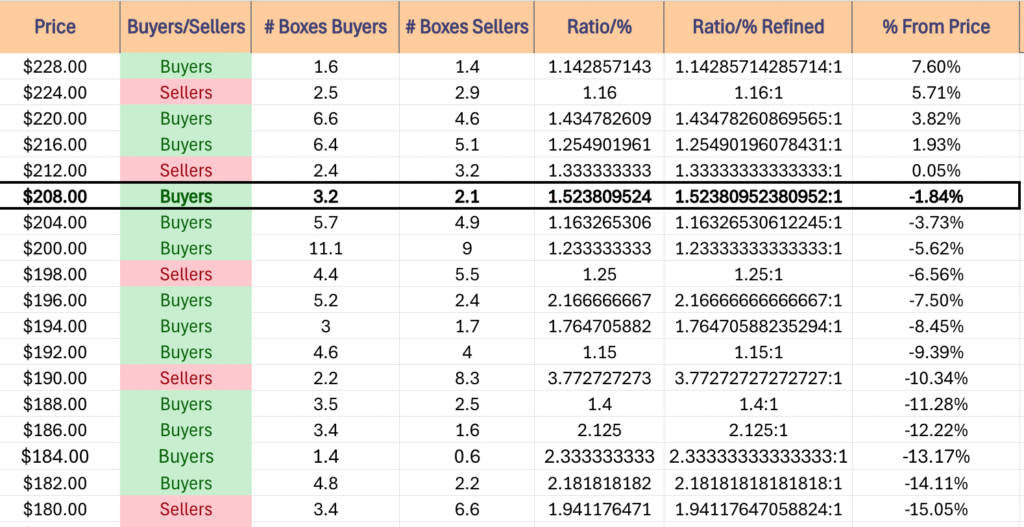

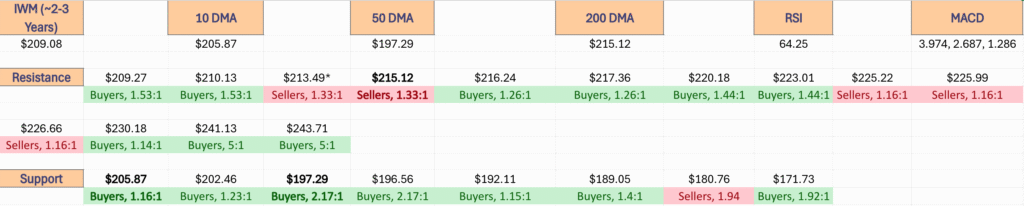

IWM has support at the $210.13 (Volume Sentiment: Buyers, 1.52:1), $209.27 (Volume Sentiment: Buyers, 1.52:1), $207.06 (10 Day Moving Average, Volume Sentiment: Buyers, 1.16:1) & $199.65/share (Volume Sentiment: Sellers, 1.25:1) price levels, with resistance at the $213.49* (2 Touch-Points, Volume Sentiment: Sellers, 1.33:1), $215.16 (200 Day Moving Average, Volume Sentiment: Sellers, 1.33:1), $216.24 (Volume Sentiment: Buyers, 1.26:1) & $217.36/share (Volume Sentiment: Buyers, 1.26:1) price levels.

IWM ETF’s Price Level:Volume Sentiment Over The Past ~2-3 Years

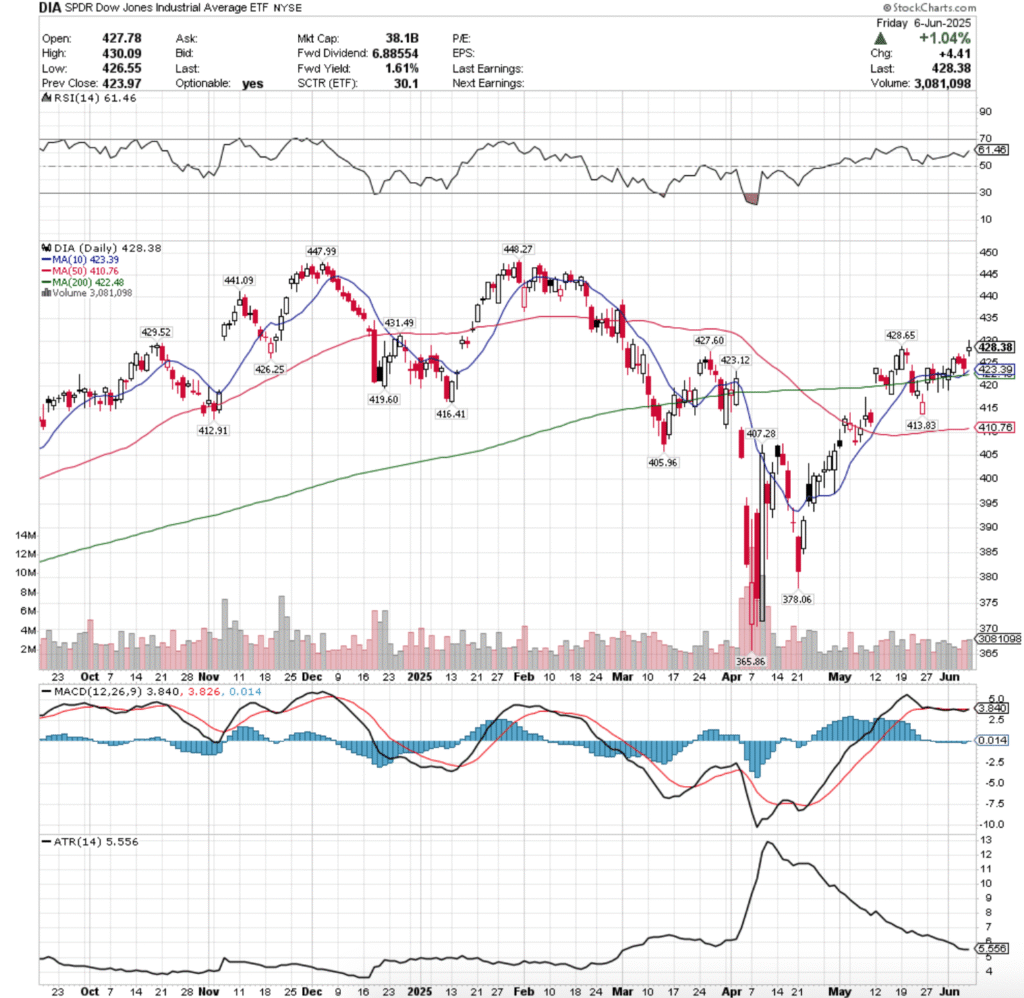

DIA ETF – SPDR Dow Jones Industrial Average ETF’s Technical Performance Over The Past Year

Their RSI is climbing higher & currently at 61.46, while their MACD is bearish but flat after the consolidation period of most of May that DIA’s been in.

Volumes were -16.28% lower than the prior year’s average (2,652,000 vs. 3,167,729), indicating that the “Buy & Hold” sentiment mentioned in the previous few weeks’ notes is still alive & well as the blue chip index investors are in a state of uncertainty.

DIA began the week just below its 10 day moving average’s resistance, tested below $420/share, before advancing to break out above all of its moving averages.

Tuesday followed suit & tested lower briefly, but support of the 10 & 200 DMA’s held up, enabling DIA to advance & close above $425/share.

Wednesday exposed that there was still some doubts about DIA’s strength, as the session opened higher, but profit taking quickly forced prices lower for a declining session.

Thursday was much the same, but market participants didn’t let DIA cross bearishly across the 10 & 200 day moving averages, but the day resulted in a decline, as the profit taking fueled the second highest volume session of the week.

Friday looked an awful lot like IWM’s chart (not surprising, as we’ve been noting now here weekly it seems), where DIA opened on a gap up, temporarily broke above the $430/share level, but ended the session as a spinning top candle on the week’s highest volume.

While that participation rate heading into a weekend might be seen by some as a sign of optimism & bullishness, looking at the declining volume of the two prior days doesn’t inspire a lot of confidence.

To the upside, the $428.65/share level will be an area of interest, along with the $429.52 & $431.49/share price levels.

These are historically Buyer dominated levels, but DIA has been more skewed towards Buyers in general as the Blue Chip index has maintained demand over the years as a safer haven than other indexes.

In the event that these levels are broken through, the $440-443.99/share zone is Seller dominated historically, which will pose an interesting problem for DIA, as it is the gatekeeper to their all-time high.

The consolidation case here looks interesting, as it involved oscillations around the 10 & 200 DMA’s simultaneously, awaiting the catalyst to the upside or the downside.

The overall market sentiment will be especially apparent based on what happens should that situation occur, as the proximity between the long & short term trend lines is quite narrow.

Any move towards the downside will be interesting to watch, as there’s solid Buyer sentiment at their next two support levels, before the following two enter Seller territory, and then the 50 day moving average comes into view.

If the 50 DMA is tested & breaks down, the $405.96/share level is the next place to begin looking for DIA, but this of course assumes a decline.

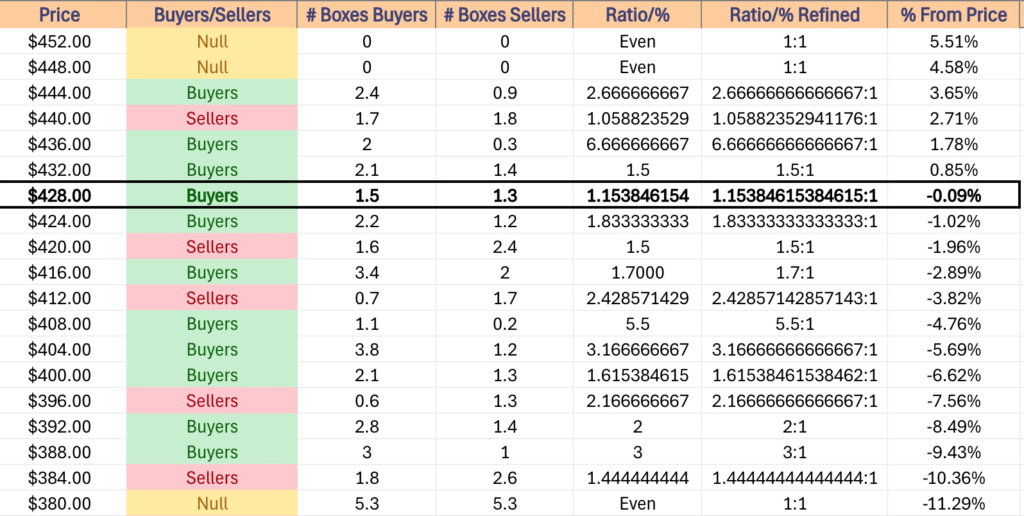

DIA has support at the $427.60 (Volume Sentiment: Buyers, 1.83:1), $426.25 (Volume Sentiment: Buyers, 1.83:1), $423.39 (10 Day Moving Average, Volume Sentiment: Sellers, 1.5:1) & $423.12/share (Volume Sentiment: Sellers, 1.5:1) price levels, with resistance at the $428.69 (Volume Sentiment: Buyers, 1.15:1), $429.52 (Volume Sentiment: Buyers, 1.15:1), $431.49 (Volume Sentiment: Buyers, 1.15:1) & $441.09/share (Volume Sentiment: Sellers, 1.06:1) price levels.

DIA ETF’s Price Level:Volume Sentiment Over The Past ~4-5 Years

The Week Ahead

Monday kicks the new week off with Wholesale Inventories data at 10 am.

Calavo Growers & Casey’s General report earnings after Monday’s close.

NFIB Optimism Index data is released on Tuesday at 6 am.

Academy Sports + Outdoors, Core & Main, J.M. Smucker & United Natural Foods report earnings before Tuesday’s opening bell, with GameStop, Dave & Buster’s, GitLab & Stitch Fix all reporting after the session’s close.

Wednesday gives us insight into inflation with Consumer Price Index, Core CPI, CPI Year-over-Year & Core CPI Year-over-Year data at 8:30 am, before Monthly U.S. Federal Budget data at 2pm.

Chewy & SailPoint report earnings before Wednesday’s opening bell, followed by Oracle & Oxford Industries after the closing bell.

Initial Jobless Claims, Producer Price Index, Core PPI, PPI Year-over-Year & Core PPI YEar-over-Year data are released Thursday at 8:30 am.

Lovesac reports earnings on Thursday before the session opens, followed by Adobe & RH after the session’s close.

Friday the week winds down with Consumer Sentiment (prelim) data at 10 am.

There are no major earnings reports due out of Friday.

See you back here next week!

*** I DO NOT OWN SHARES OR OPTIONS CONTRACT POSITIONS IN SPY, QQQ, IWM OR DIA AT THE TIME OF PUBLISHING THIS ARTICLE ***

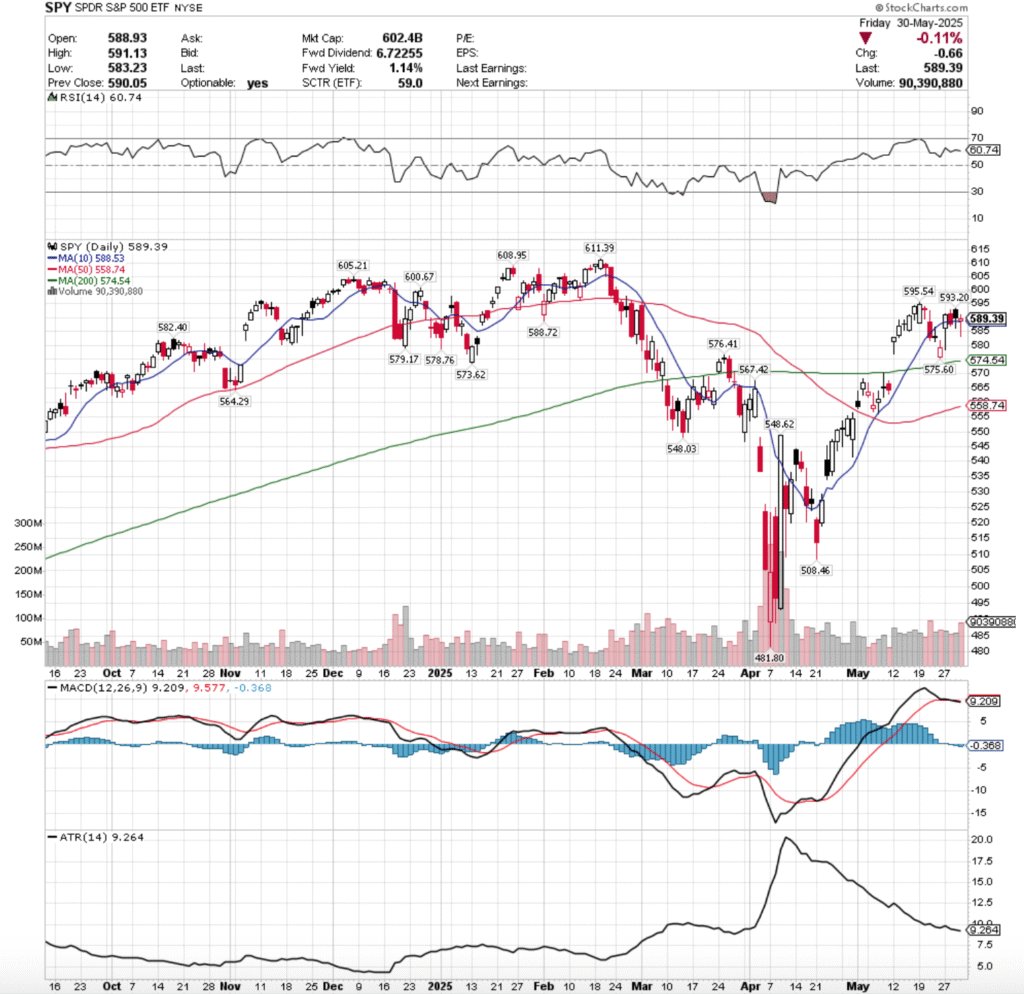

SPY, the SPDR S&P 500 ETF gained +1.78% last week, while the VIX closed the week at 18.57, indicating an implied one day move of +/-1.17% & an implied one month move of +/-5.37%.

SPY ETF – SPDR S&P 500 ETF’s Technical Performance Over The Past Year

Their RSI is relatively flat after last week’s limited price range, currently sitting at 60.74, while their MACD crossed over bearishly, but is also relatively flat.

Volumes were +32.73% above the prior year’s average (75,427,500 vs. 56,826,680), which is an area for concern given the highest volume session was Friday’s profit taking decline & two other sessions were cause for concern (75% of the week, given it was a holiday week).

Tuesday the week opened on a gap up, but with very shaky footing beneath it.

While the day closed as a +2.08% advancing session, the day’s low had retraced the entire gap range & into Friday’s candle’s body below Friday’s closing price.

While this occurred on the second highest volume of the week, it looked a lot more like an intra-day profit grab on a shortened week vs. an actual solid advancing session.

Wednesday opened slightly higher, but was pulled back down & ultimately broke down though the support of the 10 day moving average, indicating that the short-term trend is possibly in trouble.

Thursday reinforced this hazy outlook for SPY, when on an opening gap up there was no footing to be found & intraday the support of the 10 DMA broke down again as shown by the candle’s lower shadow.

The combination of the week’s second lowest volume, the deep intraday breakdown of the 10 DMA’s support, even if only temporary & the close being lower than the day’s open are all causes for concern, as market participants are clearly not thinking we’re out of the woods just yet.

Friday also did little to inspire confidence for SPY, as the week’s highest volume session opened below Thursday’s closing price, dropped temporarily intraday to below $585/share, before managing to advance above the day’s open into the close, but still resulted in a decline of -0.11%.

The high volume isn’t as bad in this instance as it may have been viewed in an outright declining day, given that there was a good amount of shares changing hands, folks taking profits & some folks buying back in in anticipation of this coming week, which will have aslew of Fed speakers & also some data points that will shed insight into the state of employment & manufacturing in the U.S..

What is alarming though is that the session opened just above the 10 DMA’s support, managed to break down through it -0.97% to the day’s low, and then saw the close wind up just marginally above the day’s open.

The Day-over-Day change in lows is also an area of concern heading into the new week, as it is exposing that there is more & more downside appetite among market participants.

In last week’s market review note we noted that there was going to be an interesting Seller zone cross through in order for price to re-test the 10 DMA & then ultimately if broken through, test the strength of it as a support level.

Most of that was accomplished by Tuesday morning’s gap up open, which should be tread carefully around given that the volume level was second highest of a 4 day week, but nothing that expressed proper conviction behind the move & it’s likely not sustainable.

This week, to the upside there will need to be the same sustainable high advancing volume levels mentioned over the past months now, but the $600.67 mark is an area to watch.

Should prices test this level it means having passed through a Seller zone to the upside, and there may be some high participation that forces prices to continue higher.

In the event of further consolidation, expect price to continue to oscillate around the 10 day moving average as we await a catalyst to the upside or downside.

In the event that it takes a few weeks to reach one (highly doubtful), there may be a slight bump to the upside from the 50 DMA crossing over the 200 DMA bullishly, but this is an extreme case example.

To the downside, the 200 day moving average is an area all eyes should be focused on, as the long-term trendline was only crossed over on a gap up, which was somewhat speculative.

How market participants think of the price in relation to the long-term trend is going to be a key area to watch.

While the past few years show that price zones down to $574.99/share have been Seller dominated, there may be some footing to be found once price has dropped below there, which would alleviate concerns of the 200 DMA being re-tested, but it is certainly an area to be watching.

Price will like oscillate between the 10 & 200 DMAs for a while while we await a further up/downside catalyst in the event that this decline takes place.

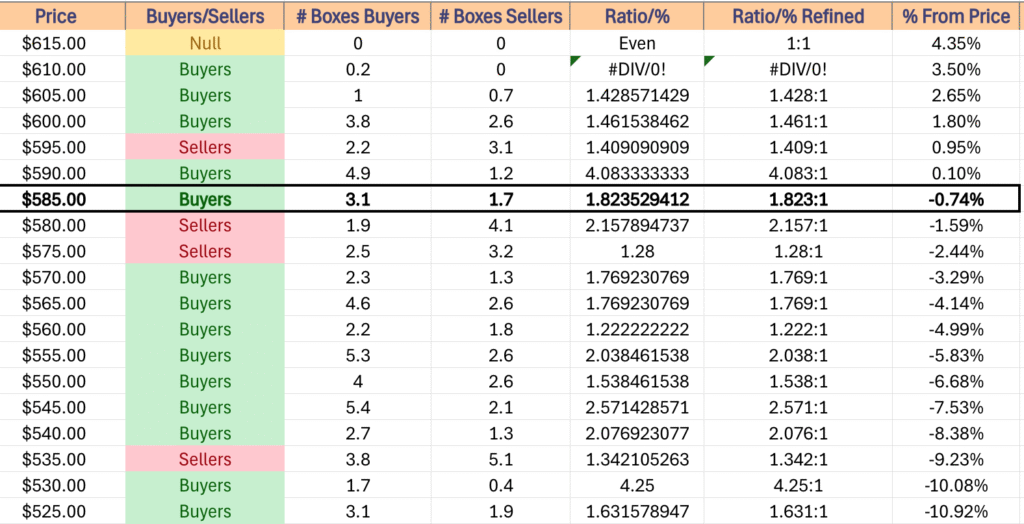

SPY has support at the $588.72 (Volume Sentiment: Buyers, 1.82:1), $588.53 (10 Day Moving Average, Volume Sentiment: Buyers, 1.82:1), $582.40 (Volume Sentiment: Sellers, 2.16:1) & $579.17/share (Volume Sentiment: Sellers, 1.28:1) price levels, with resistance at the $593.20 (Volume Sentiment: Buyers, 4.08:1), $595.54 (Volume Sentiment: Sellers, 1.41:1), $600.67 (Volume Sentiment: Buyers, 1.46:1) & $605.21/share (Volume Sentiment: Buyers, 1.43:1) price levels.

SPY ETF’s Price Level:Volume Sentiment Over The Past ~3 Years

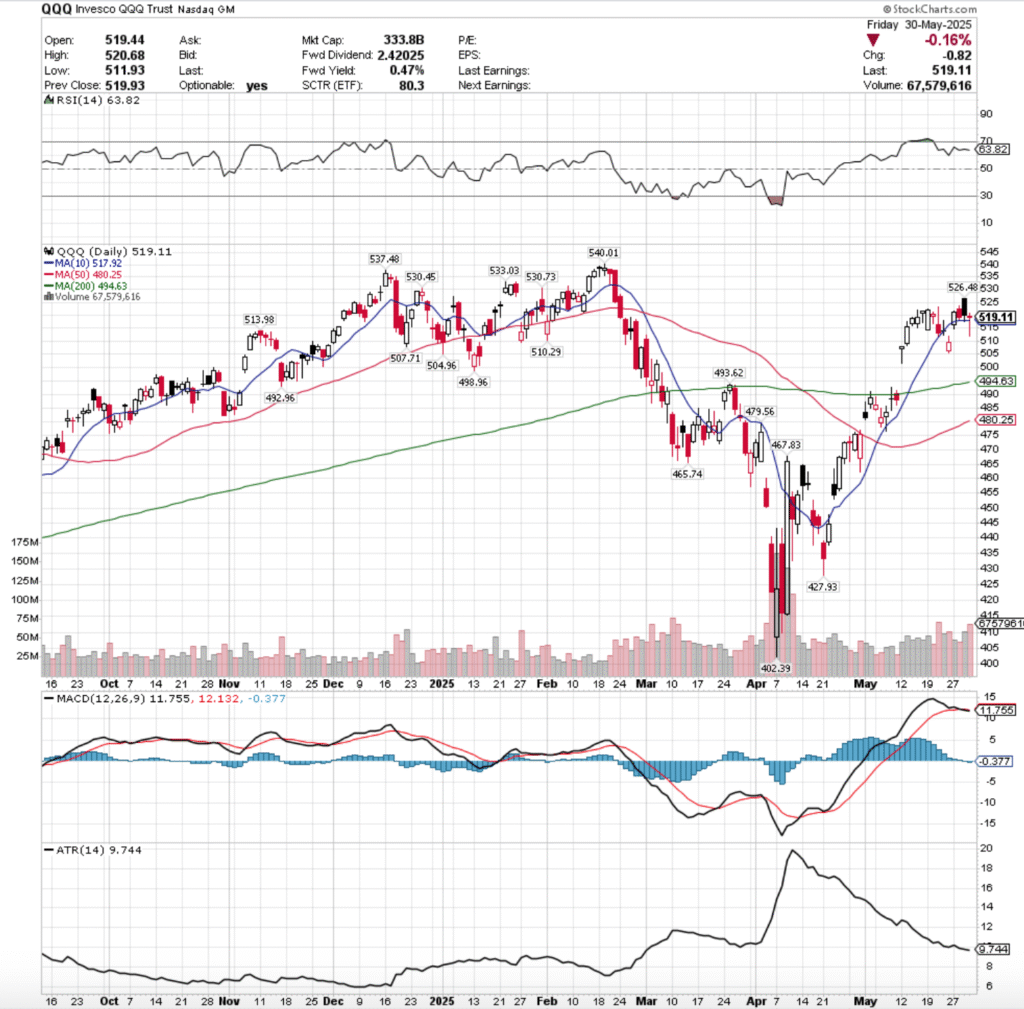

QQQ, the Invesco QQQ Trust ETF advanced +1.94% for the week, as the tech-heavy index was the favorite of the major four index ETFs.

QQQ ETF – Invesco QQQ Trust ETF’s Technical Performance Over The Past Year

Their RSI has flattened out following last week as well, but currently sits at 63.82, while their MACD is bearish.

Volumes were +45.75% higher than the prior year’s average (55,062,500 vs. 37,779,012), which paints a similar problem as the one mentioned above for SPY.

Tuesday the week opened up a similar gap up, gaining +2.35% on the day on the second lowest volume of the week.

It opened just beneath the 10 day moving average’s support, temporarily dipped below the $515/share level on the low end of the day’s range, before gaining some steam & powering higher to close setting the stage for the week to be above the 10 DMA.

Wednesday opened on a gap higher, tested slightly higher as displayed on their upper shadow, but declined the rest of the day to re-test the 10 day moving average’s support, which was able to hold up & force the day to close above it, despite declining -0.44% on the day.

Thursday is where the concern really began though & cracks began to show, as the session opened on a gap higher, but it was mostly downhill from there.

QQQ declined to dip beneath the support of the 10 day moving average, but was able to rally higher to close lower on the day than it opened, but still for a day-over-day gain of +0.2%.

Thursday was the second highest volume day of the week, and while it can be said that it covered a wide range of prices, it can also be said that it was a day of heavy profit-taking, which reflects negative sentiment & calls into question the strength of the short-term trend line (10 day moving average).

Friday confirmed that there was a bit of blood in the water, as QQQ opened lower, briefly tested to the upside, but was rejected near the close of Thursday’s session, and prices free-fell in a profit taking bonanza that dropped QQQ down to $511.93/share during the day’s low.

While prices climbed back to close the day as a dragonfly doji, this downside appetite doesn’t inspire confidence in the tech-heavy index.

Given the proximity of the short-term trend line & the new downside appetite that made a run at closing the window of Tuesday’s gap (assuming it closed near the lows), it is going to be worth watching for a rugpull in the coming week.

To the upside there are two place to watch, first being the $526.48 level & second being the resistance zone in the $530-531/share level.

While the table below shows that this is all Buyer oriented historically, this looks primed to be a time of ratio dilution with Sellers stepping in, so there will need to be some solid volume behind any upwards moves to make them sustain.

The consolidation case looks like a bit of oscillating around the 10 DMA awaiting an upside/downside catalyst, with a chance up a slight uptick when the 50 DMA crosses bullishly over the 200 DMA, but that’s weeks away, should it occur.

The downside view looks tricky, as in the event that the first support levels of $517.92 breaks down, we enter a Seller zone with two support levels, which should they break down may become problematic, given the window from early May that needs to be closed.

In the event that the gap begins to fill, the strength of the long-term trend line (200 DMA) is going to be key, but more likely to be determined by recent candles near the approach & their volume trends.

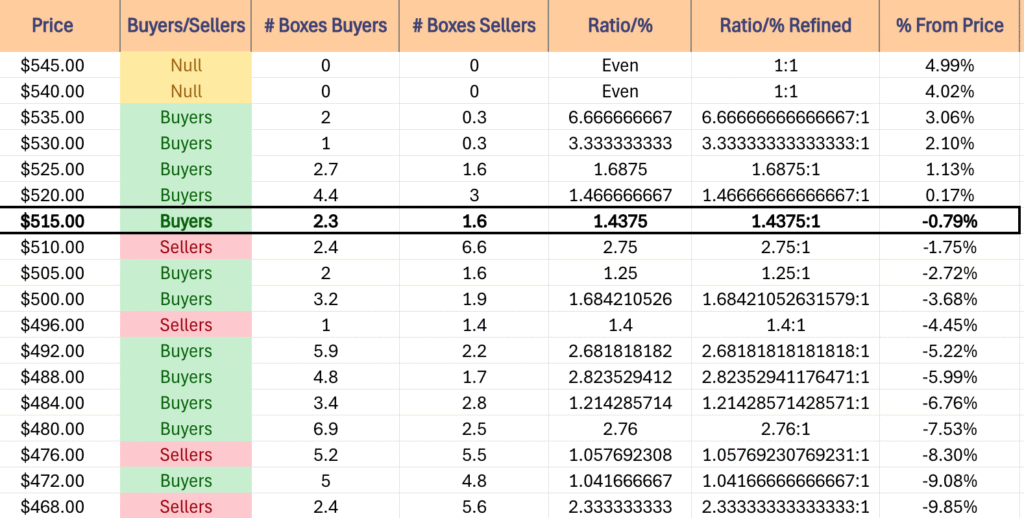

QQQ has support at the $517.92 (10 Day Moving Average, Volume Sentiment: Buyers, 1.44:1), $513.98 (Volume Sentiment: Sellers, 2.75:1), $510.29 (Volume Sentiment: Sellers, 2.75:1) & $507.71/share (Volume Sentiment: Buyers, 1.25:1) price levels, with resistance at the $526.48 (Volume Sentiment: Buyers, 1.69:1), $530.45 (Volume Sentiment: Buyers, 3.33:1), $530.73 (Volume Sentiment: Buyers, 3.33:1) & $533.03/share (Volume Sentiment: Buyers, 3.33:1) price levels.

QQQ ETF’s Price Level:Volume Sentiment Over The Past ~1 Year

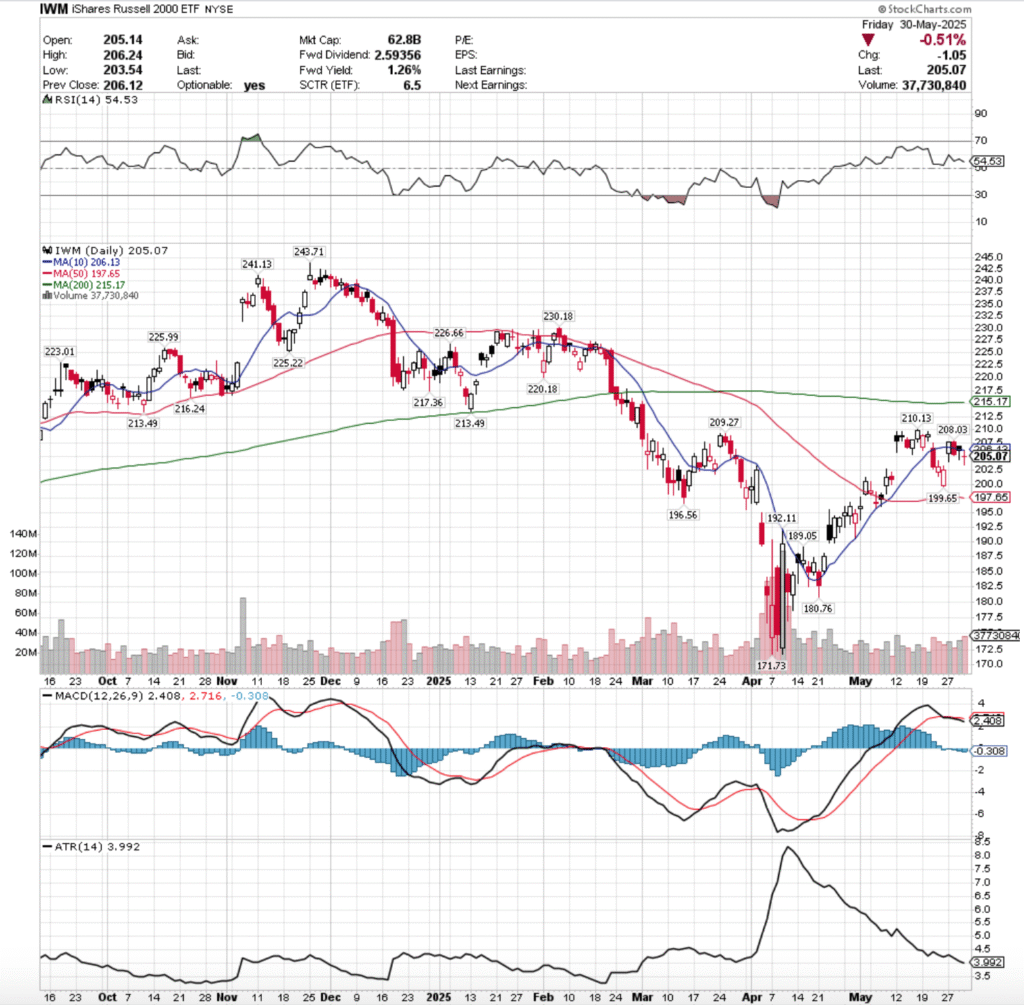

IWM ETF – iShares Russell 2000 ETF’s Technical Performance Over The Past Year

Their RSI is trending down towards the neutral 50-mark, currently sitting at 54.53, while their MACD is bearish, but has been relatively flat awaiting a catalyst for the past week.

Volumes were +6.82% above the prior year’s average level (32,070,000 vs. 30,022,411), which like the two aforementioned index ETFs is a cause for concern for IWM & its components.

The story of the week for IWM is similar to SPY & QQQ, however the 10 DMA did not prevail, which is slight cause for concern for the other two indexes.

While IWM is expected to lag them/be more of a slow grower with more oscillations on the way up, the short-term trendline’s breakdown paints a broad weak picture for the others.

Tuesday opened on a gap up, tested lower intra-day, but was able to power higher & close above the support of the 10 day moving average despite opening the day below it.

Wednesday opened in linen with Tuesday’s close, but made short work of sinking down through the 10 DMA’s support on the week’s weakest volume.

Thursday had a unique set up that signaled there was impending trouble on the horizon for IWM.

The session opened midway through Wednesday’s range, then broke out to the downside & was able to close lower than the open but above the day’s low & in-line with the 10 DMA.

Friday the week wound down on a week of skeptical uncertainty, as the week;s highest volume session resulted in a doji candle that opened on a gap lower, was unable to break out above the 10 DMA’s resistance to the upside, and a lot of profits were taken based on the amount of shares that exchanged hands over the last session of the week.

IWM is in a unique spot as it is more influenced by the larger cap indexes at the moment, as the uncertainty we’re surrounded by has folks not eager to jump into small cap names that are relatively unheard of.

As a result, the long-term trend line is the area of focus on the upside, given their state of limbo & that they’re trading below it.

Like SPY & QQQ, they’re going to need an influx in sustainable advancing volume to make a run at the 200 DMA’s resistance, so it’s something to keep an eye on, but not a focal point of IWM’s near-term performance.

In the consolidation case, we’ll see oscillations around the 10 DMA, which may wind up testing some of the other nearby support/resistance levels, which may cause the consolidation range to change, but the oscillations to continue.

The downside case brings all eyes on the 50 day moving average’s support, given that IWM is trading below its long & short-term trendlines.

Seller sentiment can bring IWM to the $197.99/share level, which would place it in the neighborhood of said re-test, which is a safe place to look in the coming week or two.

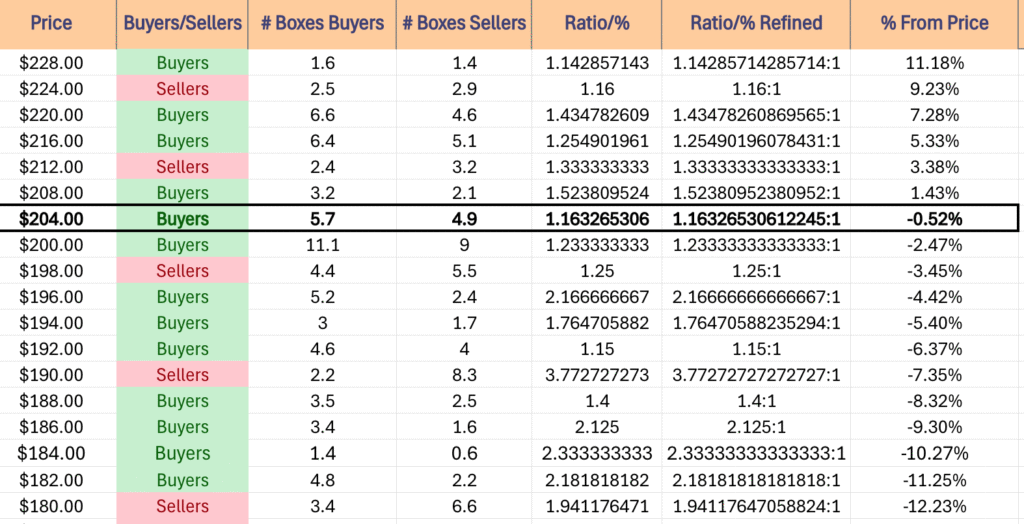

IWM has support at the $199.65 (Volume Sentiment: Sellers, 1.25:1), $197.65 (Volume Sentiment: Buyers, 2.17:1), $196.56 (Volume Sentiment: Buyers, 2.17:1) & $192.11/share (Volume Sentiment: Buyers, 1.15:1) price levels, with resistance at the $206.13 (10 Day Moving Average, Volume Sentiment: Buyers, 1.16:1), $208.03 (Volume Sentiment: Buyers, 1.52:1), $209.27 (Volume Sentiment: Buyers, 1.52:1) & $210.13/share (Volume Sentiment: Buyers, 1.52:1) price levels.

IWM ETF’s Price Level:Volume Sentiment Over The Past ~2-3 Years

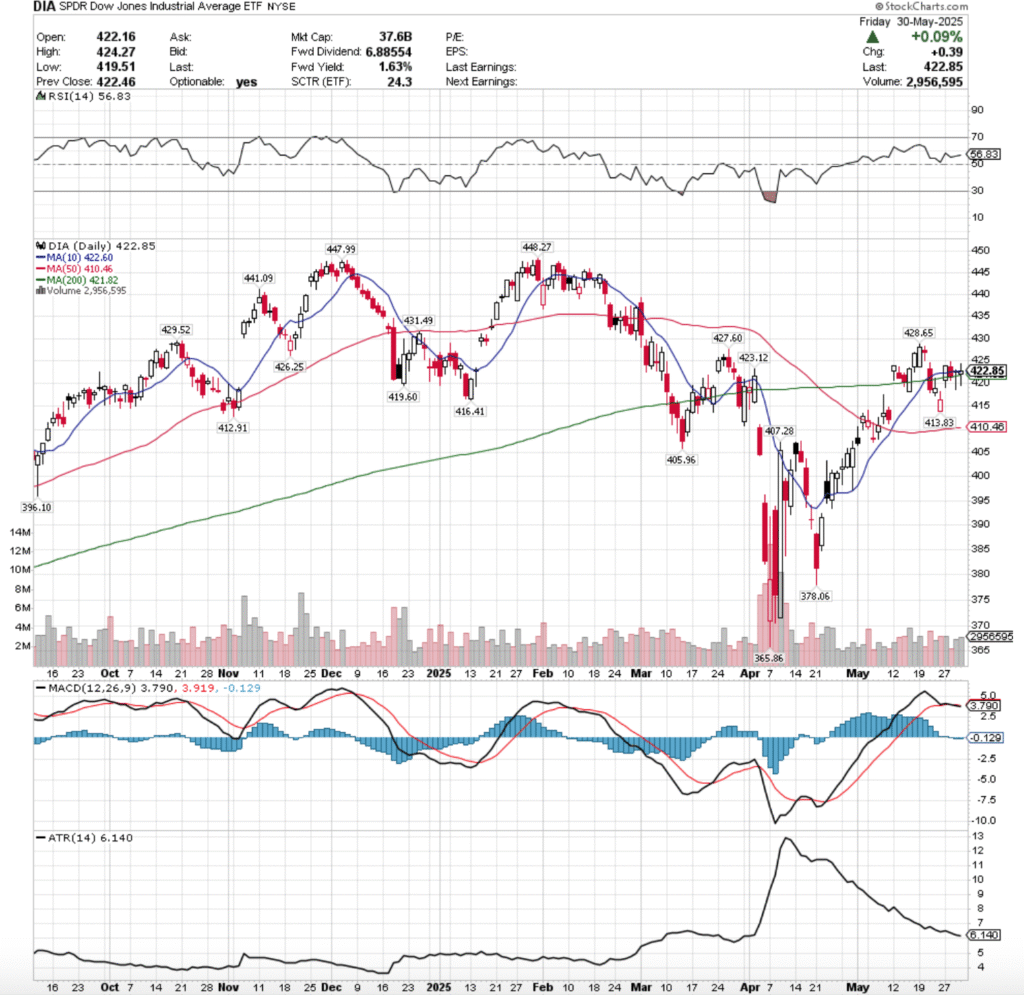

DIA, the SPDR Dow Jones Industrial Average ETF climbed +1.57% last week, but there was an air of caution based on volume levels, as we continue to see a more “buy & hold”/”wait & see” approach from the blue chip index.

DIA ETF – SPDR Dow Jones Industrial Average ETF’s Technical Performance Over The Past Year

Their RSI is currently 56.83, while their MACD is bearish, but relatively flat following last week’s consolidation range.

Volumes were -16.39% lower than the prior year’s average level (2,657,500 vs. 3,178,498), signaling that there are a lot of market participants in “wait & see” mode with the blue chip index & its components.

DIA’s week opened Tuesday with more volume than its peers comparitively speaking & was a gap up open that was able to break above the resistance of the 200 day moving average, but not until after it showed that it had a bit of downside appetite down to the $419.19/share level.

Wednesday opened slightly lower, tried to rip higher, but ultimately sank down to close just above the 200 DMA, after briefly breaking through it to the downside, but forming a bearish harami pattern with Tuesday’s candle.

Thursday things continued to be interesting, as the day opened & closed as technically a bullish harami cross, but there was a major catch.

While the daily candle is a dragonfly doji, looking closely there are a few causes for concern, namely that the session opened & closed in-line with the short-term trendline, but intraday its support broke down, as did the support of the long-term trend line.

Given that the volume was the second lowest of the week but that wide of a price range was covered there is reason for doubt regarding the near-term for DIA.

Friday didn’t settle this fear, opening lower near the 200 DMA’s support, dropping below the $420/share level, before advancing to just short of the $425/share price level & closing just beneath it as a spinning top candle.

The indecision marked by the day’s candle sets the stage for an interesting week.

To the upside, the first resistance levels is in a Seller dominated zone (table below), which as mentioned now for months will require a steady, consistent uptick in advancing volume to break above, even if this past week’s consolidation does become a launch pad.

From there, the high water mark becomes the $431.49/share level, which while there is historic Buyer sentiment all the way up to it, it wanes after the next price level, which makes it worth keeping an eye out to see if Sellers step in, rejecting an advance & diluting the historic ratio.

The consolidation case should prices not break the next resistance levels looks similar to what last week delivered, and shows DIA oscillating around the 10 & 200 day moving averages until we see an upside or downside catalyst.

An area of caution though for that scenario is that we are in a Buyer dominated price zone historically, and that may mean that any slight slips wind up leading to larger declines than expected.

In the event of a downside catalyst, the next two support levels are in a Seller dominated historic price zone.

Should both the long & short term trendlines (10 & 200 DMAs) break down & these levels can’t foot support, watch for the windows created in May to be filled & prices revert towards the 50 day moving average’s support.

Watching Volume levels & comparing them with the historic sentiments in the table below will be beneficial in navigating these markets.

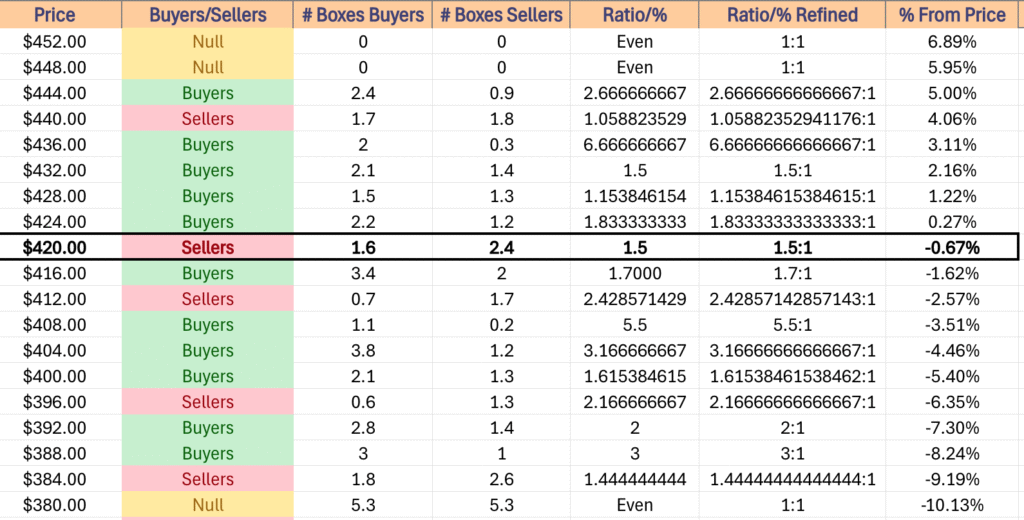

DIA has support at the $422.60 (10 Day Moving Average, Volume Sentiment: Sellers, 1.5:1), $421.82 (200 Day Moving Average, Volume Sentiment: Sellers, 1.5:1), $419.60 (Volume Sentiment: Buyers, 1.7:1) & $416.41/share (Volume Sentiment: Buyers, 1.7:1) price levels, with resistance at the $423.12 (Volume Sentiment: Sellers, 1.5:1), $426.25 (Volume Sentiment: Buyers, 1.83:1), $427.60 (Volume Sentiment: Buyers, 1.83:1) & $428.65/share (Volume Sentiment: Buyers, 1.15:1) price levels.

DIA ETF’s Price Level:Volume Sentiment Over The Past ~4-5 Years

The Week Ahead

Monday kicks the week off with S&P Final Manufacturing PMI data at 9:45 am, ISM Manufacturing data comes out at 10 am along with Construction Spending data, Fed President Logan speaks at 10:15 am, Fed President Goolsbee speaks at 12:45 pm & Fed Chair Powell speaks at 1 pm.

Before Monday’s opening bell Campbell’s Soup & Science Applications Report Earnings, before Credo Technology Group after the close.

Factory Orders & Job Openings data come out Tuesday at 10 am, before Fed President Goolsbee speaks at 12:45 pm, Fed Governor Cook speaks at 1 pm & Fed President Logan speaks at 3:30 pm.

Tuesday morning’s earnings calls include Dollar General, Donaldson, Ferguson, NIO, Ollie’s Bargain Outlet & Signet Jewelers, before CrowdStrike Holdings, Asana, Couchbase, Guidewire Software, Hewlett Packard Enterprise & Yext after the session’s closing bell.

Wednesday morning brings us ADP Employment numbers at 8:15 am, Fed Presidents Bostic & Cook speak at 10:15 am, S&P Final U.S. Services PMI data comes out at 9:45 am, ISM Services data comes out at 10 am & the Fed’s Beige Book is released at 2pm.

Dollar Tree, Genesco, REV Group, Sprinklr & Thor Industries report earnings before the opening bell on Wednesday, while Argan, Descartes, Five Below, Greif, MongoDB, PVH & Verint Systems report earnings following the session’s close.

Thursday brings us Initial Jobless Claims, U.S. Trade Deficit & U.S. Productivity data at 8:30 am, before Fed Governor Kugler speaks at 12 pm & Fed President Harker speaks at 1:30 pm.

Brown-Forman, Ciena, Cracker Barrell, Hello Group, Toro & Victoria’s Secret all report earnings before Thursday’s open, before Broadcom, Braze, DocuSign, Lululemon Athletica, Mission Produce, Petco Health & Welness, Rubrik, Samsara, Service Titan, Vail Resorts & Zumiez report after the closing bell.

U.S. Employment Report, U.S. Unemployment Rate, U.S. Hourly Wages & Hourly Wages Year-over-Year are all due Friday morning at 8:30 am, followed by Consumer Credit at 3pm.

Friday features ABM Industries reporting earnings after the session’s close.

See you back here next week!

*** I DO NOT OWN SHARES OR OPTIONS CONTRACT POSITIONS IN SPY, QQQ, IWM OR DIA AT THE TIME OF PUBLISHING THIS ARTICLE ***

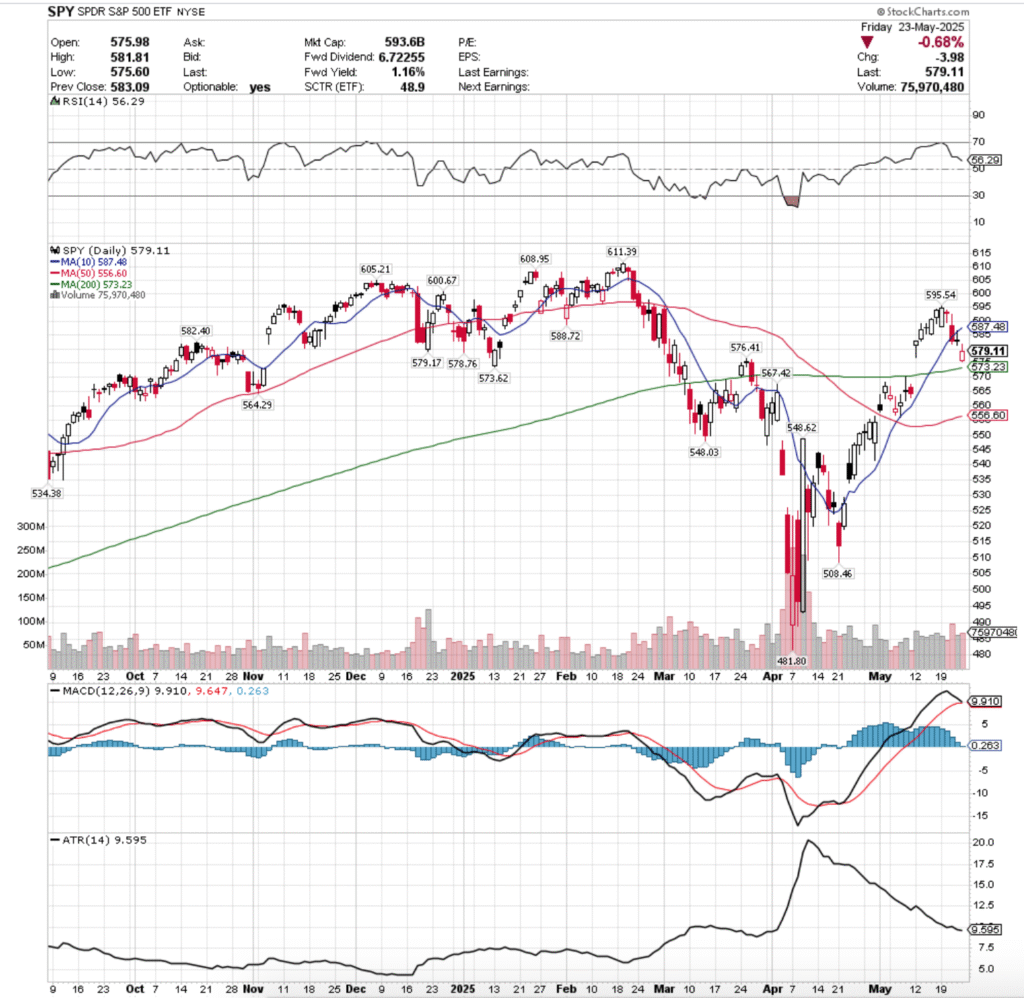

SPY, the SPDR S&P 500 ETF declined -2.54% last week, while the VIX closed the week out at 20.57, indicating an implied one day move of +/-1.3% & an implied one month move of +/-5.95%.

SPY ETF – SPDR S&P 500 ETF’s Techincal Performance Over The Past Year

Their RSI is trending down towards the neutral 50 level & sits currently at 56.29, while their MACD is set to cross over bearishly on Tuesday or Wednesday of this coming week (barring any unusual jumps in price).

Volumes were +31.36% higher than the prior year’s average levels (74,174,000 vs. 56,466,920), which certainly does not inspire near-term confidence, especially heading into a shortened holiday week.

Monday saw SPY walk up to the edge of the diving board, as the week’s second lowest volume session formed a bullish engulfing pattern with the previous Friday’s session, but SPY’s oscillators had begun to show fatigue as we noted last week.

Tuesday is when the breakdown began, as the session opened & formed a dragonfly doji that also created a bearish harami with Monday’s candle on the lowest volume of the week.

While many analysts think of the dragonfly doji as indicating that there is a spike on the horizon & maybe a reversal occuring, the low volume paired with the lower shadow’s range set the stage for more pain throughout the week, particularly given SPY’s proximity to their 10 day moving average.

Wednesday confirmed this, when SPY opened on a gap down, attempted to retrace back towards its closing price level on Tuesday, only to on the highest volume of the week see market participants head towards the exits, and SPY declined -1.69% on the day, closing down by the support of their 10 DMA.

It is worth noting that the 10 DMA temporarily broke down during the session as well, as there was quite a bit of selling pressure surrounding SPY.

Thursday saw SPY opened below the resistance of the 10 day moving average, attempt a run up at it, but it was unable to break out above it & the session closed as a gravestone doji for a gain of +0.04% for the day.

Thursday’s lower shadow also signaled that there was slightly more appetite to the downside day-over-day, which while it was a small amount, isn’t something to be ignored.

Friday showed a risk-off into the holiday weekend theme, as the week’s second highest volume session opened on a gap down, managed to briefly break above Thursday’s low price, and wound up settling higher than it opened, but for a day-over-day loss of -0.68%.

The support of the 200 day moving average was not tested, but prices were trending more in that direction than higher by the end of the week.

Heading into the new week the upside will be contingent on the strength or weakness of the 10 day moving average’s resistance.

What will make this even more interesting to watch is that the current price zone that the 10 DMA is in is historically a Buyer dominated zone, but SPY must first travel through the Seller dominated zone in the middle to earn said re-test, which may wind up showing signs of Buyer-fatigue even in the even that prices make it to that level.

SPY will still need to show strong, consistent advancing volume in order to begin to appear like a base that can be built off of is forming for a reversal.

Should the 10 DMA dip into the Seller dominated zone just above Friday’s closing price it is unlikely that there will be a successful retest of the 10 DMA this week.

The consolidation case involves oscillating between the 200 & 10 day moving averages, while staying around the window created by the gap up open from two Monday’s ago while awaiting a catalyst to the upside or the downside.

There are still some highly anticipated earnings calls this week, including the likes of NVDIA & Salesforce, a slew of Federal Reserve speakers on tap for the week & we’ll get a read on inflation based on PCE data that comes out Friday.

Without any meaningful catalyst in either direction & without some strong volume the consolidation & “wait & see” heading into next week seems the most likely.

In the event of downside action, should the 200 day moving average’s support break down then we will likely see a drop below $570/share & since there are only two support touch-points in the $560’s price range all eyes will be looking towards the 50 day moving average’s support, which will be moving higher to greet SPY’s price.

Given that this week is a short one, unless there is a major catalyst to the upside or downside it seems most likely that things will remain relatively quiet, barring any extreme news or surprises.

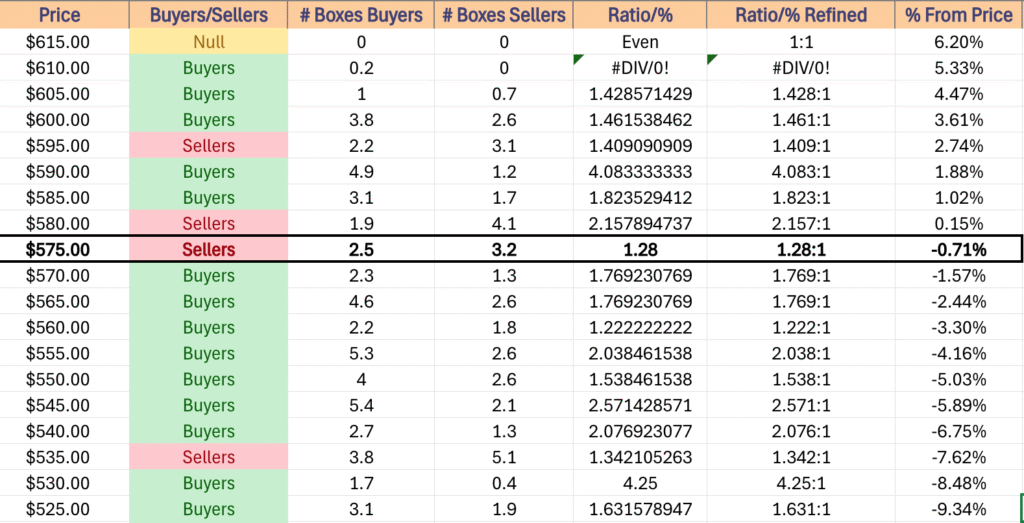

SPY has support at the $578.76 (Volume Sentiment: Sellers, 1.28:1), $576.41 (Volume Sentiment: Sellers, 1.28:1), $573.62 (Volume Sentiment: Buyers, 1.77:1) & $573.23/share (200 Day Moving Average, Volume Sentiment: Buyers, 1.77:1) price levels, with resistance at the $579.17 (Volume Sentiment: Sellers, 1.28:1), $582.40 (Volume Sentiment: Sellers, 2.16:1), $587.48 (10 Day Moving Average, Volume Sentiment: Buyers, 1.82:1) & $588.72/share (Volume Sentiment: Buyers, 1.82:1).

SPY ETF’s Price Level:Volume Sentiment Over The Past ~2-3 Years

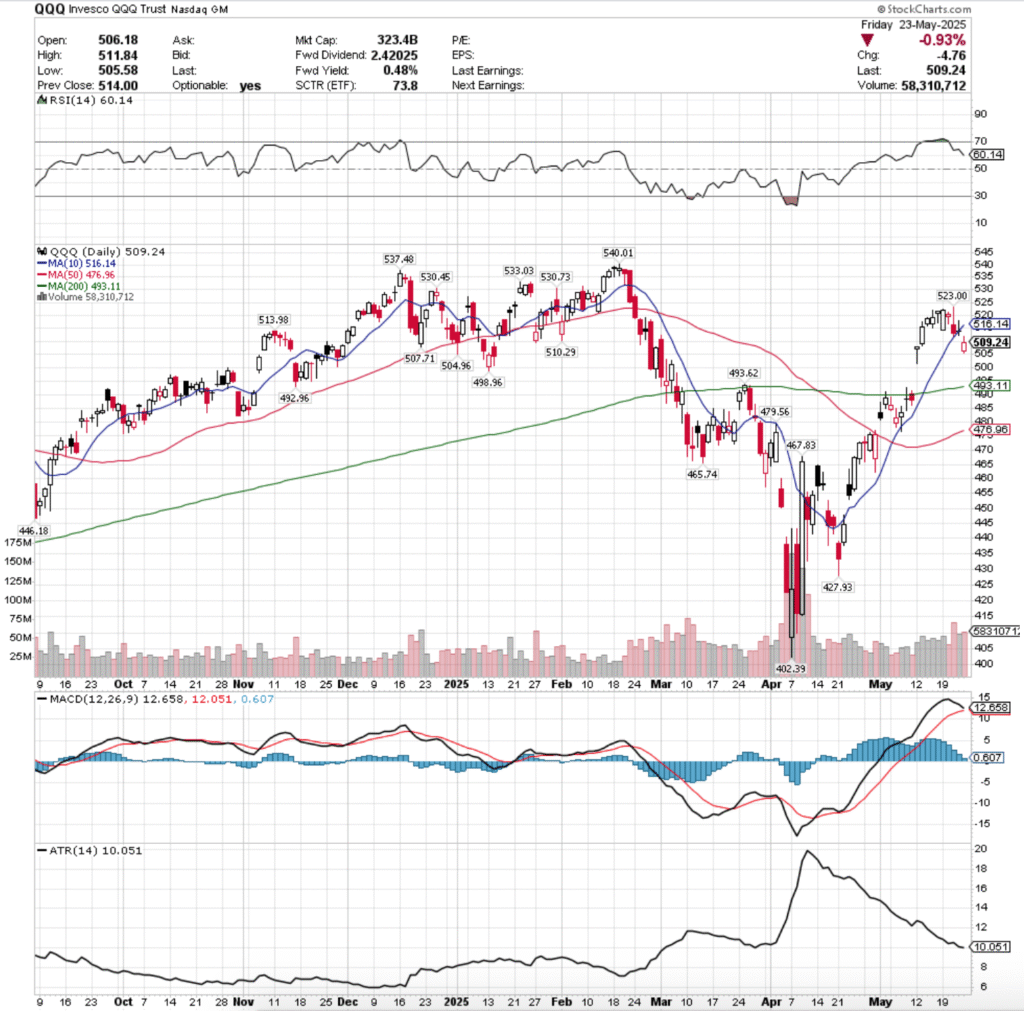

QQQ, the Invesco QQQ Trust ETF dipped -2.35% last week, as the tech-heavy index managed to log the best performance of the four majors.

QQQ ETF – Invesco QQQ Trust’s Technical Performance Over The Past Year

Their RSI dropped back below overbought levels last week & is currently trending lower at 60.14, while their MACD is set to crossover bearishly either Tuesday or Wednesday of this week following last week’s declines.

Volumes were +49.63% higher than the prior year’s average levels (56,066,000 vs. 37,470,0040), which while it shows that there was certainly a degree of profit taking during a week when all major index ETF’s declined, also shows that there is still a decent degree of hopes & optimism attached to Wednesday’s earnings calls for NVDA & Salesforce.

Monday opened the week up for QQQ in a similar manner to SPY, setting the stage for price to jump off of the diving board into the rest of the week.

Tuesday opened lower, tested to below the midway point of Monday’s session before recovering to close higher than it opened, but as a hanging man candle (bearish).

Tuesday also featured the week’s lowest volume, indicating that there was not much positive sentiment behind the day’s price action, even though it did manage to close above its opening price level.

Wednesday saw a shimmer of optimism, as despite a gap down open QQQ’s price was able to rally back to touch $523/share temporarily, but intraday profits were taken quickly, forcing QQQ to retreat & close in-line with the support of their 10 day moving average.

Thursday it was clear that market participants didn’t know which way was up, but they did know that they were only willing to go so much higher up from Wednesday’s close.

The session opened nearly in-line with Wednesday’s close & the 10 day moving average, attempted to rally higher, but was thwarted not much higher than Wednesday’s open, and the support of the 10 day moving average was temporarily broken through.

Friday this carried into the weekend, when the week’s second highest session by Volume opened on a gap lower, tested but managed to stay above the $505/share level, closing the day above its open at $509.24/share.

QQQ is in a similar boat to SPY (as they’ve been relatively similar for years), any upside movement is going to require some stable, strong advancing volume & some form of an upside catalyst, at which point all eyes will be on the 10 day moving average.

Without those conditions, at best any upside move will result in oscillations around the 10 day moving average while awaiting something to move the market.

The consolidation case features oscillations in between the 10 & 200 day moving averages while awaiting news to propel QQQ higher or to break down the 200 day moving average’s support.

In the event of a move lower, the $496-499.99/share price level is Seller dominated over the past year, which would walk prices up with some momentum behind them to retest that 200 DMA.

The window formed at the end of April/early May would then become of interest, as it was never fully closed.

It would also then see the 50 day moving average’s support be tested, which is interesting given that said gap up occurred last time that QQQ’s price tested the 50 DMA.

The table below will be handy for navigating these re-tests.

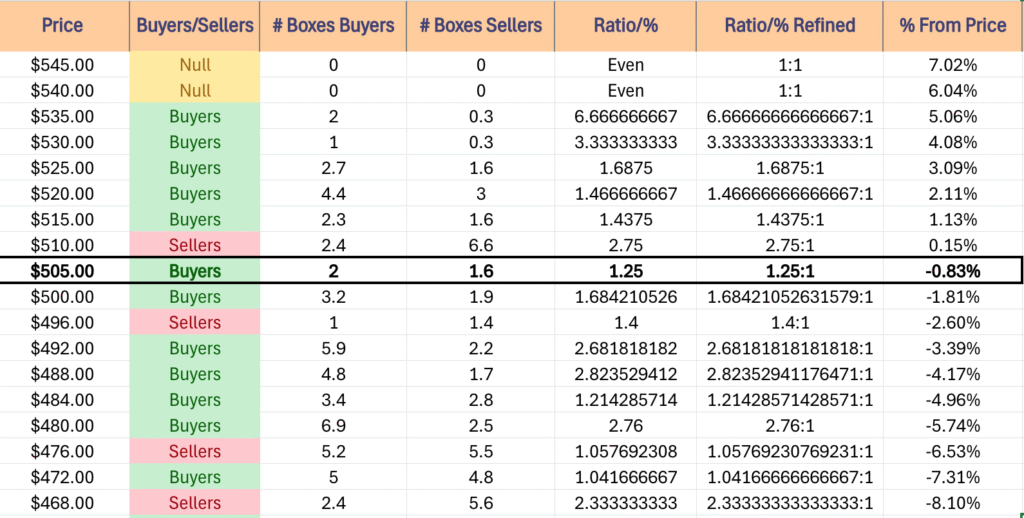

QQQ has support at the $507.71 (Volume Sentiment: Buyers, 1.25:1), $504.96 (Volume Sentiment: Buyers, 1.68:1), $498.96 (Volume Sentiment: Sellers, 1.4:1) & $493.62/share (Volume Sentiment: Buyers, 2.68:1) price levels, with resistance at the $510.29 (Volume Sentiment: Sellers, 2.75:1), $513.98 (Volume Sentiment: Sellers, 2.75:1), $516.14 (10 Day Moving Average, Volume Sentiment: Buyers, 1.44:1) & $523/share (Volume Sentiment: Buyers, 1.47:1).

QQQ ETF’s Price Level:Volume Sentiment Over The Past ~1 Year

IWM, the iShares Russell 2000 ETF fell -3.47% last week, as market participants shunned the small cap index in favor of the other four major indexes.

IWM ETF – iShares Russell 2000 ETF’s Techincal Performance Over The Past Year

Their RSI has flattened out just above the neutral 50 level & is currently at 52.21, while their MACD just crossed over bearishly late last week.

Volumes were -2.8% lower than the prior year’s average level (29,110,000 vs. 29,949,360), which indicates that there is certainly a bit of negative sentiment attached to the small cap index currently amidst market volatility.

Small cap names are not going to have an easy time recovering in the event that weakness is shown by SPY, QQQ or DIA in the next week or two, given how much uncertainty market participants are showing around those larger, more household names.

Monday the small cap index opened on a gap down, but managed to rally back to close above its open, but the session occurred on very weak volume.

Tuesday the uncertainty continued, when prices closed as a spinning top candle, indicating indecision on the weakest volume of the week (which only added to said sense of uncertainty).

Wednesday is when the damn gave way, opening on a gap down in-line with the 10 day moving average, briefly testing higher, but ultimately sliding back beneath the resistance of the 10 day moving average & declining -2.81% for the day.

Given the week’s highest volume occurred Wednesday, this should be taken as a sign of “everybody out of the pool” & that there is slipping levels of confidence in IWM.

The rest of the week IWM moved almost as though it was on stairs, opening Thursday on a gap down & closing the day as a spinning top, which indicates that there was indecision in the air, and lots of it given it occurred on the week’s second strongest volume.

This is especially true given the nature in how much profit taking (and loss cutting) was taking place intra-day when you look at the price levels that IWM was circling around all day.

Friday the week wound down on another gap down open to $199.78, but prices managed to find footing heading into the holiday weekend & closed at $202.56/share.